MGT 5 Chapter Notes - Chapter 6: Contribution Margin, Net Income, Operating Leverage

28 Jul 2017

School

Department

Course

Professor

Document Summary

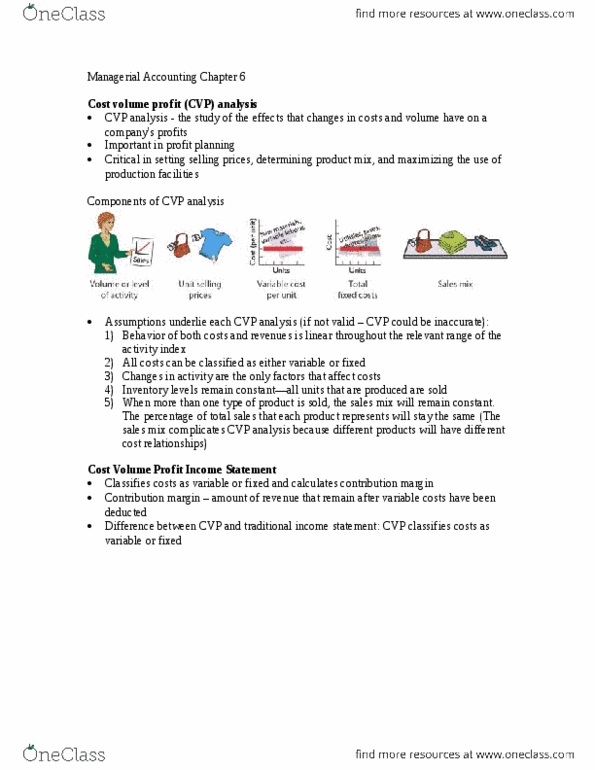

Contribution margin: amount of revenue remaining after deducting variable costs. Cost includes manufacturing costs plus selling and administrative expenses. Lo 2: explain the term sales mix and its effects on break-even sales. Sale mix: relative percentage in which a company sells its multiple products. The weighted-average unit contribution margin of all the products. Net income will be greater if higher contribution margin units are sold rather than lower contribution margin units. Lo 3: determine sales mix when a company has limited resources. Contribution margin per unit of limited resource: divide the unit contribution margin of each product by the number of units of the limited resource required for each product. Lo 4: indicate how operating leverage affects profitability. Cost structure: the relative proportion of fixed versus variable costs that a company incurs. Operating leverage: refers to the extent to (cid:449)hi(cid:272)h a (cid:272)o(cid:373)pa(cid:374)y"s (cid:374)et i(cid:374)(cid:272)o(cid:373)e rea(cid:272)ts to a given change in sales.