ACCT207 Chapter 3: Unit 3 Textbook Notes

4 Aug 2018

School

Department

Course

Professor

Document Summary

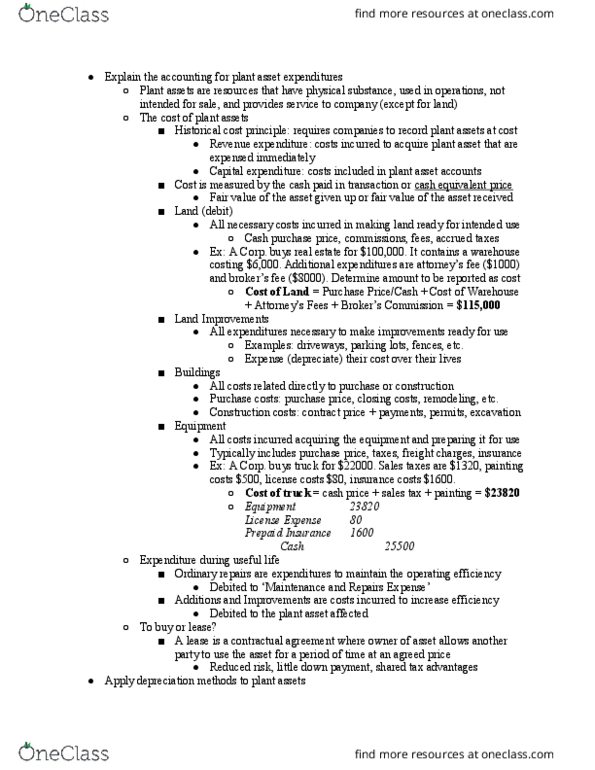

Chapter 9 reporting and analyzing long lived assets. Its important for a company to: keep assets in good operating condition, place worn out or outdates assets, expand its productive assets as needed. The historical cost principle requires that companies record plant assets at cost. Cost consists of all expenditures necessary to acquire an asset and make it ready for its intended use: such costs are referred to as revenue expenditures. Some companies, in order to boost current income, have improperly capitalized expenditures that they should have expenses. Cost is measures by cash paid in a cash transaction or by the cash equivalent price paid when companies use noncash assets in payment. The cash equivalent price is equal to the fair value of the asset given up or the fair value of the asset received, whichever is more clearly determinable. Once cost is established, it becomes the basis of accounting for the plant assets over its useful life.