ACTG 4710 Chapter Notes - Chapter 6: Compound Interest, Fide, Tax Rate

1 Nov 2016

School

Department

Course

Professor

Document Summary

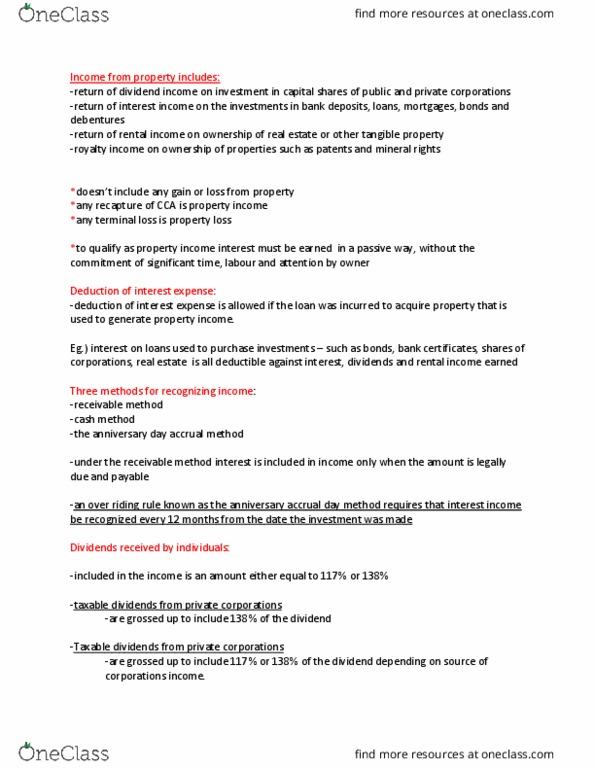

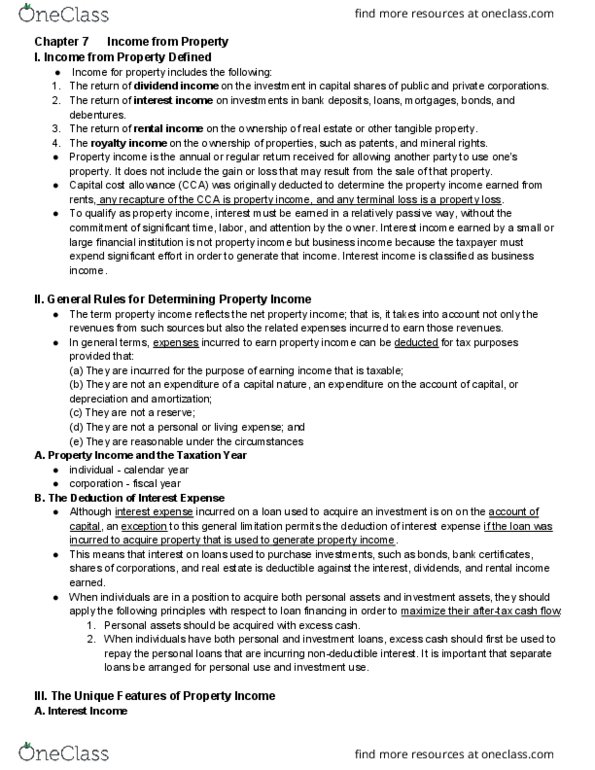

Division b income calculated by determining income from each source separately: Chapter 6: income from property: employment income, business income, property income. Property income is passive income: must be earned in passive way, without commitment of significant time, labor, and attention by owner. Interest income from bonds etc: dividend income, rental income, royalty income. Ita 16(1)(c) does(cid:374)"t i(cid:374)clude capital gain or loss. Includes recapture and terminal loss on sale of property. Individual who invests in bond and earns interest income passive income. Individual actively trades bonds in capital market continuously business income. Business income requires more activities in process that combines time, effort, and capital investment. Similarly to business income, ita sections 9-21 deal with property income. Deductible expe(cid:374)ses = (cid:396)easo(cid:374)a(cid:271)le e(cid:454)pe(cid:374)ses that a(cid:396)e i(cid:374)(cid:272)u(cid:396)(cid:396)ed fo(cid:396) pu(cid:396)pose of ea(cid:396)(cid:374)i(cid:374)g i(cid:374)(cid:272)o(cid:373)e that(cid:859)s ta(cid:454)a(cid:271)le. Incurred to earn taxable property income: for other than capital expenditures, other than reserves, for other than personal or living expenses, reasonable.