ECO105Y1 Chapter Notes - Chapter 4: Old Navy, Profit Margin, Shortage

Document Summary

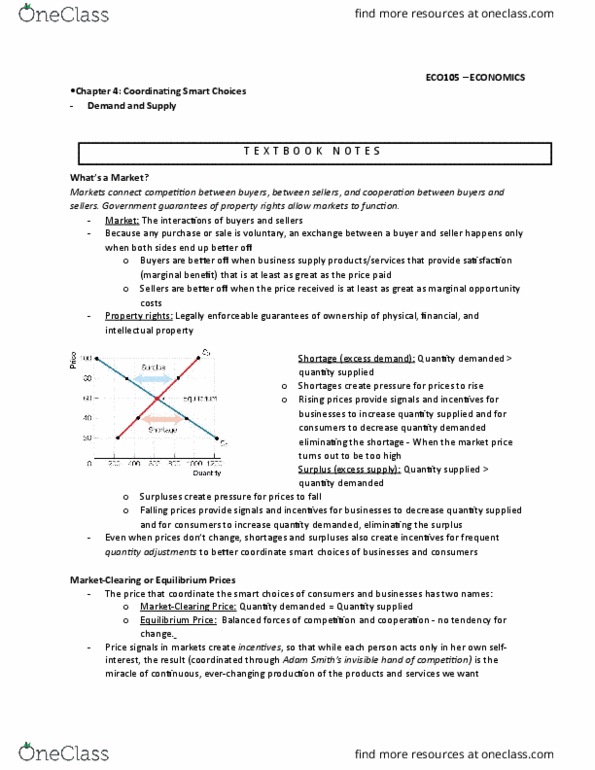

Chapter 4: coordinating smart choices (demand and supply) 4. 1- describe how buyers and sellers compete and cooperate in markets. 4. 2- explain how shortages and surpluses affect prices. 4. 3- identify how market-clearing prices coordinate the smart choices of consumers and businesses. 4. 4- illustrate how changes in demand and supply affect market-clearing price and quantities. 4. 1 what"s a market: what is a market, you are negotiating with a car dealer over the price of a new car. If so, what arguments do you use to counter riaa"s defense of property rights. What actions might old navy take: most provincial parks charge a fixed price for a camping permit, and allow you to reserve specific campsites well in advance. By the time a summer holiday weekend arrives, all the permits are taken. There is excess demand, and no price adjustment. 4. 3 when prices sit still: market-clearing prices balancing quantity demanded and.