Answer the following questions based on the case:

1. What triggered the 2008 financial crisis and how did it happen?

2. How did deregulation and derivatives contribute to the financial crisis?

3. What happened in 2003 when demand for mortgage-backed securities began outstripping supply?

4. Who is to blame for the financial crisis?

5. What actions were taken beginning October 2008 to end the crisis?

6. Based on actions taken after October 2008 to end the financial crisis, do you believe it could happen again? Support your answer.

The Global Financial Crisis of 2008:

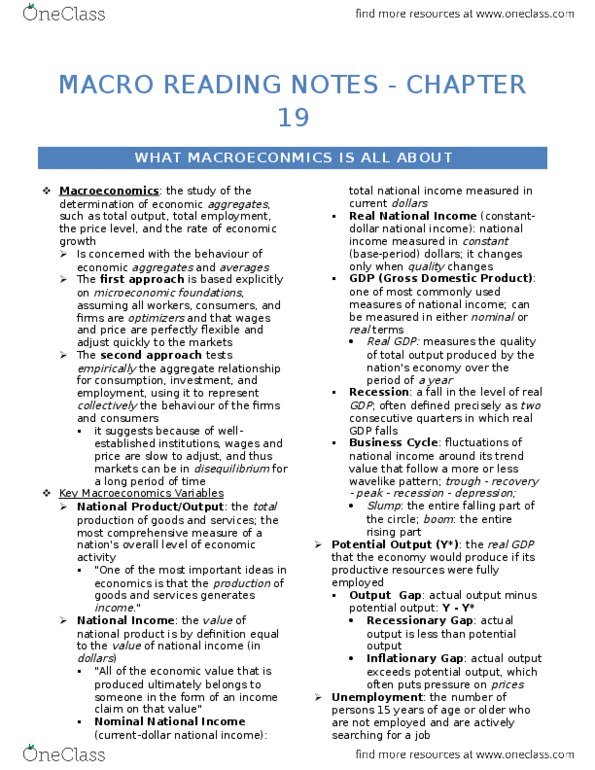

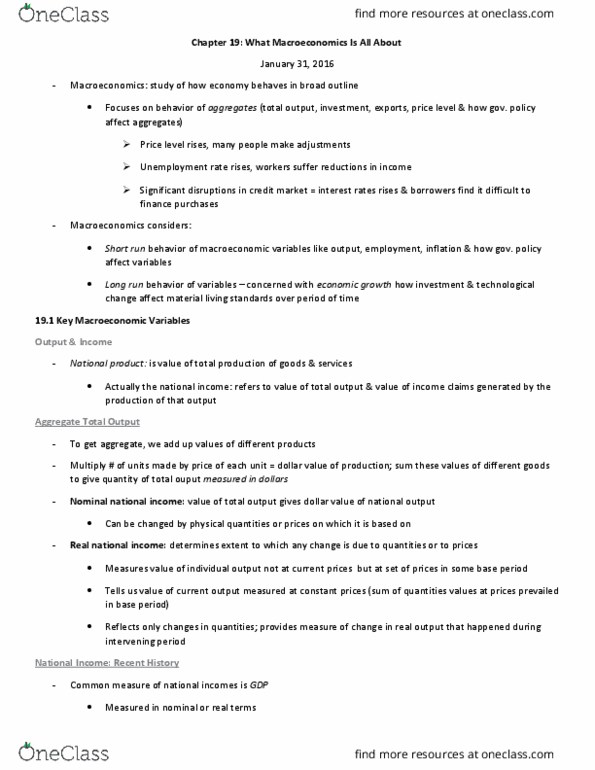

The Role of Greed, Fear, and Oligarchs Cate Reavis Free enterprise is always the right answer. The problem with it is that it ignores the human element. It does not take into account the complexities of human behavior.1 â Andrew W. Lo, Professor of Finance, MIT Sloan School of Management; Director, MIT Laboratory of Financial Engineering The problem in the financial sector today is not that a given firm might have enough market share to influence prices; it is that one firm or a small set of interconnected firms, by failing, can bring down the economy.2 â Simon Johnson, Professor of Entrepreneurship, MIT Sloan School of Management; Former Chief Economist, International Monetary Fund On October 9, 2007, the Dow Jones Industrial Average set a record by closing at 14,047. One year later, the Dow was just above 8,000, after dropping 21% in the first nine days of October 2008. Major stock markets in other countries had plunged alongside the Dow. Credit markets were nearing paralysis. Companies began to lay off workers in droves and were forced to put off capital investments. Individual consumers were being denied loans for mortgages and college tuition. After the nine-day U.S. stock market plunge, the head of the International Monetary Fund (IMF) had some sobering words: âIntensifying solvency concerns about a number of the largest U.S.-based and 1 Interview with the case writer, April 10, 2009. 2 Simon Johnson, âThe Quiet Coup,â The Atlantic, May 2009. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 2 European financial institutions have pushed the global financial system to the brink of systemic meltdown.â3 By early 2009, the markets had stabilized to the point where the U.S. stock market was no longer down 700 points one day and up 500 the next. In May, the results of the stress tests conducted on the 19 largest banks in the United States to test their capacity to withstand a further economic downturn were less negative than feared, with 10 out of the 19 subjected to the test ordered to raise $75 billion in new capital. A number of the banks that were told to raise additional capital saw their stocks rise sharply on the day the results were released, with Wells Fargo up 24% and Bank of America up 19%.4 Despite the seemingly improved situation, academics, practitioners, and politicians alike were debating how we got to where we were, and what to do in both the short and long term to bring more lasting order to the chaos and prevent the same level of turmoil the next time a financial crisis hit. That there would be a next time was indisputable in the eyes of Andrew Lo, a professor of finance at the MIT Sloan School of Management and the director of MITâs Laboratory of Financial Engineering. In fact, since 1974, 18 bank crises had occurred around the world, and each shared something in common: a period of great financial liberalization and prosperity that preceded the crisis. As Lo remarked in his November 2008 testimony before the House Oversight Committee Hearing on Hedge Funds, âFinancial crises may be an unavoidable aspect of modern capitalism, a consequence of the interactions between hardwired human behavior and the unfettered ability to innovate, compete, and evolve.â5 Simon Johnson, a professor of entrepreneurship at the MIT Sloan School of Management and former chief economist at the IMF from 2007 to 2008, believed that the current crisis was caused by powerful elites, what he called a banking âoligarchyâ that overreached in good times and took too many risks. As he wrote in an article for The Atlantic, âElite business interests played a central role in creating the crisis, making ever-larger gambles, with the implicit backing of the government, until the inevitable collapse.â6 Understanding what, how, and why the crisis happened was a critical part of the process to stabilize the financial system in the short term and soften the blow of the next financial crisis. Johnson and Lo were actively involved in finding those solutions. Whether they were advocating the right solutionsâ and whether such solutions could or would be implementedâremained unknown. What also 3 âIMF in Global âMeltdownâ Warning,â BBC News, October 12, 2008. 4 Damian Paletta and Deborah Solomon, âMore Banks Will Need Capital,â The Wall Street Journal, May 5, 2009. 5 Andrew W. Lo, âHedge Funds, Systemic Risk, and the Financial Crisis of 2007â2008: Written Testimony for the House Oversight Committee Hearing on Hedge Funds,â November 13, 2008, p. 1. 6 Simon Johnson, âThe Quiet Coup,â The Atlantic, May 2009. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 3 remained unknown was whether their solutions aptly addressed what David Beim, a finance professor at Columbia Business School, believed was at the heart of the problem: The problem is not the banks, greedy though they may be, overpaid though they may be. The problem is us. We have been living very high on the hog. Our standard of living has been rising dramatically over the last 25 years, and we have been borrowing to make much of that prosperity happen. We have over-borrowed, and we have done that over many, many decades. And now itâs reached just an unbearable peak where people on average cannot repay the debts theyâve got.7 What Happened From a macroeconomic perspective, the collapse of the U.S. housing market triggered the financial crisis that began in 2008.8 As Johnson explained, the erosion of the housing market led to an erosion of wealth: What is on everyoneâs minds is this big loss of wealth. We had stocks that are now worth 50% less than what they were worth. We owned houses that have fallen substantially in value. The point is that people were banking on these assets having a certain value. And that has implications for how much they were willing to consume and if they were firms how much they were willing to invest.9 Few ordinary investors believed that the U.S. housing market would ever crash. For many years, real estate was considered one of the safest and most profitable investments. From the late 1990s into the mid-2000s, housing prices around the country rose at a compound annual growth rate of 8%. By 2006, the average home cost nearly four times what the average family made. (Historically, it had been between two to three times.10) Demand was outstripping supply. Even though household incomes remained flat during this time (Figure 1), more and more people were able to afford houses due to an easing of lending requirements that began in the Clinton administration and continued into the Bush administration. High-risk loans, including subprime mortgages given to people with troubled credit, fueled the growth. In fact, the housing boom from the late 1990s into the mid-2000s drove much of the U.S. economy, adding jobs in construction, remodeling, and real estate services. Consumers feasted on the equity in their homes, taking out a total of $2 trillion via loans, refinancings, and sales. 11 The ratio that measures household debt to GDP doubled from 50% in the 1980s to 100% of GDP by the mid- 7 Ira Glass, Adam Davidson, and Alex Blumberg, âBad Bank,â NPR: This American Life, February 27, 2009. 8 For a more in-depth explanation of the financial crisis, see the blog http://baselinescenario.com. 9 Terry Gross, âSimon Johnson On Bank Bailout Plan,â NPR: Fresh Air, March 3, 2009. 10 Ben Steverman and David Bogoslaw, âThe Financial Crisis Blame Game,â BusinessWeek, October 18, 2008. 11 Shawn Tully, âWelcome to the Dead Zone,â Fortune, May 5, 2006. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 4 2000s. The last time the level of debt was 100% of GDP was 1929, the beginning of the Great Depression. 12 Figure 1 Growth of U.S. Housing Prices versus Household Income, 1991â2007 Source: S&P/Case-Shiller National Home Price Indices; U.S. Census Bureau. By 2006, it was evident that the housing bubble was starting to burst. People began defaulting on their mortgages, sending a ripple effect throughout the financial system. As more people defaulted and went into foreclosure, more houses came on the market and precipitously pushed down housing prices (Figure 2). Figure 2 U.S. Housing Prices, 1990â2008 (adjusted for inflation) Source: S&P/Case-Shiller National Home Price Indices. 12 Ira Glass, Adam Davidson, and Alex Blumberg, âBad Bank,â NPR: This American Life, February 27, 2009. $0 $50,000 $100,000 $150,000 $200,000 $250,000 $300,000 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 $149,752 $171,421 $261,739 $180,100 -15 -10 -5 0 5 10 15 % Growth Housing Prices Household Income Housing Prices -2.2 -2.4 -0.7 0.5 0 -0.8 2.7 5.7 5.5 6.2 5.8 8.1 8.7 10.9 10.7 -2.2 -12.5 Household Income 0.6 1.7 2 3.3 5.6 4.2 6 3.4 4.7 3.2 0.6 0.4 2.1 2.3 4.5 4 4.2 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 5 As prices began to fall and the loan default rate began to rise, big Wall Street firms stopped gobbling up the riskier mortgages, which at one time had been extremely lucrative. Smaller banks and mortgage companies were left saddled with loans that they had borrowed money to buy in the first place and now could not sell. Suddenly, banks started defaulting on their loans as well, triggering the downward spiral that by late 2008 gripped the world economy. Many banks were facing insolvency: Their assets were too small to cover their liabilities, which meant that they owed more money than they had. Credit markets started to freeze up, and individuals and businesses alike could not get loans.13 This was more or less the simplistic macroeconomic explanation. But Andrew Lo believed that the crisis was about more than economic forces. In his mind, a human element was at play, most notably the emotions of greed and fear of the unknown. As Lo stated in his House Oversight Committee testimony: During extended periods of prosperity, market participants become complacent about the risk of lossâeither through a systematic underestimation of those risks because of recent history, or a decline in their risk aversion due to increasing wealth, or both. In fact, there is mounting evidence from cognitive neuroscientists that financial gain affects the same âpleasure centersâ of the brain that are activated by certain narcotics. This suggests that prolonged periods of economic growth and prosperity can induce a collective sense of euphoria and complacency among investors that is not unlike the drug-induced stupor of a cocaine addict. The seeds of this crisis were created during a lengthy period of prosperity. During this period we became much more risk tolerant.14 In other words, âweâ became greedy. As Lo put it, this greed was spurred on by âthe profit motive, the intoxicating and anesthetic effects of success.â15 When everything began to collapse, our greed then turned into fear. What we feared, Lo argued, was the unknownâin this case, who and what we owed, what our assets were worth, and how bad things really were. As one journalist wrote, âConcern about who is still holding dud paper has gummed up credit markets, with banks refusing to lend to one another for fear that the borrowers may default or may have themselves lent to other banks that could default.â16 Banks were not willing to mark-to-market. This meant that they did not want to enter the actual market price of their assets on their books, for by doing so many would be declaring bankruptcy. Instead, many banks chose to hold on to their assets, thinking either that they were worth more than the market thought or that they would come back.17 13 Ira Glass, Adam Davidson, and Alex Blumberg, âBad Bank,â NPR: This American Life, February 27, 2009. 14 Andrew W. Lo, âHedge Funds, Systemic Risk, and the Financial Crisis of 2007â2008: Written Testimony for the House Oversight Committee Hearing on Hedge Funds,â November 13, 2008, p. 12. 15 Ibid., p. 14. 16 Peter Gumbel, âThe Meltdown Goes Global,â Time, October 20, 2008. 17 Ira Glass, Adam Davidson, and Alex Blumberg, âBad Bank,â NPR: This American Life, February 27, 2009. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 6 Fear froze the markets, which in turn led to liquidity runs on financial institutions, even those that were not facing insolvency. Johnson explained: The fundamental problem is that all players in the financial system have realized that a bank that is solvent can still be subject to a bank run. Once that happens, Bank A doesnât want to lend money to Bank B for two reasons: first, Bank A wants to hold on to its cash in case it becomes the target of a bank run; and, second, Bank A is afraid that Bank B could be the target of a bank run, and hence is afraid that if it lends to Bank B it wonât get its money back. Like all such panics, this becomes self-fulfilling: because banks donât want to lend, banks canât get short-term credit, which makes them vulnerable.18 To help arrest and fend off future bank runs, starting in the fall of 2008 the U.S. government stepped in with financial assistance. How Did We Get Here? There were several reasons why the U.S. financial industry got to the point where the government was propping up some of the countryâs largest banks with hundreds of billions of dollars in financial assistance. Among the most talked about were banking deregulation, increasingly close relations between Washington and Wall Street, and an influx of ânew moneyâ looking for investment. Deregulation and Derivatives As Andrew Lo emphasized in his 2008 testimony, there was a direct correlation between the loosening of regulations on banks during the late 1990s and early 2000s and the most recent financial crisis: The overall impact of relaxed constraints [created] an over-extended financial systemâpart of which was invisible to regulators and outside their direct controlâthat could not be sustained indefinitely. The financial system became so âcrowdedâ in terms of the extraordinary amounts of capital deployed in every corner of every investable market that the overall liquidity of those markets declined significantly. The implication of this crowdedness is simple: the first sign of trouble in one part of the financial system will cause nervous investors to rush for the exits, but it is impossible for everyone to get out at once, and this panic can quickly spread to other parts of the financial system.19 Many considered the repeal of the Glass-Steagall Act in 1999 to be one of the more critical regulatory changes that played a role in the financial crisis. Passed in 1933, the act (also known as the Banking 18 James Kwak, âFinancial Crisis for Beginners,â http://baselinescenario.com/financial-crisis-for-beginners/, accessed May 19, 2009. 19 Andrew W. Lo, âHedge Funds, Systemic Risk, and the Financial Crisis of 2007â2008: Written Testimony for the House Oversight Committee Hearing on Hedge Funds,â November 13, 2008, p. 9. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 7 Act) helped control abuse and the level of risk to investors by prohibiting any one institution from acting as both an investment bank and a commercial bank, or as both a bank and an insurer. Its repeal opened up competition among banks, securities companies, and insurance companies. Commercial lenders like Citigroup, which in 1999 was the largest U.S. bank by assets, were now allowed to underwrite and trade instruments such as mortgage-backed securities. Another act of deregulation that many believed hastened the financial crisis was the Commodity Futures Modernization Act. Signed into law in 2000, the act left much of the multi-trillion-dollar derivatives market unregulated. Derivatives were contracts whose value depended on the underlying value of something specific such as a stock, bond, currency, or commodity. (The value of the instrument âderivesâ from some underlying item.) Derivatives allowed money to flow more freely from those who had it to those who needed it. In addition to offering protection against the risk of financial loss, they offered âfairâ returns to high-dollar investors willing to take calculated risks.20 For banks that loaned out tens of billions of dollars, derivatives, theoretically, helped mitigate risk by protecting them in case loans defaulted. Mortgage-backed securities and credit default swaps (CDSs) were two types of derivatives that became quite popular during the housing boom. A mortgage-backed security was essentially a pool of mortgages that were bundled together and sold as tranches up the investment chain: from mortgage broker to private mortgage bank and then to a Wall Street investment house. Mortgage-backed securities became a popular investment tool because they were initially considered to be low riskâ since housing prices kept going upâwith high returns: an average mortgage would typically provide returns of 5% to 9% in interest per year. CDSs were insurance-like contracts typically used for municipal bonds, corporate debt, and mortgage securities that promised to cover losses on certain securities in the event of a default. The buyer of the credit default insurance would pay a premium over a period of time in return for being covered if losses occurred. CDSs were sold by banks, insurance agencies, hedge funds, pension funds, and other investment outlets as a way for banks to get credit risk off their books.21 With the growth of mortgage-backed securities in the early 2000s, CDSs exploded in popularity as a way to protect against potential default. As an industry insider noted, speculative investors, hedge funds, and others bought and sold CDS instruments without having any direct relationship with the underlying investment: âTheyâre betting on whether the investments will succeed or fail.â22 Because the CDS market was not regulated, contracts could be traded from investor to investor without any oversight to determine their value and ensure that the buyer had the resources to cover losses in case 20 Steve Jordan, âChancy Derivatives Also Have Good Side,â Omaha World-Herald, October 26, 2008. 21 Janet Morrissey, âCredit Default Swaps: The Next Crisis?â Time, March 17, 2008. 22 Ibid. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 8 of default. As Johnson explained, âCDSs are one of the things that create uncertainty in the banking sector; a bank may look healthy, but it may be counting on CDS payouts from banks that you canât see; you canât be sure itâs healthy, so you wonât lend to it.â23 In light of this more loosely regulated environment, banks which, according to Johnson, had became âproprietary trading rooms,â buying and selling securities for profit,24 became âtoo big to fail.â AIG and Bear Stearns both nearly imploded due to the investments they had made in CDSs. As one journalist wrote, âBanks have become so big and so leveraged that their balance sheets can exceed the gross domestic product of the country in which they are based.â25 Iceland was a case in point. Several domestic banks had combined âtoxicâ assets that were larger than the countryâs entire economy.26 Deregulation and the âexoticâ investment products that flourished brought the industry enormous wealth. According to Johnson, between 1973 and 1985, the financial sector never earned more than 16% of domestic corporate profits. By the 2000s, this figure reached 41%. Compensation shot up from 99% to 108% of the average for domestic private industries between 1948 and 1982, and to 181% in 2007.27 And with this wealth came political influence. Close Ties Another ingredient that helped create the mix that nearly brought the U.S. financial industry to its knees was the cozy relationship that had built up over the years between Wall Street and Washington. As Johnson noted, âOversize institutions disproportionately influence public policy; the major banks we have today draw much of their power from being too big to fail. [Wall Street] benefited from the fact that Washington insiders already believed that large financial institutions and free-flowing capital markets were crucial to Americaâs position in the world.â28 By the time of the crisis, 90% of all the money deposited in the United States was in 20 banks.29 It was no secret that Wall Street firms were big political contributors. The securities and investment industryâwhich included Goldman Sachs, Morgan Stanley, Merrill Lynch, Lehman, and Bear Stearnsâgave $97.7 million to federal political candidates during the 2004 election and $70.5 million for the 2006 congressional election.30 In addition to their financial contributions, there was a fair 23 James Kwak, âFinancial Crisis for Beginners,â http://baselinescenario.com/financial-crisis-for-beginners/, accessed May 19, 2009. 24 Ibid. 25 Peter Gumbel, âThe Meltdown Goes Global,â Time, October 20, 2008. 26 Ibid. 27 Simon Johnson, âThe Quiet Coup,â The Atlantic, May 2009. 28 Ibid. 29 Ira Glass, Adam Davidson, and Alex Blumberg, âBad Bank,â NPR: This American Life, February 27, 2009. 30 Ben Steverman and David Bogoslaw, âThe Financial Crisis Blame Game,â BusinessWeek, October 20, 2008. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 9 amount of âinterweaving of career tracksâ31 between the two sectors. Goldman Sachs had been given the moniker âGovernment Sachsâ for the disproportionate number of executives who were taking public-sector jobs, including Henry Paulson, who had been CEO of Goldman from 1998 to 2006 and who was named Treasury secretary under President George W. Bush; Robert Rubin, who was cochairman when he was tapped to serve as Treasury secretary under President Bill Clinton; and Jon Corzine, governor of New Jersey, who served as CEO during the majority of the 1990s. As one industry observer remarked, âIt is a widely held view within the bank that no matter how much money you pile up, you are not a true Goldman star until you make your mark in the political sphere.â32 A spokesman for Goldman noted, âWeâre proud of our alumni, but frankly, when they work in the public sector, their presence is more of a negative than a positive for us in terms of winning business. There is no mileage for them in giving Goldman Sachs the corporate equivalent of most-favored-nation status.â33 New Money Looking for Investment At the same time that U.S. banking regulations were easing, the middle class in emerging markets such as China and India was growing at a phenomenal rate. As a result of this economic growth, the âglobal pool of moneyâ doubled from $36 trillion in 2000 to $70 trillion in 2008. One economist observed, âThe world was not ready for all this money. Thereâs twice as much money looking for investments, but there are not twice as many good investments.â34 What was once considered a safe and profitable investment, U.S. Treasury bonds, was no longer appealing as the federal funds rate that was 6.5% for much of 2000 dropped below 2% in 2003.35 Enter mortgage-backed securities. As one executive director at Morgan Stanley recalled, it didnât take long for mortgage-backed securities, which offered returns ranging from 5% to 9%, to become the financial industryâs new favorite investment tool: It was unbelievable. We almost couldnât produce enough to keep the appetite of the investors happy. More people wanted bonds than we could actually produce. They would call and ask, âDo you have any more fixed rate? What have you got? Whatâs coming?â From our standpoint, itâs like, thereâs a guy out there with a lot of money. We gotta find a way to be his sole provider of bonds to fill his appetite. And his appetiteâs massive.36 By 2003, the demand for mortgage-backed securities began outstripping supply, and the mortgage industry needed to ramp up production. It was at this point that the guidelines for getting a mortgage 31 Simon Johnson, âThe Quiet Coup,â The Atlantic, May 2009. 32 Julie Creswell and Ben White, âThe Guys From âGovernment Sachsâ,â The New York Times, October 17, 2008. 33 Ibid. 34 Ira Glass, Adam Davidson, and Alex Blumberg, âThe Giant Pool of Money,â NPR: This American Life, May 9, 2008. 35 Ben Steverman and David Bogoslaw, âThe Financial Crisis Blame Game,â BusinessWeek, October 20, 2008. 36 Ira Glass, Adam Davidson, and Alex Blumberg, âThe Giant Pool of Money,â NPR: This American Life, May 9, 2008. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 10 loosened considerably. Mortgages for $400,000 were being given to people who did not have to provide proof of income or assets. One person in the industry quipped, âYou [didnât] have to state anything. [You] just [had] to have a credit score and a pulse.â37 Equity lines of credit also were being sold at an alarming rate, allowing people to take out another loan from the bank against the value of their house, which for many was worth more than what they had paid for it. The banks did not care how risky these loans were because they would own them for a few weeks, then sell them up the chain to Wall Street, and Wall Street would in turn sell them on to the âglobal pool of money.â But up until 2005, the risk was considered minimal because the value of homes in the United States kept going up. If someone defaulted on their loan, the bank would then own the home that was worth more than it was when the loan was first made. 38 But the housing bubble burst, prices took a downward turn, and with it the economy followed. As one journalist put it, âWith all the brainpower on Wall Street, few made the connection between the trillions of dollars in real estate assets held by financial firms and what would happen if the value of those assets suddenly dropped.â39 Who Is to Blame? Finger pointing over who was to blame had run amok and by early 2009 had become a ânational pastimeâ40 of sorts. Commercial and investment banks, mortgage lenders, credit-rating agencies, insurance companies, regulators, politicians, government-sponsored entities, investors, and homeowners all played a role. Many people believed that those in senior management positions in banks and investment firms were largely to blame for not understanding the highly complex models devised by their quantitative analysts or âquants,â and for their inability to properly manage how and the degree to which those models became highly sought-after products in the market.41 Some blamed the quants for creating financial instruments that were simply too complicated for those in senior management to understand. Still others blamed the regulators. In 2004, the SEC had loosened leverage (debt) rules for investment banks, and by 2008 many were plagued by leverage ratios that were 30 to 40 times, as opposed to 10 to 15 times, their core holdings.42 Others pointed to the lack of relevant expertise that existed within the halls of the SEC. As Lo explained, the SEC was staffed with lawyers who âdonât have the kind of training thatâs necessary to be able to deal with some of these more complex kinds of strategies.â43 37 Ira Glass, Adam Davidson, and Alex Blumberg, âThe Giant Pool of Money,â NPR: This American Life, May 9, 2008. 38 Ibid. 39 Ben Steverman and David Bogoslaw, âThe Financial Crisis Blame Game,â BusinessWeek, October 20, 2008. 40 Ibid. 41 Ira Flatow, âDoes Wall Street Need More Physicists?â NPR: Talk of the Nation/Science Friday, March 13, 2009. 42 Ben Steverman and David Bogoslaw, âThe Financial Crisis Blame Game,â BusinessWeek, October 20, 2008. 43 Ira Flatow, âDoes Wall Street Need More Physicists?â NPR: Talk of the Nation/Science Friday, March 13, 2009. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 11 Many blamed politicians for repealing Glass-Steagall. As Lo testified, the repeal of Glass-Steagall fueled growth in shadow banking44 institutions like hedge funds. Hedge funds, he explained, were among the most secretive of financial institutions because: Their franchise value was almost entirely based on the performance of their investment strategies, and this type of intellectual property was perhaps the most difficult to patent. Therefore, hedge funds have an affirmative obligation to their investors to protect the confidentiality of their investment products and processes. It is impossible, therefore, to determine their contribution to systemic risk.45 While most analysts did not believe that hedge funds caused the current crisisâafter all, hedge funds did do good things including raising tens of billions of dollars since the mid-2000s for infrastructure investments in India, Africa, and the Middle Eastâthey were heavy investors in risky mortgagebacked securities.46 Government-sponsored enterprises Fannie Mae and Freddie Mac also shared the blame. These institutions, which had a charter from Congress with a mission of supporting the housing market, were responsible for purchasing and securitizing mortgages in order to ensure that funds were consistently available to the institutions that lent money to home buyers. As private companies with close ties to the government, Fannie and Freddie could borrow money at relatively low interest rates.47 Pressured by Congress to increase lending to lower-income borrowers back in the mid-1990s, Fannie and Freddie began lowering credit standards and purchased or guaranteed âdubiousâ home loans. What Now? As the full force of the financial crisis hit in October 2008, one month before the U.S. presidential election, there was heated debate in Congress over what to do. There was a call for doing nothing and letting the markets âwork themselves out.â After all, that was how capitalism was supposed to work, and having the government step in and help was a form of socialism. Federal Reserve Chairman Ben Bernanke believed that doing nothing would be catastrophic, and told Congress, âIf we let the banking system fail, no one will talk about the Great Depression anymore, because this will be so much worse.â48 44 Shadow banking system: consists of investment banks, hedge funds, mutual funds, insurance companies, pension funds, endowments and foundations, and various broker/dealers that provide many of the same services as banks but are outside the banking system and therefore are not controlled by regulatory bodies. The shadow banking system grew rapidly after the repeal of the Glass-Steagall Act of 1999. 45 Andrew W. Lo, âHedge Funds, Systemic Risk, and the Financial Crisis of 2007â2008: Written Testimony for the House Oversight Committee Hearing on Hedge Funds,â November 13, 2008, p. 8. 46 Ellen Nakashima, âThe Year Hedge Funds Got Hit,â The Washington Post, January 3, 2009. 47 James R. Hagerty, âThe Financial Crisis: Bailout Politics,â The Wall Street Journal, October 16, 2008. 48 Ira Glass, Adam Davidson, and Alex Blumberg, âBad Bank,â NPR: This American Life, February 27, 2009. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 12 Toward the end of President George W. Bushâs second term in office and continuing with incoming President Barack Obama, the U.S. government was doing several things to stop the bleeding and put the country on a path to recovery. First, in October 2008 the government gave certain banks and other financial institutions considerable amounts of money from its Troubled Asset Relief Program (TARP). Citigroup, for example, received $45 billion; Bank of America, $25 billion; and AIG, $180 billion. These loans came with certain restrictions, in particular pertaining to executive compensation, which were expanded under the new Obama administration (Exhibit 1). The hope was that this money would help stabilize balance sheets to the point where banks would start to lend money again and the credit markets would begin to loosen up. Months after the money had been given, however, many banks still were not scaling up their lending as originally anticipated. Instead, they were holding on to the money they received in order to build up their capital and make their balance sheets healthy again. As a number of economists pointed out, unhealthy banks should loan less, not more. After all, excessive lending was how the U.S. banking industry got to where it was in the first place.49 Second, in early 2009, Treasury Secretary Timothy Geithner introduced the Public Private Investment Program, which was established to purchase real estate-related loans from banks and the broader market. Financing in the amount of $500 billion had been set aside to subsidize private investors interested in buying pools of the âtoxicâ loans. The value of the loans and securities purchased under the program was to be determined by the private-sector buyers. Finally, around the same time that the Public Private Investment Program was introduced, Geithner announced that 19 of the nationâs largest banks (those with $100 billion or more in assets) would be subjected to a stress test, also known as a capital assessment. The purpose of the test was to determine if the countryâs largest banks had sufficient capital buffers to withstand a further economic downturn. Each participating financial institution was asked to analyze potential firm-wide losses, including those in its loan securities portfolios, as well as those from any off-balance-sheet commitments and contingent liabilities and exposures, under two different economic scenariosâscenarios that many felt were âoverly rosyâ50âduring a two year period. (See Figure 3 for economic scenarios.) Participating financial institutions also were instructed to forecast the internal resources available to absorb losses, including pre-provision net revenue and the allowance for loan losses. Supervisors (as named by the U.S. Federal Reserve) would meet with senior management at each participating institution to review and discuss loss and revenue forecasts.51 49 Ibid. 50 Deborah Solomon, David Enrich and Damian Paletta, âBanks Need at Least $65 Billion in Capital,â The Wall Street Journal, May 7, 2009. 51 http://www.FDIC.gov/news/news/press/2009/pr09025a.pdf. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 13 Figure 3 Economic Scenarios for Bank Stress Tests Source: FAQs â Supervisory Capital Assessment Program, http://www.FDIC.gov/news/news/press/2009/pr09025a.pdf. The initial reaction of many to the tests was one of great suspicion that nationalization of the banks would be the next step. However, the results announced in May indicated that the banks were healthier than anticipated. There was widespread belief that most if not all of the banks would be able to boost their capital without needing additional government funds. They could achieve this by raising money privately, selling shares to the public, selling parts of their business, or converting preferred shares into common shares, a move that would increase tangible common equity without providing banks any new cash. One bank analyst called such a measure âwindow dressingâ in that it would not add one extra dollar to a bankâs capital buffer against losses: âItâs just moving capital from one place to another.â52 If such a measure were taken, the government (and therefore taxpayers) would go from being lenders to part owners. The governmentâs multi-prong approach had its share of critics, Simon Johnson among them. In his mind, there was a seeming unwillingness to upset the financial sector: The âstressâ scenario used by the government turns out to be a mild and short-lived downturn, so the tests were effectively designed to allow everyone to pass. Actual official outcomes for each bank are the result of complicated closed-door negotiations, and at the bank level all we have learned is who has more or less political power.53 Consumers and businesses are still dependent on banks that lack the balance sheets and the incentives to make the loans the economy needs, and the government has no real control over 52 Edmund L. Andrews, âBanks Told They Need $75 Billion in Extra Capital,â The New York Times, May 8, 2009. 53 âGrading the Banksâ Stress Test,â The New York Times, May 6, 2009. 2009 2010 Real GDP Average Baseline -2.0 2.1 Alternative More Adverse -3.3 0.5 Civilian Unemployment Rate Average Baseline 8.4 8.8 Alternative More Adverse 8.9 10.3 House Prices Average Baseline -14 -4.0 Alternative More Adverse -22 -7.0 THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 14 who runs the banks, or over what they do.54 The government is dictating how GM needs to start behaving, but it is not doing it with the banks. There is asymmetry in how the financial sector is being treated and how manufacturing is being treated. The government is not afraid of manufacturing going into bankruptcy, but they are afraid of finance going into bankruptcy.55 Johnson believed that the administrationâs current deal-by-deal strategy, whereby what was done for one bank was different than what was done for another, would not work: âYou donât know what the rules are. Itâs complete chaos and confusion.â56 Johnson proposed that âyou do it once and for all. You do it systematically. You have very clear rules that are pre-announced.â57 Reflecting back to his years as chief economist at the IMF, Johnson asked rhetorically: What would the U.S. tell the IMF to do if this were any country other than the U.S.? If you covered up the name of the country, and just showed me the numbers, just show me the problems, talk to me a little about the politics in a generic way. With the financial system, you have a boom, and then a crash.... I know what the advice would be, and that would be, taking over the banking system. Clean it up; re-privatize it as soon as you can.58 Johnson feared that by not responding to the crisis in a more consistent, systematic way, the United States could go in the direction of the Japanese banking system during the 1990s. The IMFâs advice that the Japanese government take over the banks; break them up into healthy, functioning smaller operations; and re-privatize them fell on deaf ears. What arose instead were âzombie banks,â or banks that were allowed to keep operating even though they had massive debts.59 The 1990s were considered Japanâs lost decade, when economic growth was stagnant. Recognizing that the word ânationalizationâ was a red flag, Johnson was calling for a âgovernmentmanaged bankruptcy programâ or âgovernment-run receivershipâ in which the toxic assets of banks were put into a separate entity and then the healthy parts were broken down and sold off in smaller chunks to the private sector. Johnson repeatedly made the point that these were the exact actions the IMF had taken many times with emerging marketsâincluding Korea, Indonesia, Russia, and Argentina after their respective financial meltdowns in the late 1990s and early 2000s. Breaking down the banks into local or regional entities also would break up the banking âoligarchyâ that Johnson believed played a central role in creating the crisis: âBy selling off the banks into smaller, more concentrated ownership stakes, you will get more powerful owners who will hold management accountable.â60 54 Simon Johnson, âThe Quiet Coup,â The Atlantic, May 2009. 55 Interview with the case writer, April 7, 2009. 56 Ibid. 57 Ibid. 58 Ira Glass, Adam Davidson, and Alex Blumberg, âBad Bank,â NPR: This American Life, February 27, 2009. 59 Terry Gross, âSimon Johnson On Bank Bailout Plan,â NPR: Fresh Air, March 3, 2009. 60 Interview with the case writer, April 7, 2009. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 15 Keeping the banks under government control long term was not something that Johnson advocated: How much do you enjoy going to get your driverâs license renewed, going to the DMV, or, even worse, moving to a new state and having to get a new driverâs license? The government does [not do] a very good job of managing things as simple as a driverâs license, and certainly something as complicated as a bank would almost certainly not go well at all.61 Of course some people will complain about the âefficiency costsâ of a more fragmented banking system, and these costs are real. But so are the costs when a bank that is too big to failâa financial weapon of mass self-destructionâexplodes. Anything that is too big to fail is too big to exist.62 A loud contingent of economists, politicians, and business leaders believed that nationalizing banks was a âcrime against the capitalist system.â Johnson thought otherwise: âMy view is [that] the offense against American capitalism was committed by the big banks who brought us to this point: Their mismanagement, their compensation schemes, their attitude towards the public.â63 The governmentâs priority, he believed, should be to protect the payment system: âYou want to protect deposits and anything that is like a deposit. If you force people to take losses on the payments part of the system, then all hell is going to break loose.â64 Several hurdles needed to be cleared if the government was to take the route advocated by Johnson. First, there was a manpower issue. One expert predicted that it would take thousands of people for each bank takeover. A second problem had to do with timing. As Columbiaâs Beim noted: Nationalizations are kind of like potato chips. Itâs hard just to have one. Youâd have to come out with a plan for all of the banks, and youâd have to do the whole thing in one day, at one time. Because if you just start taking over one bank, people with money at other banks will start worrying that their bank will be nationalized next, and that will cause investors to panic and theyâll pull all their money out of that bank.65 When it came time to re-privatize, the question was whether there was enough well-capitalized demand for all the potential supply. As one economist pointed out, âFinding enough private equity to 61 Terry Gross, âSimon Johnson On Bank Bailout Plan,â NPR: Fresh Air, March 3, 2009. 62 Simon Johnson, âThe Quiet Coup,â The Atlantic, May 2009. 63 Terry Gross, âSimon Johnson On Bank Bailout Plan,â NPR: Fresh Air, March 3, 2009. 64 Andrew Leonard, âSimon Johnson Says: Break Up the Banks,â Salon.com, April 28, 2009. 65 Ira Glass, Adam Davidson, and Alex Blumberg, âBad Bank,â NPR: This American Life, February 27, 2009. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 16 buy one bank would not be a problem. Finding enough money to buy all the banks was another story.â66 In addition to the logistical hurdles, Johnson noted, there would inevitably be a lot of political resistance: The politics are awkward. Cleaning up a banking system, in my view, technically, is not that difficult. But when you clean up a banking system, and you do it properly, some powerful people lose. They lose their bonuses, they lose their banks, they lose their access; so who is going to lose? Who is going to decide who is in and who is out? I donât think the people at the top are yet ready to have that conversation.67 Long Term In his November 2008 testimony to the House Oversight Committee Hearing on Hedge Funds, Andrew Lo made a number of recommendations for regulatory reforms and other changes to prevent and/or soften the landing the next time a bank crisis hits. Effective Regulation Unlike many economists, Lo believed that financial markets didnât need more regulation, but rather more effective regulation that provided greater transparency: As a general principle, the more transparency is provided to the market, the more efficient are the prices it produces, and the more effectively will the market allocate capital and other limited resources. When the market is denied critical information, its participants will infer what they can from existing information, in which case rumors, fears, and wishful thinking will play a much bigger role in how the market determines prices and quantities.68 The current financial crisis is a mystery, and concepts like subprime mortgages, CDOs, CDSs, and the âseizing upâ of credit markets only create more confusion and fear. A critical part of any crisis management protocol is to establish clear and regular lines of communication with the public, and a dedicated interagency team of public relations professionals should be formed for this express purpose.69 Lo believed that more information was needed on the shadow banking system, particularly hedge funds. As he explained in his testimony, âWithout access to primary sources of dataâdata from 66 Ibid. 67 Ibid. 68 Andrew W. Lo, âHedge Funds, Systemic Risk, and the Financial Crisis of 2007â2008: Written Testimony for the House Oversight Committee Hearing on Hedge Funds,â November 13, 2008, p. 21. 69 Ibid., p. 2. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 17 hedge funds, their brokers, and counterpartiesâit is simply not possible to derive truly actionable measures of systemic risk.â70 Lo recommended that hedge funds with more than $1 billion in gross notional exposures provide regulatory authorities with confidential information on a regular basis on the following: assets under management, leverage, portfolio holdings, list of credit counterparties, and list of investors. Lo believed that the confidentiality aspect of the information was critical: âIf hedge funds are forced to reveal their strategies, the most intellectually innovative one will simply cease to existâ¦. This would be a major loss to U.S. capital markets and the U.S. economy, hence it is imperative that regulators tread lightly with respect to this issue.â71 One change Lo proposed was to provide the public with information on financial institutions that had failed: âIt is unrealistic to expect that market crashes, manias, panics, collapses, and fraud will ever be completely eliminated from our capital markets, but we should avoid compounding our mistakes by failing to learn from them.â72 In his testimony, Lo called for the creation of a Capital Markets Safety Board (CMSB), an independent investigatory review board similar to that of the National Transportation and Safety Board, an independent government agency that investigates accidents. âThe financial industry can take a lesson from other technology-based professions,â Lo argued. âIn the medical, chemical engineering, and semiconductor industries, for example, failures are routinely documented, catalogued, analyzed, internalized, and used to develop new and improved processes and controls. Each failure is viewed as a valuable lesson to be studied and reviewed until all the wisdom has been gleaned from itâ¦.â73 Every completed investigation would produce a publicly available report documenting the details of each failure and recommendations for avoiding similar future outcomes. In addition to investigating financial âblow-ups,â a CMSB would be responsible for obtaining and maintaining information on the shadow banking system, including hedge funds and private partnerships, and integrating this information with other regulatory agencies. The CMSB would act as a single agency responsible for managing data relating to systemic risk. New Accounting Methods Lo also believed that accounting methods needed to take risk into account. Current accounting methods (e.g., Generally Accepted Accounting Principles or GAAP) were backward looking, focused on value resulting from revenue and costs that had already occurred, and not risk: âAccountants tell us what has happened, leaving the future to corporate strategists and fortunetellers.â74 In Loâs view, accounting methods needed to be counterbalanced with something he referred to as a ârisk balance 70 Ibid., p. 7. 71 Ibid., p. 8. 72 Ibid., p. 21. 73 Ibid., p. 18. 74 Andrew W. Lo, âHedge Funds, Systemic Risk, and the Financial Crisis of 2007â2008: Written Testimony for the House Oversight Committee Hearing on Hedge Funds,â November 13, 2008, p. 24. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 18 sheetâ: the risk decomposition of a firmâs mark-to-market balance sheet where both assets and liabilities were considered to be random variables. âSince assets must always equal liabilities,â he explained, âthe variance of assets must always equal the variance of liabilities, hence the risk balance sheet is just the variance decomposition of both sidesâ¦. Risk accounting standards must address both the proper methods for estimating the variances and covariances of assets and liabilities, and the potential instabilities in these estimates across different economic environments.â75 Corporate Governance According to Lo, the single most important implication of the financial crisis was corporate governance: Many corporations did a terrible job in assessing and managing their risk exposures, with some of the most sophisticated companies reporting tens of billions of dollars in losses in a single quarter. How do you lose $40 billion in a quarter and then argue that youâve properly assessed your risk exposure? I donât think itâs credible to say it was just bad luck. If troubled companies want to explain away 2008 as a âblack swan,â then someone should take responsibility for creating the oil slick that seems to have tarred the entire flock. The current crisis is a major wake-up call that we need to change corporate governance to be more risk sensitive.76 As a way to increase risk sensitivity, Lo believed quants were needed in management positions and at the board of director level where they would be a part of the decision-making process. He explained that the absence of quants from top management was due to the fact that their specialty did not exist when those in top management began their careers. In other words, there was a generational gap that needed to be filled. In his mind, the lack of quants in the decision-making process made no sense: âCan you imagine a board of directors of a hospital not having a few doctors or a technology firm not having a few technology experts? It doesnât make sense, and itâs got to change.â77 Lo also believed that the role of risk officers and how they were compensated needed to change. He argued that the direct reporting relationship between risk officers and CEOs created conflicts of interest and that those heading up risk management efforts should report directly to the board of directors. How risk managers were compensated also needed to change: âWhy is a risk manager paid the same way as a CEO? They should be compensated based on their ability to keep the company stable, not on how much money the company makes.â78 In Loâs mind, reforms at the corporate governance level included distancing Wall Street from Washington. âPoliticians rely on corporate America for their campaign contributions,â he noted. âNo 75 Ibid., p. 24. 76 Andrew W. Lo, âUnderstanding Our Blind Spots,â The Wall Street Journal, March 23, 2009. 77 Interview with the case writer, April 10, 2009. 78 Ibid. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 19 one wants to deal with it, but it must be dealt with. Corporations should not be allowed to make contributions to political campaigns. Period. Weâll never get past this conflict of interest unless we make this across-the-board change.â79 Education According to Lo, finance education clearly needed to be addressed, particularly the knowledge gap that existed between quants and those in senior management positions: We often take it for granted that large financial institutions capable of hiring dozens of âquantsâ each year must have the technical expertise to advise senior management, and senior management has the necessary business and markets expertise to guide the quantitative research process. However, in fast-growing businesses the realities of day-to-day market pressures make this idealized relationship between senior management and research a fantasy. Senior management typically has little time to review the research, much less guide it; and in recent years, many quants have been hired from technically sophisticated disciplines such as mathematics, physics, and computer science but without any formal training in finance or economics.80 Lo believed that Wall Street needed more scientists: âThe problem is not that there are too many physicists on Wall Street, but that there are not enough.â81 He recalled one investment banker telling him that Wall Street was not looking for Ph.D.s, but rather P.S.D.sâpoor, smart, and a deep desire to get rich.82 In his testimony, Lo called for government funding to expand the number of Ph.D. programs in financial technology. Conclusion By spring 2009, the collateral damage from the financial crisis was still unknown. It would take time before anyone knew the real value of the âtoxic assetsâ that were plaguing the banking system. Furthermore, personal credit card debt had yet to hit. When it did, many economists believed the downward spiral could re-ignite, sending unemployment into the double digits and the stock market well below 6,000. It was also unknown whether the governmentâs plan to rescue the financial system would work. Simon Johnson and Andrew Lo were advocating measures that they believed would solve the current crisis and make the next one less severe. Whether and how the government would implement their recommendations was uncertain. 79 Ibid. 80 Andrew W. Lo, âHedge Funds, Systemic Risk, and the Financial Crisis of 2007â2008: Written Testimony for the House Oversight Committee Hearing on Hedge Funds,â November 13, 2008, p. 27. 81 Interview with the case writer, April 10, 2009. 82 Dennis Overbye, âThey Tried to Outsmart Wall Street,â The New York Times, March 10, 2009. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 20 Besides the fact that financial crisesâin the United States and elsewhereâwould happen again, Lo noted that the financial industry was in a state of flux. For young people studying finance, the industry held a lot of promise: I look at this as an incredible opportunity for those who want to get into finance. Periods of crisis breed opportunity. There will be many opportunities in the next five to 10 years to create new financial technologies to help us prevent this level of crisis. The industry will not be what it was. Compensation will not be the same. There has to be a paradigm shift in how we think about financial markets, both from a financial technology point of view and the human side.83 83 Interview with the case writer, April 10, 2009. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 21 Exhibit 1 Highlights of Expanded Restrictions for TARP Recipients Bonus Retention and Incentive Compensation. TARP recipients are prohibited from paying bonuses, retention awards, and incentive compensation until the financial institutions satisfy their TARP obligations. Executives subject to compensation restrictions depend upon the amount of TARP assistance received: Amount of TARP Assistance Covered Executives Less than $25 million Most highly paid employee $25 million to $250 million Five most highly paid employees More than $250 million to $500 million Senior executive officers (SEOs)* and next 10 most highly paid employees More than $500 million SEOs and next 20 most highly paid employees *SEOs include the top five most highly paid officers. Long-term Restricted Stock. TARP recipients may provide long-term restricted stock so long as: ⢠The covered executive does not fully vest in the restricted stock during the TARP period; ⢠The value of the restricted stock does not exceed one-third of the covered executiveâs âtotal amount of annual compensationâ; and, ⢠The restricted stock complies with such other restrictions as the Treasury Department may impose. Pre-existing Employment Contracts. The restrictions on payment of bonuses and incentive compensation do not apply to amounts paid pursuant to a written employment contract entered into on or before February 11, 2009. Incentive Compensation for Risk Taking and Earnings Manipulation. TARP recipients are prohibited from paying incentive compensation for âunnecessary and excessive risksâ and earnings manipulation. Golden Parachutes (benefits promised to an employee upon termination of employment). TARP recipients are prohibited from paying golden parachute payments to the SEOs and any of the next five most highly paid employees. There is no exception for pre-existing employment contracts. Clawbacks. TARP recipients must take clawback bonus, retention, and incentive compensation for the SEOs and the next 20 most highly paid employees if payments were made on inaccurate performance criteria. THE GLOBAL FINANCIAL CRISIS OF 2008: THE ROLE OF GREED, FEAR, AND OLIGARCHS Cate Reavis Rev. March 16, 2012 22 Luxury Expenditures. The Board of Directors of each TARP recipient must establish a policy on luxury or excessive expenditures, including entertainment or events, office and facility renovations, company-owned aircraft and other transportation, and similar activities or events. âSay on Pay.â TARP recipients must provide shareholders with a non-binding advisory âsay on payâ vote on executive pay. IRC Section 162(m) Deduction Limit. TARP recipients are prohibited from deducting more than $500,000 in annual compensation from the CEO, the CFO, and the three next most highly paid officers under Internal Revenue Code Section 162(m). Compensation Committee Governance. The Board of Directors of each TARP recipient must establish a compensation committee to review compensation plans. The compensation committee must consist entirely of independent directors. This restriction does not apply to private companies that receive less than $25 million in TARP assistance. CEO and CFO Certification. The CEO and CFO must certify compliance with the requirements noted above. For public companies, certification must be made to the SEC. For private companies, certification must be made to the Treasury Department. Treasury Department Review of Bonus Payments. The Treasury Department is directed to review bonuses to the SEOs and the next 20 most highly paid employees paid before February 18, 2009. If the Treasury Department finds the bonuses were not justified, it will negotiate with the TARP recipient and/or executive to obtain reimbursement of the bonus. TARP Fund Repayment. TARP recipients may repay TARP funds without replacing the repaid amount with other funds and without a waiting period. If the amounts are repaid, the restrictions on executive compensation would cease to apply. Source: Marjorie M. Glover, Rachel M. Kurth, â2009 American Recovery and Reinvestment Act,â