MGAB03H3 Chapter Notes - Chapter 1: Business Process Management, Management Accounting, International Financial Reporting Standards

22 Oct 2013

School

Department

Course

Professor

Document Summary

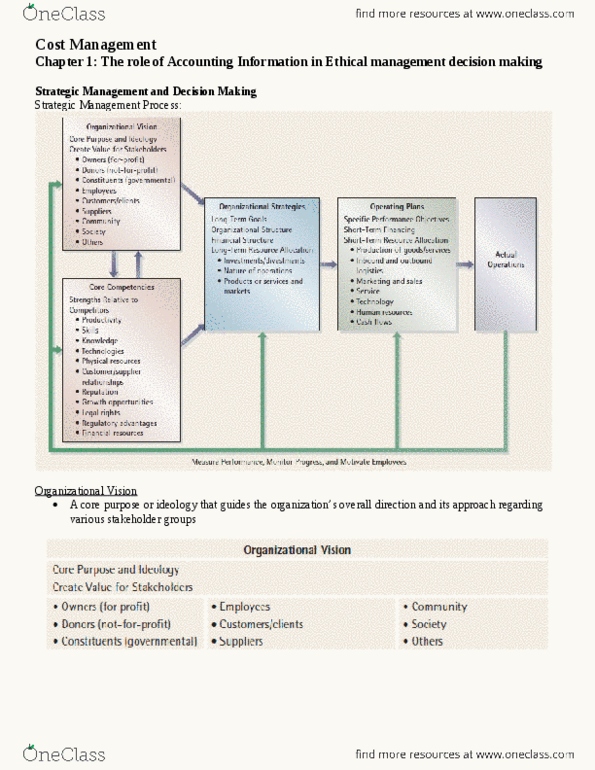

Chapter one: the role of accounting information in ethical management. Organizational vision: core purpose & ideology of an organization, which guides the organization"s overall direction & approaches toward various stakeholder groups. Shud b built on existing & achievable strengths. Organizational core competencies: the organization"s strengths relative to its competitors which creates value for stakeholders. Usually find theses by evaluating a company"s swot. Swot analysis: an analysis which looks @ the strengths, weaknesses, opportunities, and threats of an organization. Organizational strategies: the tactics that mangers use to take advantage of core competencies, while working toward the organizational vision. Operating plans: involves specific short-term decisions that shape an organization"s day-to-day activities, drawing cash from a bank line of credit, hiring an employee, or ordering material. Often include specific performance objectives, such as a budgeted revenue & costs. Actual operations: the various actions taken & results achieved over a period of time.