ACCT 1201 Chapter Notes - Chapter 8: Interest Rate, Accounts Receivable, Accounts Payable

5 May 2015

School

Department

Course

Professor

Document Summary

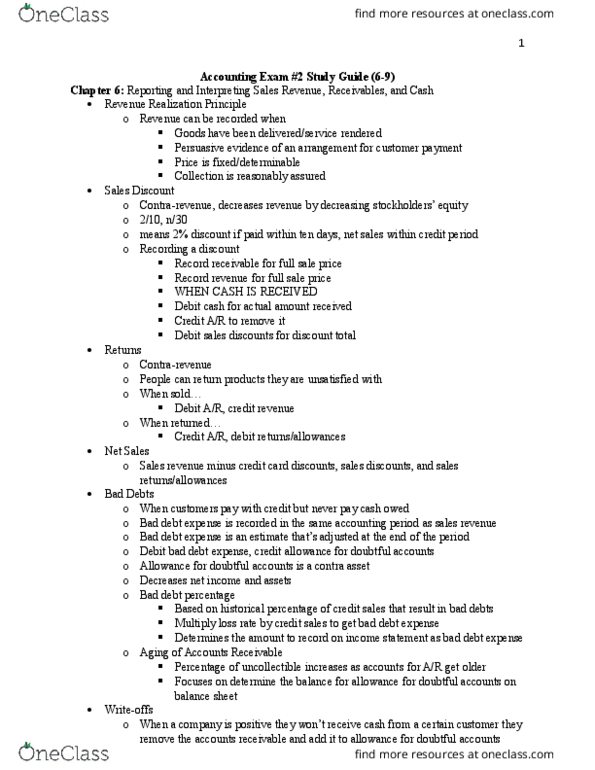

Types of receivables: 1) accounts receivable: amounts customers owe as a result of the sale of company"s product, and expected to be collected within 30 to 60 days. 2) notes receivable: (trade receivables) are a written promise for amounts which are expected to extend 60 - 90 days or longer, they are collected with interest. 3) other receivables: include nontrade receivables which do not result from the operations of the business. Accounts receivables: recognizing, valuing and disposing accounts receivable: recognizing: when a company provides its product (service or good) on account. Selling on account increases (debits) accounts receivable and increases (credits) sales revenue. Sales returns decreases (credits) accounts receivable , and increases (debits) sales returns. To encourage early payments , the seller offers discount , so when it"s paid both of. Cash and discount increase (debit), and accounts receivables decreases (credit).