RSM324H1 Chapter Notes - Chapter 6: The Employer, Remittance

15 Feb 2017

School

Department

Course

Professor

Document Summary

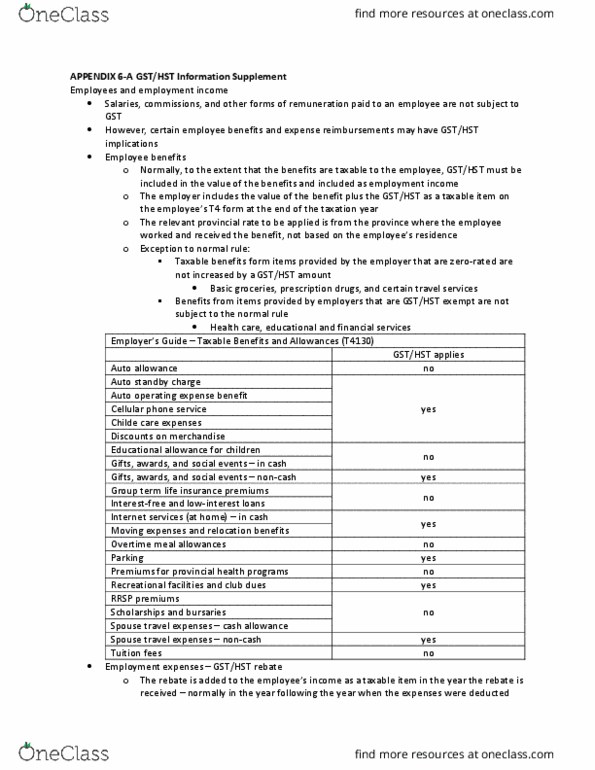

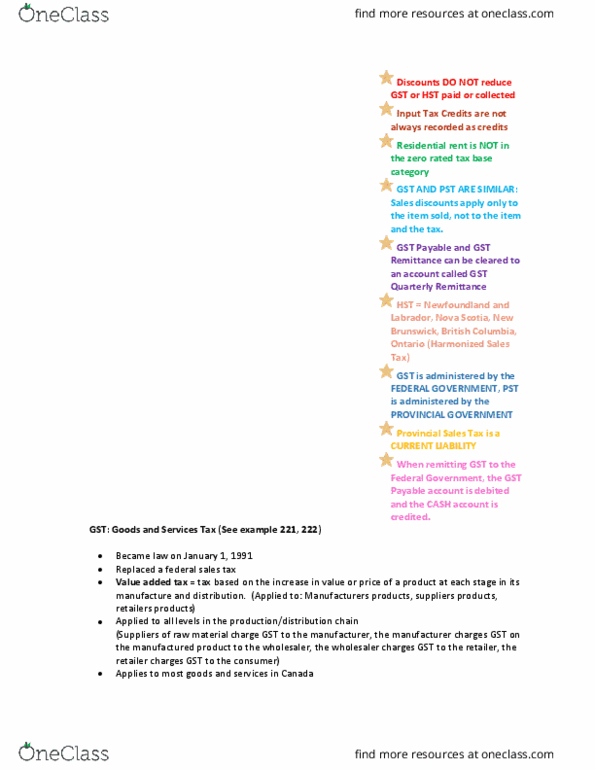

All gst/hst registrants are required to collect and remit the gst/hst on all sales of goods and services other than zero-rated and exempt items. In addition, registrants can obtain an input credit for goods and services acquired. Timing of tax and input credits: the gst/hst is due on the sale of taxable goods and services and, therefore, is eligible for remittance on the earliest of: The date of the invoice or the day the invoice is first issued. The day the invoice would normally have been issued but for an undue delay. The day on which the payment became due pursuant to a written agreement. Input credits do not have to be claimed in the period they occur. Instead, they can be claimed anytime within 4 years form the date the gst/hst was paid. 5/105 of the amount owing for the gst and the appropriate ratio for the hst (13/113 in.