Economics 1021A/B Chapter Notes - Chapter 13: Price Discrimination, Marginal Revenue, Economic Rent

10 Sep 2013

School

Department

Course

Professor

94

ECON 1021A/B Full Course Notes

Verified Note

94 documents

Document Summary

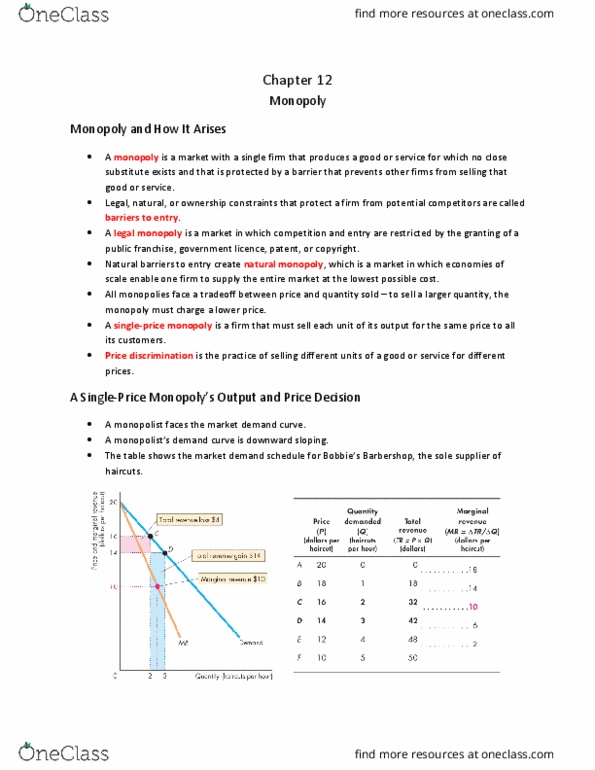

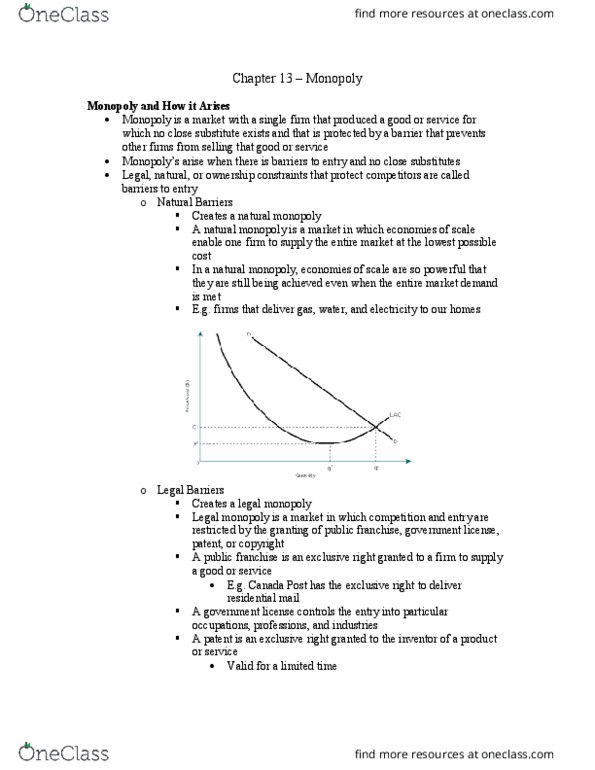

A monopoly is a market with a single firm that produces a good or service for which no close substitute exists and that is protected by a barrier that prevents other firms from selling that good or service. Legal, natural, or ownership constraints that protect a firm from potential competitors are called barriers to entry. A legal monopoly is a market in which competition and entry are restricted by the granting of a public franchise, Natural barriers to entry create natural monopoly which is a market in which economies of scale enable one firm to supply the entire market at the lowest possible cost. All monopolies face a trade off between price and quantity sold, to sell a larger quantity, the monopoly must charge a lower price. A single price monopoly is a firm that must sell each unit of its output for the same price to all its customers.