*Article*

The U.S. economy is revving up just as Europe and other major economies lose steam, jeopardizing a rare period in which the worldâs largest economies have been accelerating in unison.

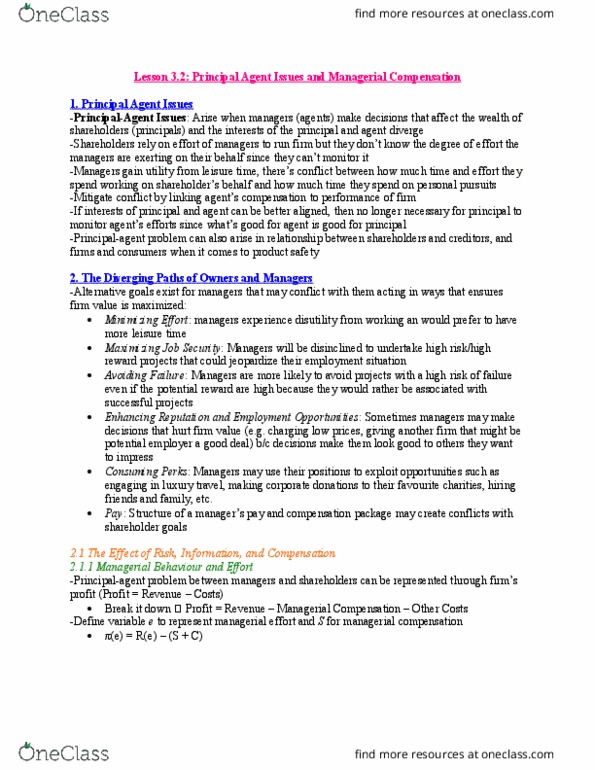

The European Central Bank on Thursday took another step toward ending the massive stimulus measures it has used in an effort to boost growth since 2015. But ECB officials also said they would hold interest rates steady through summer next year, a sign that they felt the eurozone economy remains fragile.

In an indication of growing economic vigor in the U.S., the Federal Reserve on Wednesday tapped the brakes again, raising the benchmark interest rate by a quarter of a percentage point and signaling it may quicken the pace of future rate increases because of a strengthening economy and tightening labor markets.

The economiesâ diverging paths were expressed most prominently in the euro, which on Thursday suffered its worst day against the dollar in two years. The euro lost 1.88% against the U.S. currency, its biggest drop since the day after the U.K. voted to leave the European Union.

The central bank announcements over the past two days offered the latest evidence that heady growth expectations for Europe and other major economies outside the U.S. might not be achieved, defying analysts who began the year convinced that the world economyâs first synchronized expansion in years would continue.

The International Monetary Fund said in January that the worldâs seven largest economies each grew more than 1.5% in 2017, and it predicted more solid growth this year. Global manufacturing was booming and the IHS Markit global purchasing managers index that month was its strongest in nearly seven years.

Many investors counted on a revitalized Europe to lead that growth in 2018. But recent labor strikes in France, political turmoil in Italy and softer economic data are causing investors to rethink that premise. Germany last week reported that factory orders dropped 2.5% in April, while eurozone growth was 0.4% in the first quarter, down from 0.7% in the final quarter of 2017. On Thursday, the ECB revised down its eurozone growth expectations for this year to 2.1%, from 2.4%.

âWhen we look at Europe, the very strong momentum we saw in data last year has been waning this year,â said Holly MacDonald, chief investment strategist at Bessemer Trust.

Europe isnât the only region to show signs of cooling down. The Peopleâs Bank of China this week also left a suite of key short-term interest rates unchanged. New data showed business activity, including investment and retail sales, slowed in May, suggesting the worldâs second-largest economy is facing growing headwinds.

The disappointing figures âwarranted China to take a cautious tone,â said Tommy Xie, an economist at OCBC Bank.

In the U.S., meanwhile, recent data suggest an economic expansion that just became the second-longest in the nationâs history is accelerating, rather than slowing down.

The U.S. economy grew modestly over the winterâat a 2.2% annual rate in January through Marchâbut seems to be ramping up further this spring. Growth is on track to exceed a 4% pace in the three months ending in June, which would be the fastest of any quarter in almost four years.

Spending at U.S. retailers soared 0.8% in May, the biggest jump in six months, according to U.S. government data released on Thursday. Consumers, spurred by tax cuts and the lowest unemployment in half a century, shelled out more for cars, clothing, building supplies, health products and bar tabs.

âWe may be entering a new level of consumer spending right now,â said economist Robert Frick of the Navy Federal Credit Union. He pointed out that more and more blue-collar workers are finding work as the labor expansion endures, and those workers tend to spend a greater portion of their incomes, out of necessity, than higher-income workers, who save more.

He added that low unemployment, strong consumer spending and modest inflation are likely to keep the economy on strong footing this year: âWeâre in a Goldilocks zone right now.â

In the eurozone, rates have stayed pegged at negative levelsânow at minus 0.4%âsince 2014. Despite some initial concerns, investors have become more relaxed about possible unintended effects of negative rates on the economy.

On Thursday, investors reacted to the ECBâs announcement to end bond purchases while keeping rates low longer by selling the euro and bidding up stocks. It is the latest example of interest-rate moves returning to the driverâs seat of monetary policy. In the wake of the financial crisis, central bankers rolled out a raft of unprecedented and complex measures, including bond buying and lending facilities for banks, pitching them as a way to lower long-term borrowing costs at a time when short-term rates could go no lower.

Not all investors are ready to write off Europeâs growth prospects. Roland Kaloyan, head of European equity strategy at ?Société Générale, believes that lackluster economic data in the first quarter is a âtemporary soft patch,â and that âfundamentals remain very solid for eurozone growth,â whereas he expects the U.S. economy to go into a recession around 2020.

Others believe the euro will continue to weaken further this year, but think that markets are swinging too far in favor of U.S. growth.

Next year, âwe expect the euro to rebound against the dollar even if the ECB only hikes late in the year,â said Ingvild Borgen Gjerde, an analyst at Capital Economics. âWe think the Fedâs tightening cycle will come to an end in mid-2019, far sooner than is discounted in the markets.â

*question*