ACCT 2520 Chapter Notes - Chapter 15: Net Income, Stock Split, Treasury Stock

16 Mar 2017

School

Department

Course

Professor

Document Summary

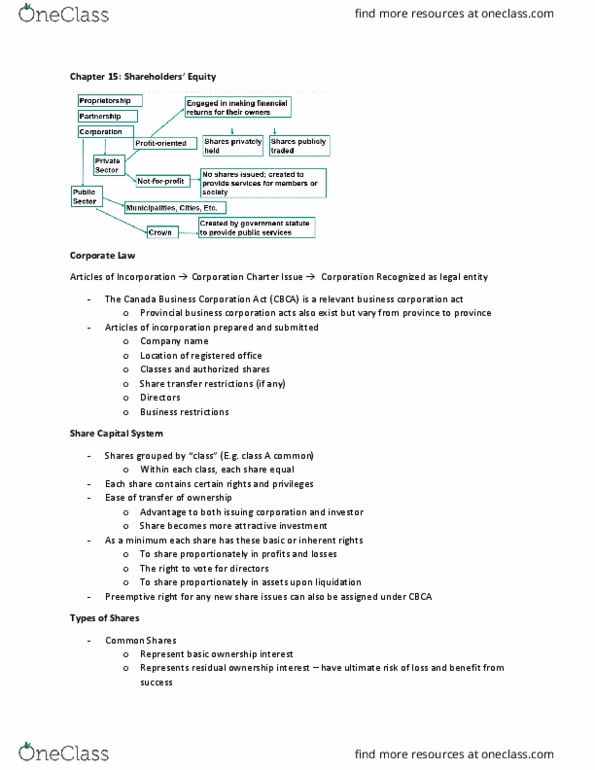

Dividends: two classes, return on capital (share of earnings, return of capital (liquidating dividends) Non-cumulative and non-participating shares: dividends are distributed only when declared, up to the stated amount of the share, no amount is paid for years where dividends were not declared. Cumulative and non-participating shares: the dividends that were not paid to preferred shareholders in the previous years must also be paid. Stock dividends vs. stock splits: stock dividend, a type of dividends, both the number of shares and the amount of chare capital is affected, shares are not exchanged, stock split. Increases the number of shares outstanding: amount of share capital is not affected, results in a market price per share change. Contributed surplus transactions: par value share issue and/or retirement, treasure share transactions, liquidating dividends, financial reorganization, stock options and warrants, share subscriptions forfeited, donated assets by a shareholder, redemption or conversion of shares.