ACTG 2P31 Lecture Notes - Lecture 6: Consignee, Consignor, Profit Center

8 Dec 2016

School

Department

Course

Professor

Document Summary

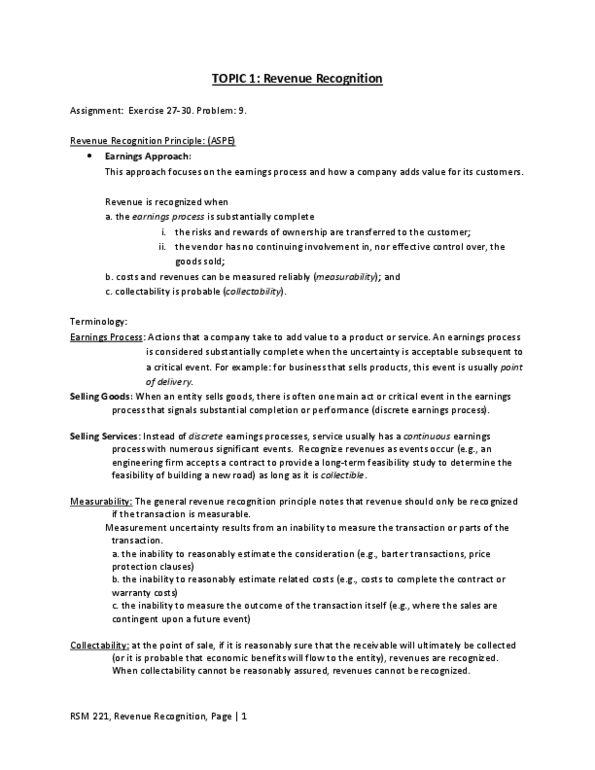

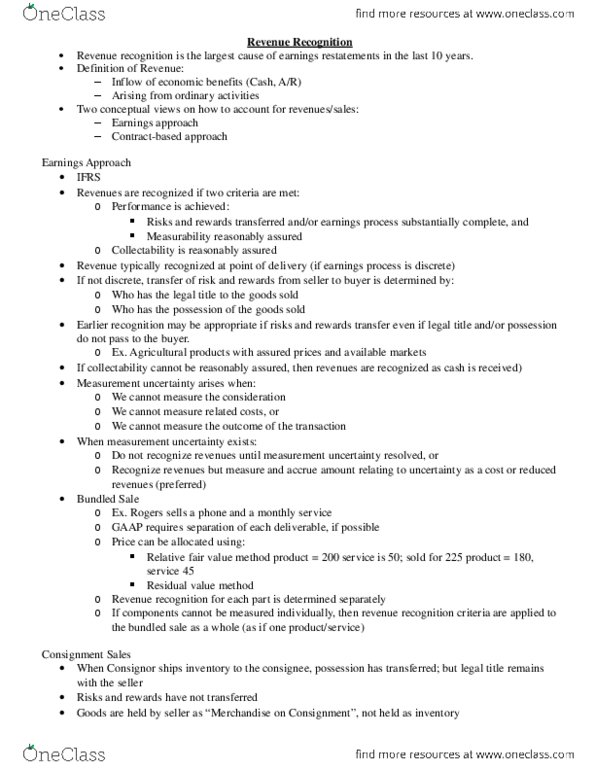

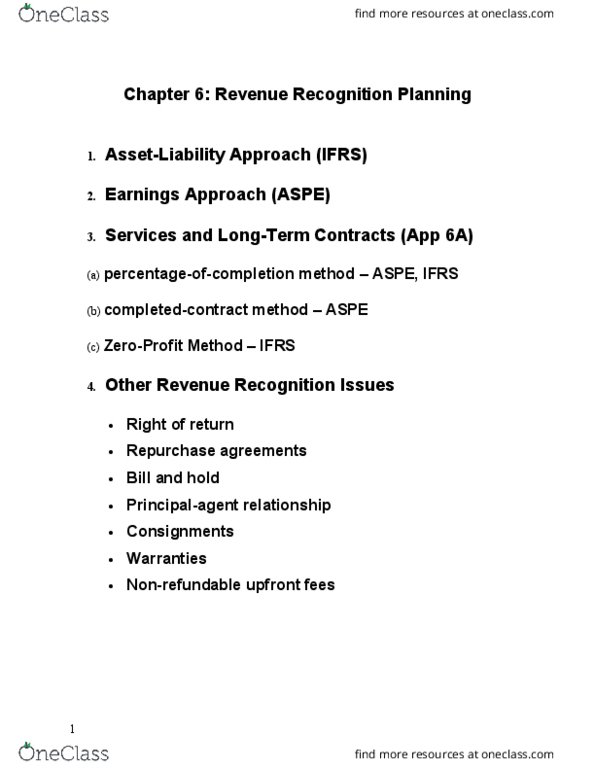

The asset-liability model is a balance-sheet approach, with more emphasis on contractual rights and performance obligations created by the contract between the parties. The traditional revenue recognition model is an income-statement approach, with more emphasis on the earning process. Ifrs 15 adopts an asset-liability approach as the basis for revenue recognition mandatory on. Revenues are recognized when the following criteria are met: performance is achieved, risks and rewards transferred and/or earnings process substantially complete, and, measurability reasonably assured, collectability is reasonably assured. Operational functions firm that add value in generation of revenue. Problems with traditional revenue recognition: multiple (and sometimes conflicting) guidance on revenue recognition, difficult to apply, difficult to determine definitively who has the risks and rewards, too much subjective judgment. Recognize revenue at different stages in the earnings process. Many long term construction contracts: when production is complete (before sale)