ACCT20200 Chapter Notes - Chapter 9: Amortization Schedule, Internal Financing, Interest Expense

Ch. 9 Long-Term Liabilities

● Internal financing: sourced from generated profits

● External financing: funds coming from outside of the company

● Liabilities and stockholder’s equity reveal debt financing and equity financing

○ Debt financing: borrowing money from creditors (L)

○ Equity financing: obtaining investment from stockholders (E)

● Capital structure: the mixture of liabilities and equity a business uses

● Interest expense incurred when borrowing money is tax-deductible, whereas dividends

paid to stockholders are not tax-deductible

○ Debt can be a less costly source of external financing

○ Interest expense incurred on debt reduces taxable income

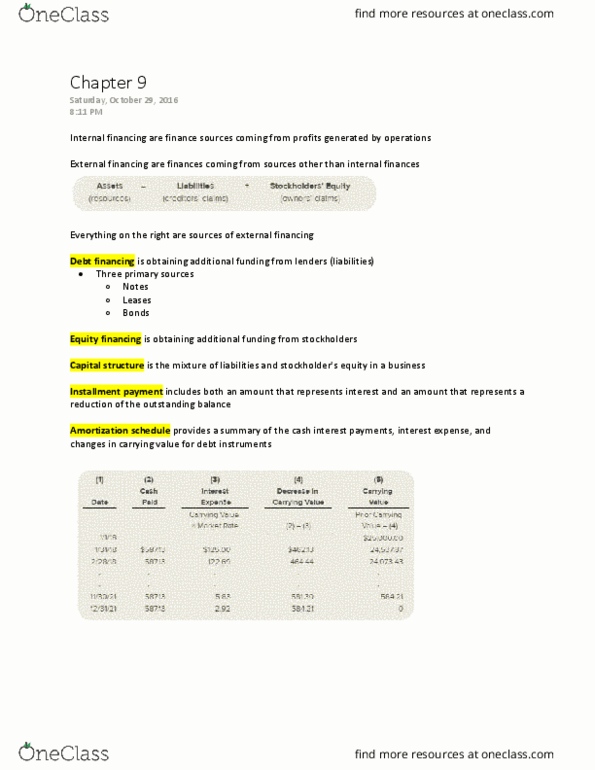

● Installment payments: include both an amount that represents interest and an amount that

represents a reduction of the outstanding balance

○ Amortization schedule: a table format detailing the cash payments each period,

interest portion, carrying value charge and the balance of the carrying value.

○ Installment note payable = interest is recorded as interest expense

○ * = omitted periods

○ Elements of an amortization schedule:

■ Date (end-of-the-month payments)

■ Cash paid (same every month)

■ Interest expense (prior month’s carrying value times interest)

■ Decrease in carrying value (cash paid in excess of interest expenses reduced

the remaining loan balance)

■ Carrying value: remaining balance of the loan after each monthly payment

○ Monthly amortization payment record:

■ Debit interest expense for the interest and debit notes payable for the

difference in the monthly payment

■ Credit cash for the full monthly payment amount.

● Credit the account that the note was used to purchase (either cash or

a non cash asset)

● Lease: contractual agreement by which the owner provides the user the right to use an asset

for a specified period of time.

○ Benefits of leasing instead of buying:

■ Reduces upfront cash needed to use an asset

■ Payments are lower than installment payments

■ Offers flexibility and lower costs when disposing of an asset

■ May offer protection against the risk of declining asset values

○ Recording a lease:

■ User: acquire an asset(lease) and get a lease payable

● Initial record: debit lease asset and credit lease payable at the present

value of the lease payments.

■ Lease payment annuity calculation: need to know future value, lease

payment, number of payments, interest rate.

● Bond: formal debt instrument issued by a company to borrow money

○ The issuer received cash by selling the bond to an investor.

○ Issuer promises to pay back:

■ Stated amount (principal/face amount) at a specific maturity date

■ Periodic interest payments over the life of the bond.

○ Underwriting services: bonds are sold by specific investment houses

■ Creates a service fee for issuing company

○ Private placement: sale of debt securities directly to a single investor

○ Bonds have a lower interest rate than a bank loan

○ Secured bonds: are backed by collateral

○ Unsecured bonds: are not backed by a specific asset

○ Term bonds: full principal amount payment mat a single maturity date

■ Sinking fund: an investment fund used to set aside money to be used to pay

debts as they come due

○ Serial bonds: require payments in installments over a series of years

○ Callable bonds: issuing company can pay off bonds early at a specific price

○ Convertible bonds: investor can convert bonds to common stock

○ Most bonds pay interest semiannually