BU487 Chapter Notes - Chapter 2: Current Asset, Retained Earnings, Financial Statement

Document Summary

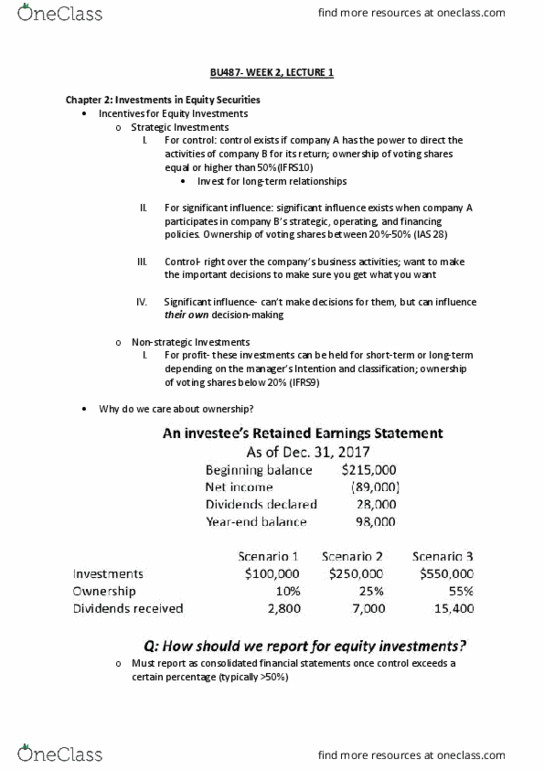

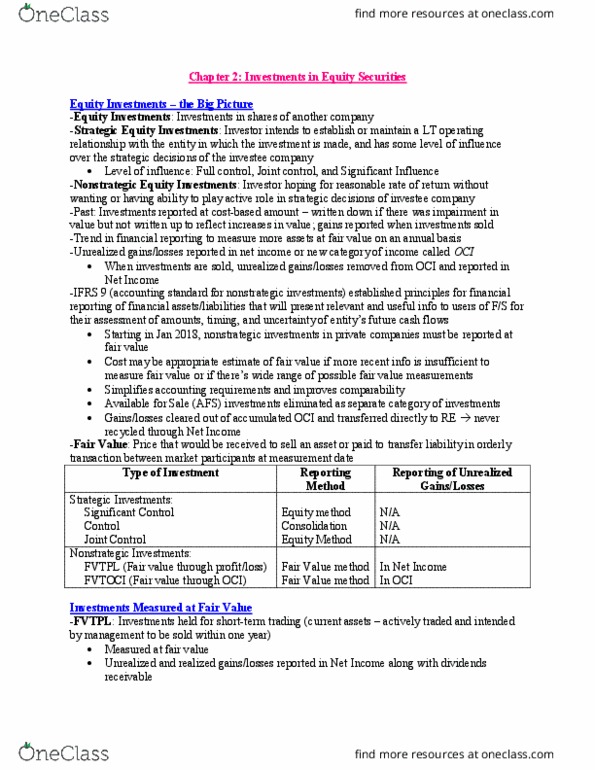

Investments are made in the shares of another company: seeks to have a long term relationship with the company and wants to have influence over strategic decisions, significant influence, control, joint control. Non-strategic: wants a good return on the investment but doesn"t care too much for having influence on company, fvtpl, fvtoci. Measured at fair value at each reporting date. The unrealized and realized gains are reported in net income. All unrealized gains are reported in oci. Cumulative unrealized gains are cleared out and placed into retained earnings this transaction usually occurs when investment is sold. Available for sale investments that do not have a market quoted value. Parent company"s books before making consolidated financial statements. Record dividends when they are received and not declared. Investment account is directly effected by net income changes. When the acquisition cost is greater than carrying amount of the investment this will be considered as goodwill.