ACG 2071 Chapter Notes - Chapter 3: Financial Statement, Internal Control, Larceny

26 Feb 2019

School

Department

Course

Professor

Document Summary

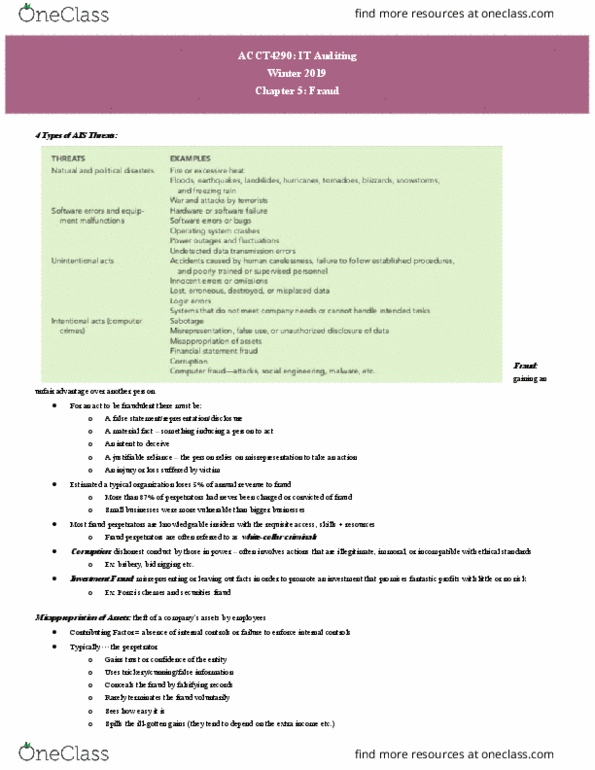

Fraud denotes a false representation of a material fact made by one party to another party with the intent to deceive and induce the other party to justifiably rely on the fact to his or her detriment. In the business environment, fraud is an intentional deception, misappropriation of a company"s assets, or manipulation of a company"s financial data to the advantage of the perpetrator. Auditors encounter fraud at two levels: employee fraud fraud by non-management employees, generally designed to directly convert cash or other assets to the employee"s personal benefit. Notwithstanding the importance of personal ethics and situational pressures in inducing one to commit fraud, opportunity is the factor that facilitates the act. No one can perpetrate a fraud if no opportunity to do so exists. Three broad categories of fraud schemes are defined as: fraudulent statements, corruption, and asset misappropriation.