EC238 Chapter Notes - Chapter 12: Opportunity Cost, Social Cost

Chapter 12 – Emission Taxes and Subsidies

Market-Based Incentive Policies

1.) Taxes and subsidies

2.) transferable emission permits

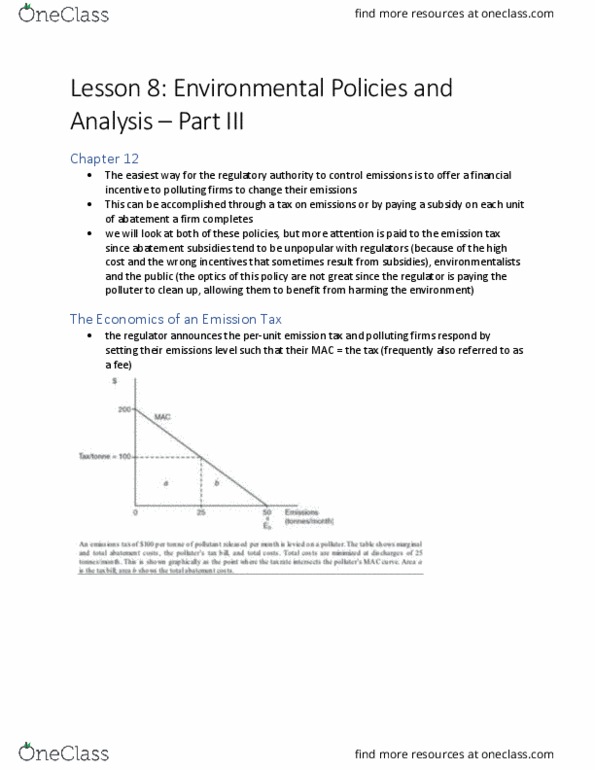

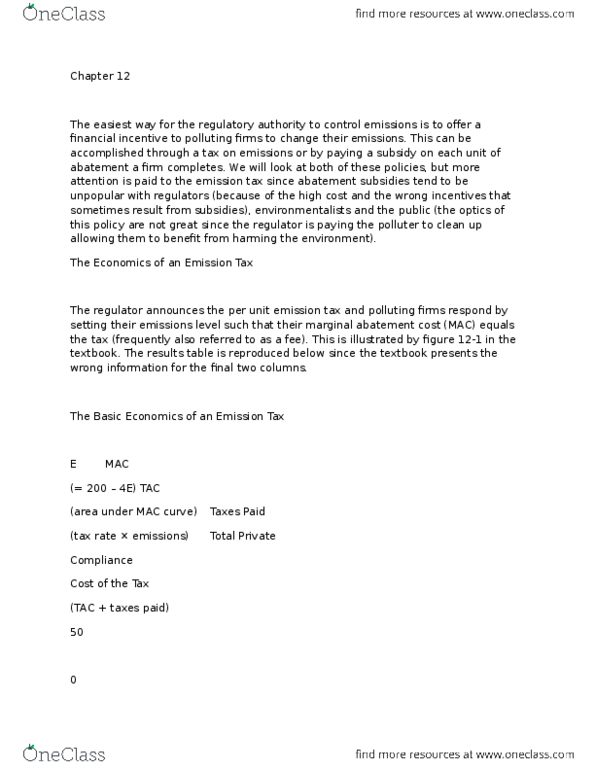

Emission Taxes or Emission Charges

Incentive based approach to controlling emissions

o1.) taxing each unit of emissions or

o2.) giving a subsidy for each unit of emissions that the source cuts back

As you pollute more, the less subsidy you will get, therefore you need to find a maximum of subsidy you

get minus abatement cost, so reducing emissions until the tax rate equals their marginal abatement cost

Total damages forgone = area (e + f)

Net social benefit = area (e + f) minus e

Emission Taxes vs. Standards

When MACs differ among polluters, social compliance costs are lower under a tax than a

uniform standard meeting the same target level of emissions because the tax is cost effective

and the uniform standard is not

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Incentive based approach to controlling emissions: 1. ) taxing each unit of emissions or, 2. ) giving a subsidy for each unit of emissions that the source cuts back. As you pollute more, the less subsidy you will get, therefore you need to find a maximum of subsidy you get minus abatement cost, so reducing emissions until the tax rate equals their marginal abatement cost. Total damages forgone = area (e + f) Net social benefit = area (e + f) minus e. When macs differ among polluters, social compliance costs are lower under a tax than a uniform standard meeting the same target level of emissions because the tax is cost effective and the uniform standard is not. Emission taxes, the double dividend, and the bc carbon tax. The taxes that government collect from emissions, it is used to reduce other taxes that provide disincentives to work, such as taxes on payroll, income, and investments.