MGAB01H3 Chapter Notes - Chapter 10-13: Profit Margin, Quick Ratio, Dividend Yield

MGAB01H3 Full Course Notes

Document Summary

Get access

Related Documents

Related Questions

|

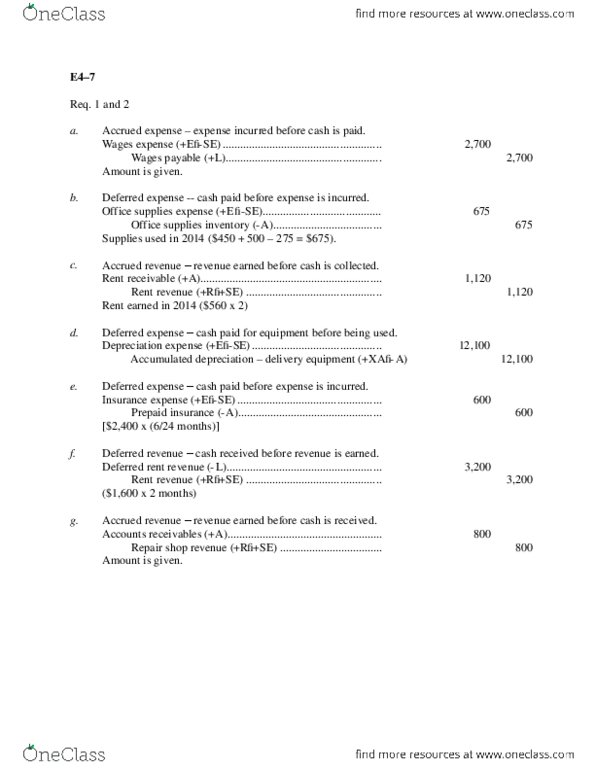

Record the necessary correcting and adjusting entries. Indicate which of the adjusting entries may be reversed at thebeginning of the next accounting period. |

Terrific Temps fills temporary employment positions for localbusinesses. Some businesses pay in

advance for services; others are billed after services have beenperformed. Advanced payments are

credited to an account entitled Unearned Fees. Adjusting entriesare performed on a monthly basis.

An unadjusted trial balance dated December 31, 2015, follows. (Bearin mind that adjusting entries

have already been made for the first 11 months of 2015, but not forDecember.)

| TERRIFIC TEMPS UNADJUSTED TRIAL BALANCE DECEMBER 31, 2015 | |||||

| Cash | $ | 27,020 | |||

| Accounts receivable | 59,200 | ||||

| Unexpired insurance | 900 | ||||

| Prepaid rent | 3,000 | ||||

| Office supplies | 600 | ||||

| Equipment | 60,000 | ||||

| Accumulated depreciation: equipment | $ | 29,500 | |||

| Accounts payable | 4,180 | ||||

| Notes payable | 12,000 | ||||

| Interest payable | 320 | ||||

| Unearned fees | 6,000 | ||||

| Income taxes payable | 4,000 | ||||

| Unearned revenue | 20,000 | ||||

| Retained earnings | 49,000 | ||||

| Capital stock | 25,000 | ||||

| Dividends | 3,000 | ||||

| Feesearned | 75,000 | ||||

| Travel expense | 5,000 | ||||

| Insurance expense | 2,980 | ||||

| Rentexpense | 9,900 | ||||

| Office supplies expense | 780 | ||||

| Utilities expense | 4,800 | ||||

| Depreciation expense: equipment | 5,500 | ||||

| Salaries expense | 30,000 | ||||

| Interest expense | 320 | ||||

| Income taxes expense | 12,000 | ||||

| $ | 225,000 | $ | 225,000 | ||

| Other Data | |

| 1. | Accrued butunrecorded fees earned as of December 31, 2015, amount to$1,500. |

| 2. | Records showthat $2,500 of cash receipts originally recorded as unearned feeshad been earned as of December 31. |

| 3. | The companypurchased a six-month insurance policy on September 1, 2015, for$1,800. |

| 4. | On December 1,2015, the company paid its rent through February 28, 2016. |

| 5. | Office supplieson hand at December 31 amount to $400. |

| 6. | All equipment was purchased when the business first formed. Theestimated life of the equipment at that time was 10 years (or 120months). |

| 7. | On August 1, 2015, the company borrowed $12,000 by signing asix-month, 8 percent note payable. The entire note, plus sixmonths' accrued interest, is due on February 1, 2016. |

| 8. | Accrued butunrecorded salaries at December 31 amount to $2,700. |

| 9. | Estimated incometaxes expense for the entire year totals $15,000. Taxesare due in the first quarter of 2016. |

| Instructions |

| a. | For each of thenumbered paragraphs, prepare the necessary adjusting entry.(If no entry is required for a transaction/event, select"No journal entry required" in the first accountfield.) |

Journal Entry Worksheet

Record the accrued but uncollected fees earned.

Record fees earned as of December 31st.

Record the December insurance expense.

Record the December rent expense.

Record the offices supplies used in December.

Record the December depreciation expense.

Record the interest accrued in December.

Record the salaries accrued in December.

Record the income taxes accrued in December.

| |||||||||||||||||||||||||

|

*Enter debits before credits

| 1. | Fees earned | |

| 2. | Travel expense | |

| 3. | Insurance expense | |

| 4. | Rent expense | |

| 5. | Office supplies expense | |

| 6. | Utilities expense | |

| 7. | Depreciation expense: equipment | |

| 8. | Interest expense | |

| 9. | Salaries expense | |

| 10. | Income taxes expense |

| . | The unadjusted trial balance reportsdividends of $3,000. As of December 31, 2015, have these dividendsbeen paid? | ||||

|

Please record the entry to close revenue earned to income summary, close all expense accounts to income summary, record the entry to transfer net income earned in 2015 to the retained earnings account, and Record the entry to transfer dividends declared in 2015 to the retained earnings account

| On December 1, 2015, John and Patty Driver formed a corporation called Susquehanna Equipment Rentals. The new corporation was able to begin operations immediately by purchasing the assets and taking over the location of Rent-It, an equipment rental company that was going out of business. The newly formed company uses the following accounts: |

| Cash | Capital stock |

| Accounts receivable | Retained earnings |

| Prepaid rent | Dividends |

| Unexpired insurance | Income summary |

| Office supplies | Rental fees earned |

| Rental equipment | Salaries expense |

| Accumulated depreciation: Rental equipment | Maintenance expense |

| Notes payable | Utilities expense |

| Accounts payable | Rent expense |

| Interest payable | Office supplies expense |

| Salaries payable | Depreciation expense |

| Dividends payable | Interest expense |

| Unearned rental fees | Income taxes expense |

| Income taxes payable |

| The corporation performs adjusting entries monthly. Closing entries are performed annually on December 31. During December, the corporation entered into the following transactions: |

| Dec. 1 | Issued to John and Patty Driver 20,000 shares of capital stock in exchange for a total of $200,000 cash. | |

| Dec. 1 | Purchased for $240,000 all of the equipment formerly owned by Rent-It. Paid $140,000 cash and issued a one-year note payable for $100,000. The note, plus all 12-months of accrued interest, are due November 30, 2016. | |

| Dec. 1 | Paid $12,000 to Shapiro Realty as three monthsâ advance rent on the rental yard and office formerly occupied by Rent-It. | |

| Dec. 4 | Purchased office supplies on account from Modern Office Co., $1,000. Payment due in 30 days. (These supplies are expected to last for several months; debit the Office Supplies asset account.) | |

| Dec. 8 | Received $8,000 cash as advance payment on equipment rental from McNamer Construction Company. (Credit Unearned Rental Fees.) | |

| Dec. 12 | Paid salaries for the first two weeks in December, $5,200. | |

| Dec. 15 | Excluding the McNamer advance, equipment rental fees earned during the first 15 days of December amounted to $18,000, of which $12,000 was received in cash. | |

| Dec. 17 | Purchased on account from Earth Movers, Inc., $600 in parts needed to repair a rental tractor. (Debit an expense account.) Payment is due in 10 days. | |

| Dec. 23 | Collected $2,000 of the accounts receivable recorded on December 15. | |

| Dec. 26 | Rented a backhoe to Mission Landscaping at a price of $250 per day, to be paid when the backhoe is returned. Mission Landscaping expects to keep the backhoe for about two or three weeks. | |

| Dec. 26 | Paid biweekly salaries, $5,200. | |

| Dec. 27 | Paid the account payable to Earth Movers, Inc., $600. | |

| Dec. 28 | Declared a dividend of 10 cents per share, payable on January 15, 2016. | |

| Dec. 29 | Susquehanna Equipment Rentals was named, along with Mission Landscaping and Collier Construction, as a co-defendant in a $25,000 lawsuit filed on behalf of Kevin Davenport. Mission Landscaping had left the rented backhoe in a fenced construction site owned by Collier Construction. After working hours on December 26, Davenport had climbed the fence to play on parked construction equipment. While playing on the backhoe, he fell and broke his arm. The extent of the companyâs legal and financial responsibility for this accident, if any, cannot be determined at this time. ( Note: This event does not require a journal entry at this time, but may require disclosure in notes accompanying the statements.) | |

| Dec. 29 | Purchased a 12-month public-liability insurance policy for $9,600. This policy protects the company against liability for injuries and property damage caused by its equipment. However, the policy goes into effect on January 1, 2016, and affords no coverage for the injuries sustained by Kevin Davenport on December 26. | |

| Dec. 31 | Received a bill from Universal Utilities for the month of December, $700. Payment is due in 30 days. | |

| Dec. 31 | Equipment rental fees earned during the second half of December amounted to $20,000, of which $15,600 was received in cash. | |

| Data for Adjusting Entries |

| a. | The advance payment of rent on December 1 covered a period of three months. |

| b. | The annual interest rate on the note payable to Rent-It is 6 percent. |

| c. | The rental equipment is being depreciated by the straight-line method over a period of eight years. |

| d. | Office supplies on hand at December 31 are estimated at $600. |

| e. | During December, the company earned $3,700 of the rental fees paid in advance by McNamer Construction Company on December 8. |

| f. | As of December 31, six daysâ rent on the backhoe rented to Mission Landscaping on December 26 has been earned. |

| g. | Salaries earned by employees since the last payroll date (December 26) amounted to $1,400 at month-end. |

| h. | It is estimated that the company is subject to a combined federal and state income tax rate of 40 percent of income before income taxes (total revenue minus all expenses other than income taxes). These taxes will be payable in 2016. |