Management and Organizational Studies 3363A/B Chapter Notes - Chapter 12: List Of Fables Characters, Audit Risk, Revenue Recognition

2 May 2017

School

Department

Professor

Document Summary

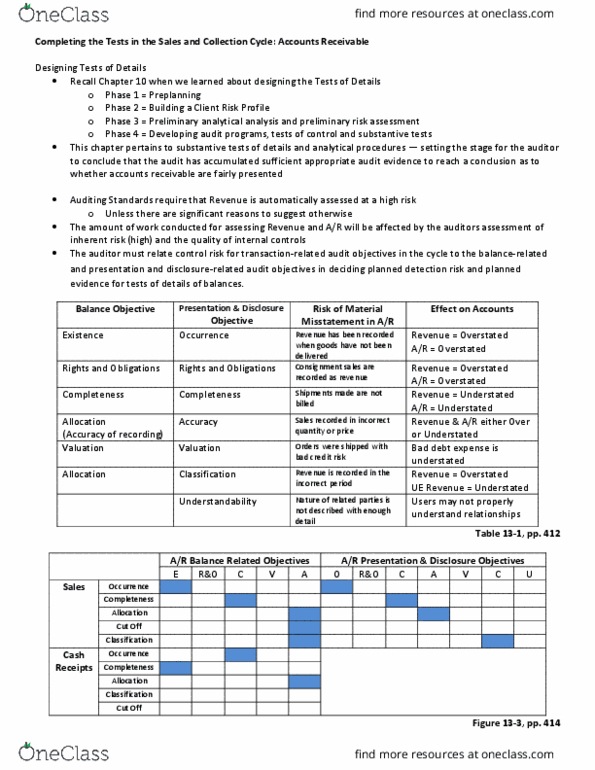

Audit of sales and collection cycle: tests of control: the overall objective of any cycle is to evaluate whether the account balances affected by the cycle are fairly presented. Identify any controls that may offset the risks. Identify the tests of details that will help you test the concern. Revenue cycle: purchase order, credit check, order gets processed. Invoice is sent (based on shipping document: processing returns and allowance, accounting for bad debts, receiving the cash owed, and record receipt of cash. Accounts in the cycle: revenue, sales returns and allowance, accounts receivable, bad debt expense, cash. Sales cycle audit planning: risk assessment comprises the first three phases of the audit: preplanning, client risk profile and planning the audit. It is only after risk assessment that the auditor can decide upon the risk response and design further procedures, such as control testing: the higher the risk level, the more testing is required by the auditor.