RSM222H1 Chapter Notes - Chapter 4: Weighted Arithmetic Mean, Microsoft Powerpoint, Indian Railways

7 Apr 2013

School

Department

Course

Professor

Document Summary

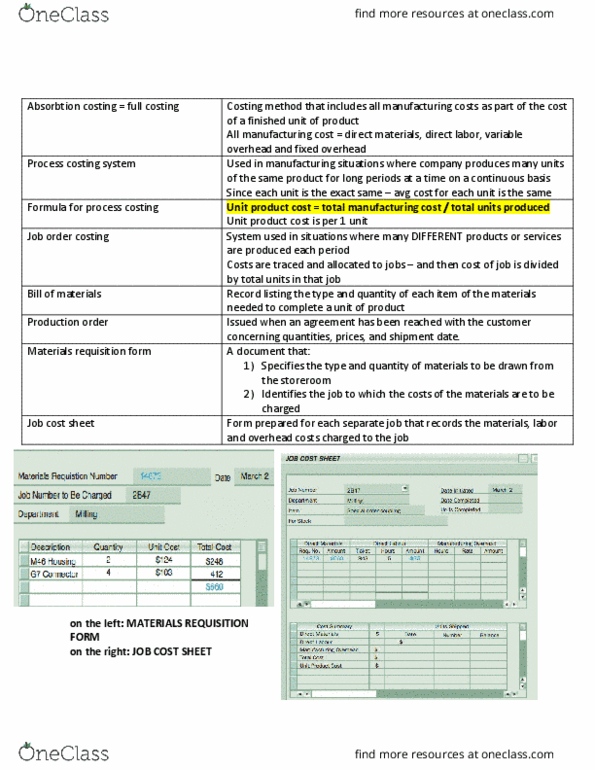

The differences between these two costing systems is: the flow of units in a process costing system is more or less continuous, these units are indistinguishable from one another. Job cost sheet is not used a process costing, says the focal point of that market is department. ** exhibit 4. 1 differences between job order and process costing** Processing departments: any location in an organization where work is performed on a product and where materials, labor, or overhead costs are added to the product. A company has as many or as few processing departments as are needed to complete a product or service. All processing departments have two essential features: the activity performed in the processing department must be performed uniformly on all of the units passing through it, the output of the processing department must be identical. The flow of materials, labor, and overhead costs.