BUSI 2160U Chapter Notes - Chapter 8: Historical Cost, Intangible Asset, Capital Asset

Document Summary

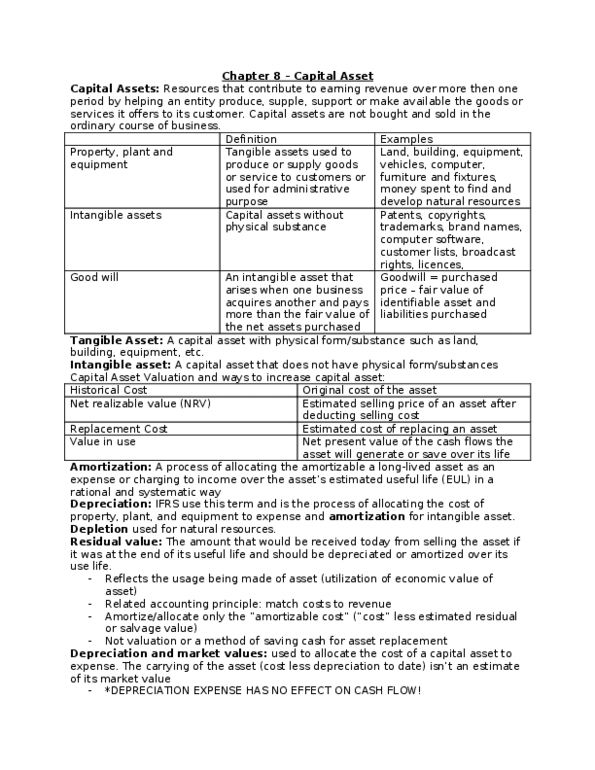

Chapter 8 capital assets: property, plant, and equipment, intangibles, and goodwill. Capital assets are resources that contribute to the earnings of revenue over more than one period by helping an entity to produce, supply, support, or make available the goods or services it offers to its customers. Tangible asset is a capital asset with physical substance, such as land, buildings, equipment, vehicles, and furniture. Intangible assets lack physical substance, such as patents, copyrights, trademarks, brand names and good will. Common practice for companies to lease assets instead of buying them. Measuring capital assets & limitations to historical cost accounting. Capitalized is an amount expended or accrued that is recorded on the balance sheet as an asset. Historical cost accounting"s purpose is to match the cost of capital assets to revenue earned over the life of the asset. Three alternatives to historical cost accounting for capital assets: fair value, replacement cost, and value-in-use.