BADM*2020 Chapter Notes - Chapter 10: Standard Cost Accounting, European Cooperation In Science And Technology, Deutsche Luft Hansa

Document Summary

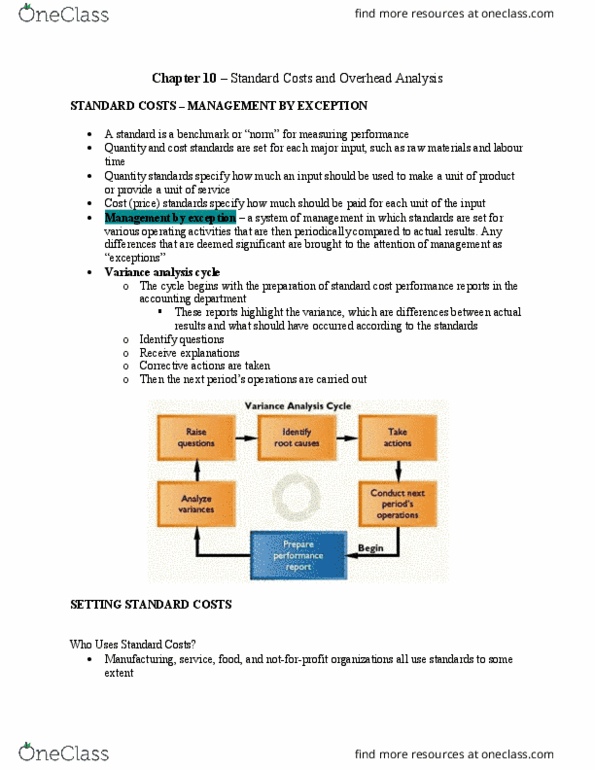

Agenda: standard costs: standard costs, setting standard costs. Setting standard costs: a standard is a benchmark or norm for measuring performance, price standard: how much an input should cost, quantity standard: how much of a given input should be used to make a unit of output. Ideal standards allow for no machine breakdowns or work interruptions, and can be attained only by working at peak effort 100% of the time. Such standards: often discourage workers, shouldn"t be used for decision making. Practical standards allow for normal down time, employee rest periods, and the like. Such standards: are felt to motivate employees, since the standards are tight but attainable. , are useful for decision purposes, since variances from standard will contain only abnormal elements. Budget is for whole company, departments, products etc. Need to stretch, but not so far that it is out of reach. The company wants to develop standards for material, labour, and variable manufacturing overhead.