BUSI 2402U Chapter Notes - Chapter 11: Risk Premium, Westjet, Weighted Arithmetic Mean

Document Summary

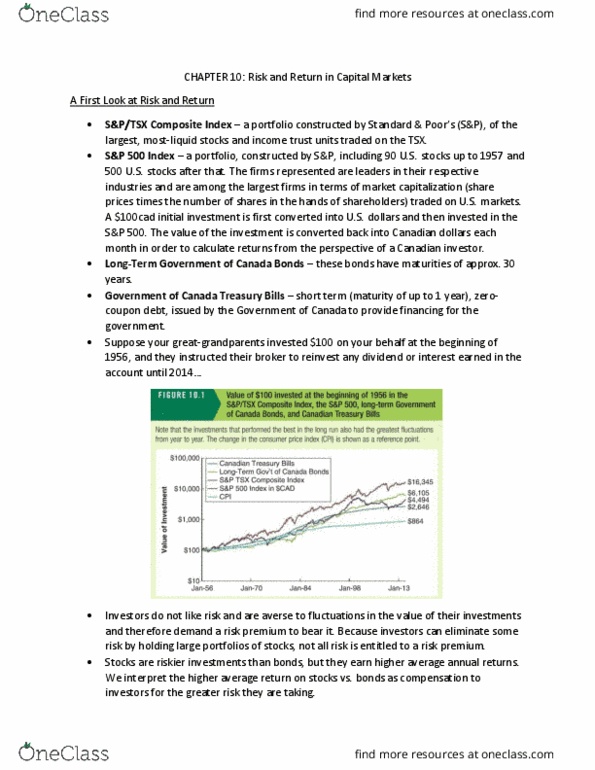

Chapter 11: systematic risk and the equity risk premium. The expected return of a portfolio: portfolio weight the fraction of the total investment of each stock (westjet, hasbro, The volatility of a portfolio: volatility of a portfolio the total risk, measured as sd, of a portfolio. For example, because the two airline stocks tend to perform well or poorly at the same time, the portfolio of airline stocks has a volatility that is only slightly lower than the volatility of the individual stocks. The airline and oil stocks, on the other hand, do not move together almost in opposite directions. As a results, more risk is cancelled out, making that portfolio less risky. So, stocks in the same industry tend to have highly correlated returns than stocks in different industries: see page 381 to learn how to calculate correlation on excel! As a result, its clear that we can eliminated some volatility by diversifying.