STEN 1000 Chapter Notes - Chapter 13: Capital Structure, Profit Margin, Initial Public Offering

20 Jun 2018

School

Department

Course

Professor

CHAPTER 13 – UNDERSTANDING BUSINESS FINANCES

Fundamentals of Financial Analysis

Five key areas (fig. 13.1)

1. Revenue Model

- Sales revenue = per unit selling price x quantity sold

- Managers need to analyse the underlying trends impacting the revenue model - whether

these trends will assist in growing revenue, or reduction in revenue

- What percentage of total sales and revenue does each product represent

2. Cost Structure and Drivers

- Cost base – total costs associated with delivering the products or service to the

marketplace

- Procurement of parts, manufacturing,

distribution, marketing and sales,

administration, post-purchase service

and support (fig. 13.4)

- Total cost base = direct/variable costs +

indirect/fixed costs

- Variable/direct costs – costs that are directly tied to the manufacturing of a

product / service

- Ex. materials, packaging, direct labor costs, distribution costs – if

manufacturing stopped, these costs would disappear

- Indirect cost base = fixed costs + committed current period costs (fig. 13.6)

- Fixed /indirect costs – costs that exists as a result of conducting and operating

the business

- Insurance, utilities, interest on debt,

administration cost – uncontrollable in

the short-term

- Committed costs – costs a business commits to

in an operating year, often spend in advance or

at beginning of manufacturing or sales cycle

- Managers to identify 2 main conclusions:

1. The percentage of costs considered to be direct/variable costs vs. the percentage

of indirect/fixed cost

2. The cost areas that make up a significant percentage of the overall cost base

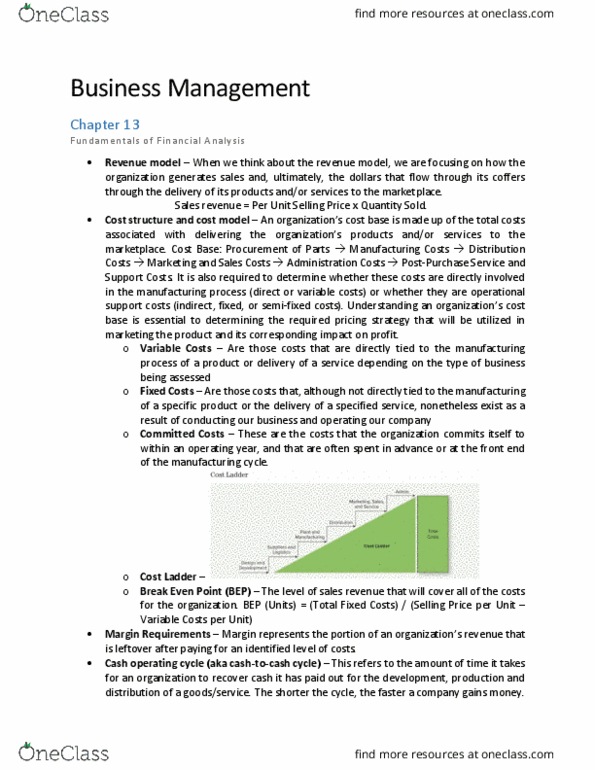

- Composition of a cost position – cost ladder (fig. 13.7)

- Total cost base composition (fig. 13.13)

- Understanding an organization’s cost base is essential to determining the required

pricing strategy that will be utilized

in marketing the product and its

corresponding impact on profit

- Breakeven Point Analysis!

- Breakeven Point (BEP) – the level of sales

revenue o volume that is required for the

organization to cover all of its costs

- BEP Formula (fig. 13.10):

Total Sales Revenue – Total Costs (VC + FC) = $0 profit

- BEP – the minimum acceptable position for the business in the short term

- Computing BEP:

1. Reasonably estimate organization’s costs – if they are fixed or variable

2. Take this costs analysis and incorporate it into the BEP formula!

- Calculating BEP:

- 𝐵𝐸𝑃!𝑢𝑛𝑖𝑡𝑠 =!!"#$%!!"#$%!!"#$#

(!"##$%&!!"#$%!!"#!!"#$ !!"#$%"&'!!"#$#!!"#!!"#$ )

- 𝐵𝐸𝑃!𝑑𝑜𝑙𝑙𝑎𝑟𝑠 =!!"#$%!!"#$%!!"#$#

(!!!"#$"%&'!!"#$!!"#$"%&'(")

! Managers need to continually reassess their breakeven position in order to understand

how changes to their cost structure or to their selling price will impact BEP

- BEP is used to identify the level that sales revenue has to reach in order to cover the

total operating costs of an organization

3. Margin Requirements

- Margin – represents the portion of an organization’s revenue that is left over after paying

for an identified level of costs

- Key indicator of the overall operating efficiency of an organization

4. Cash Operating Cycle (COC)

- Cash Operating Cycle (COC) = the amount of time it takes for an organization to

recover the cast (product is sold and money is received) it has paid out for the

development, production, and distribution of products (Fig. 13.15)

Document Summary

Sales revenue = per unit selling price x quantity sold. Managers need to analyse the underlying trends impacting the revenue model - whether these trends will assist in growing revenue, or reduction in revenue. What percentage of total sales and revenue does each product represent: cost structure and drivers. Cost base total costs associated with delivering the products or service to the marketplace. Procurement of parts, manufacturing, distribution, marketing and sales, administration, post-purchase service and support (fig. Total cost base = direct/variable costs + indirect/fixed costs. Variable/direct costs costs that are directly tied to the manufacturing of a product / service. Ex. materials, packaging, direct labor costs, distribution costs if manufacturing stopped, these costs would disappear. Indirect cost base = fixed costs + committed current period costs (fig. Fixed /indirect costs costs that exists as a result of conducting and operating the business. Insurance, utilities, interest on debt, administration cost uncontrollable in the short-term.