BADM*2020 Chapter Notes -Contribution Margin, Variable Cost

Document Summary

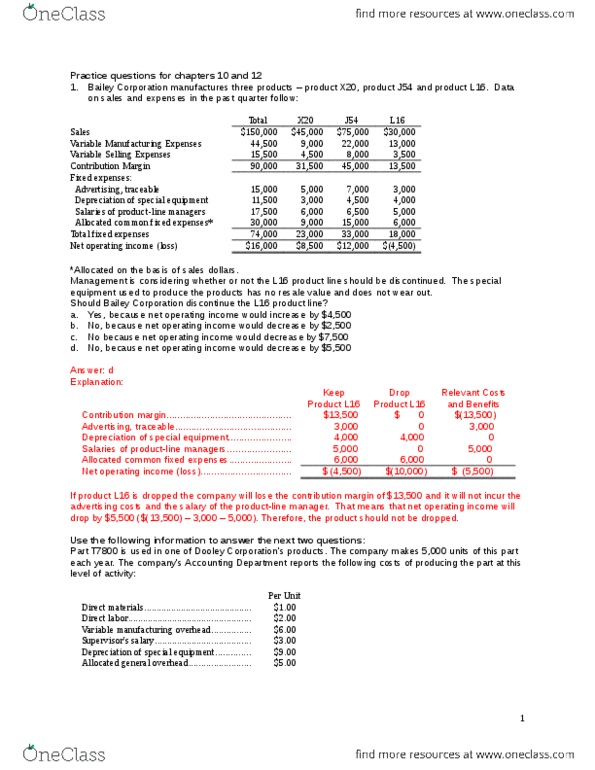

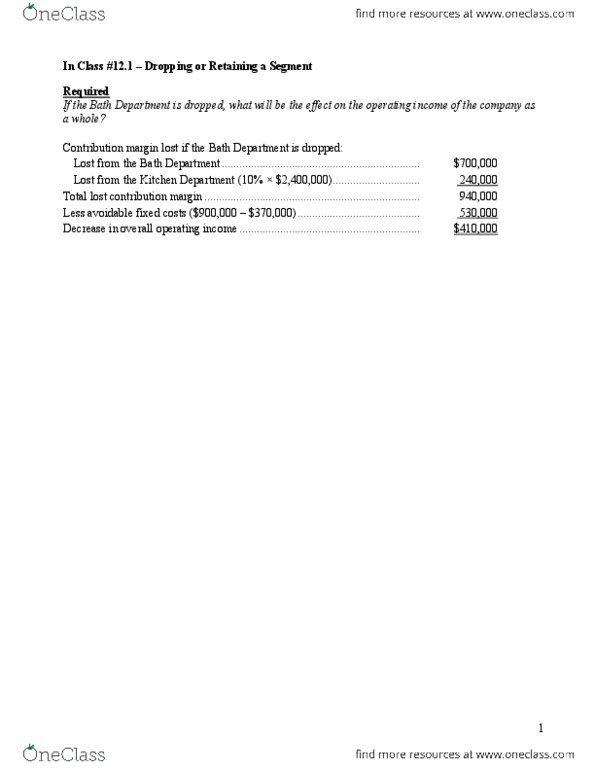

*six years remaining useful life, no salvage value, or current resale value. If the division is dropped, the staff will be laid-off, with the exception of one person who. The company has the following per unit product costs for a part it produces and uses in another division. 75% of the traceable fixed overhead consists of depreciation of equipment with no resale value. 25% of the traceable fixed overhead can be avoided if the part is bought from an outside supplier. An outside supplier is offering to sell the company 5,000 units at each. The company produces two products, standard and deluxe. Production of each of these products requires time on a machine that has a capacity to run 9,600 minutes per month. A company produces two products from a common input: The net effect is negative, therefore do not drop. Therefore it is cheaper to make rather than buy.