ACCT 2550 Chapter Notes - Chapter 9: Target Costing

20 Nov 2016

School

Department

Course

Professor

Document Summary

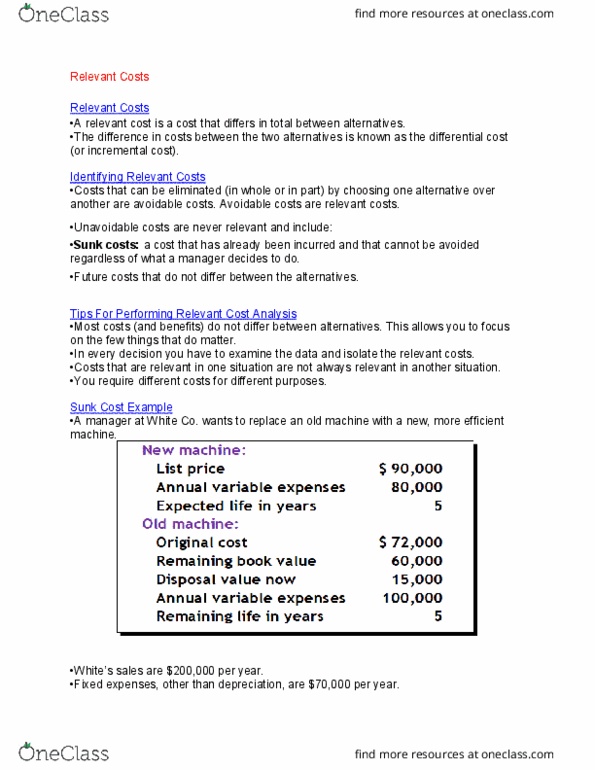

Relevant costs costs that differ between alternatives. Identifying relevant costs and benefits: differential cost the difference in costs between two alternatives, avoidable cost can be eliminated in whole or in part by choosing one alternative over the other, characteristics of relevant costs. They are costs that will be incurred in the future: steps to identify costs that are avoidable/differential. Eliminate costs and benefits that do not differ between alternatives (sunk and future costs) Use remaining costs and benefits that do differ in making the decision. A decision about whether to produce a fabricated part internally or buy the part externally from a supplier. A one-time order that is not considered part of the company"s normal ongoing business. Target costing provides an alternative, market-based approach to pricing new products. Management estimates how much the market will be willing to pay for the new product even before it has been designed.