ECO 1104 Chapter Notes - Chapter 5: Demand Curve, Inferior Good, Normal Good

18 Oct 2016

School

Department

Course

Professor

16

ECO 1104 Full Course Notes

Verified Note

16 documents

Document Summary

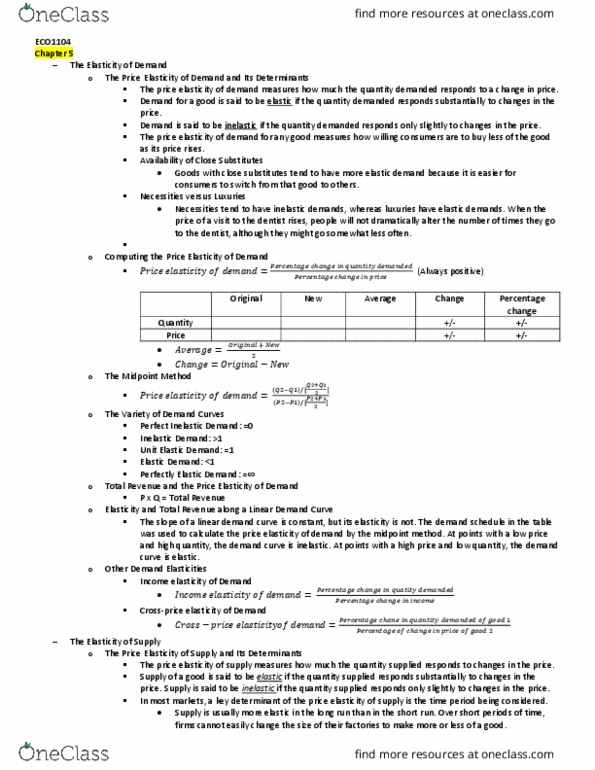

Measure of how much buyers and sellers respond to changes in market conditions. To measure how much consumers respond to changes in these price, income, price of complement and substitute. Ration of percentage change in two variabes. Price elasticity of demand: measures how much the quantity demanded responds to a change in price. Price elasticity of demand = percentage change in quantity demanded. Elastic: if the demand responds substantially to changes in the price. Inelastic: if the quantity demanded responds only slightly to changes in price. Because consumers switch to the other good if it gets too expensive. Because it is easier to find substitutes. Goods have more elasticity over longer time horizons. Price elasticity of demand= (q2-q1)/[(q2+q1)/2] => midpoint % change in quantity (p2-p1)/[(p2+p1)/2] => midpoint% change in price. Total revenue: the amount paid by buyers and received by sellers of a good, computed as the price of the good times the quantity sold.