Management and Organizational Studies 3370A/B Chapter Notes - Chapter 9: Profit Motive, Finished Good

14 Mar 2016

School

Department

Professor

Document Summary

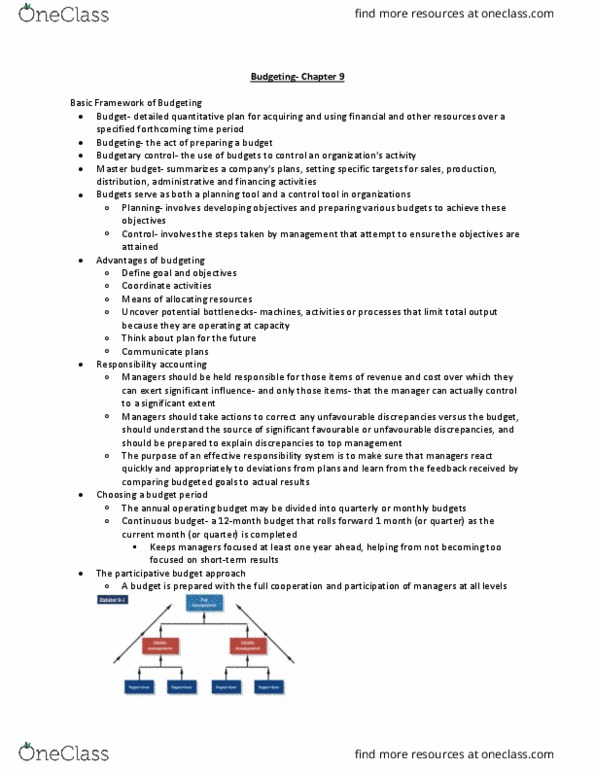

Planning involves developing objectives and preparing various budgets to achieve these objectives. Control involves the steps taken by management that attempt to ensure the objectives are attained. Think about and plan for the future. Managers should be held responsible for those items and only those items that the manager can actually control to a significant extent. The annual operating budget may be divided into quarterly or monthly budgets. A continuous budget is a 12 month budget that rolls forward one month (or quarter) as the current month (or quarter) is completed. A budget is prepared with the full cooperation and participation of managers at all levels. Participative (self-imposed) budgets should be reviewed by higher levels of management to prevent budgetary slack . Most companies do not rely exclusively upon participative budgets in the sense that top managers usually initiate the budget process by issuing broad guidelines in terms of overall profits or sales. Overall policy matters relating to the budget.