COMM321 Chapter Notes - Chapter 6: Financial Statement, Consignor, Consignee

13 Apr 2017

School

Department

Course

Professor

Document Summary

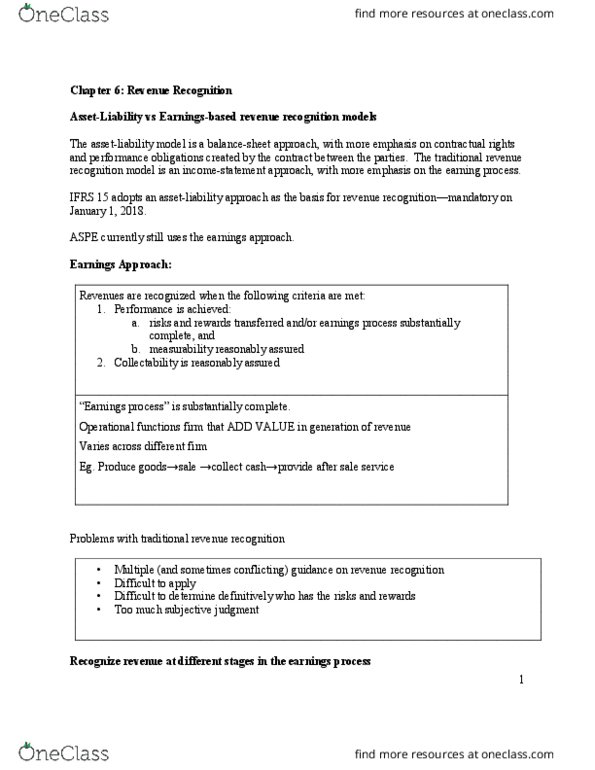

Chapter 6: revenue recognition planning: asset-liability approach (ifrs, earnings approach (aspe, services and long-term contracts (app 6a) (a) percentage-of-completion method aspe, ifrs (b) completed-contract method aspe (c) zero-profit method ifrs, other revenue recognition issues. Agreement that creates enforceable rights or obligations. Can be written, oral, or implied from business practice. Promise in a contract to provide product or service. Contracts with multiple distinct performance obligations represent bundled sales. If goods and services are highly interrelated, they are not separate performance obligations: determine the transaction price. Amount of consideration expected to receive in exchange for goods and services. Consider: time value of money, variable, or non-cash consideration: allocate the transaction price to separate performance obligations. Allocation is based on relative fair values: recognize revenue when performance obligation is satisfied. Obligation is satisfied if control is transferred to customer. Obligation may be satisfied at a point in time (e. g. , deliver goods) or over time (e. g. , provide services)