FINE 4050 Chapter Notes - Chapter 6: Life Annuity, Double Taxation, Canada Revenue Agency

12 Dec 2015

School

Department

Course

Professor

Document Summary

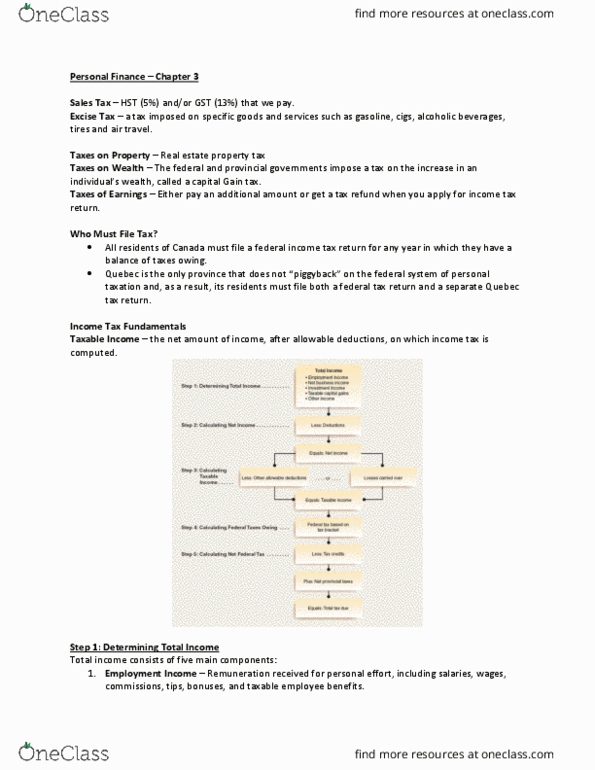

Tax returns: required to file a tax return annually if you are a canadian resident with income above a certain benchmark; combined form in which both levels of taxes are calculated. Residence status: determined by amount of time spent in canada that year, ownership of residence in canada, social & economic ties to canada. Quebec: does not follow combined form; uses its own personal income tax collection. Taxable income: figure out total income from all sources; domestic and foreign sources included; subtract deductions that are allowable through tax laws. Taxable income = total income tax deductions. Chapter 6 personal income taxes (canadian content) Income taxes in canada: assessed both provincially and federally. Tax payable: remove tax credits from total tax. Tax payable = total tax amount tax credits. Employment income: wages, salary, commissions, bonuses, other employment benefits; those self-employed consider employment income to be business income less reasonable expenses. Pension income: from either company"s pension plan or canada pension plan;