ACIS 4414 Chapter Notes - Chapter 12-14: Audit Risk

2 Nov 2016

School

Department

Course

Professor

Document Summary

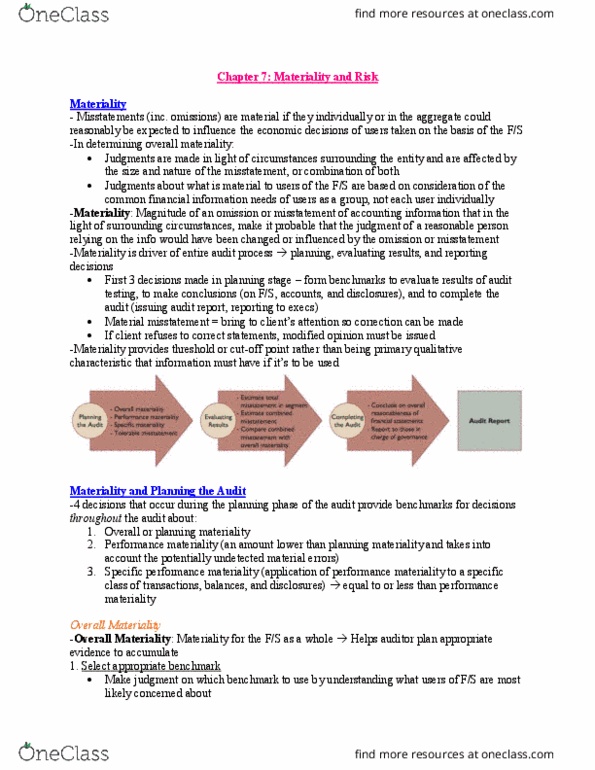

Conduct audits to obtain reasonable assurance that f/s are free of material. Magnitude of an omission or misstatement that makes it probable that a reasonable user of f/s"s judgement would be affected: take all groups and take the lowest who could care. Factor in: client size, distribution of ownership, nature & amount of liabilities. Inversely related to amount of evidence: materiality for segments of the audit, allocate materiality to bs accounts, example: m=1 million pm = 750,000 (75%) Benchmarks to determine if a misstatement is material. If an amount changes income to a loss: loan covenant, ratios, state of business, risk of being sued. Tolerable misstatement: pcaob says it"s a misstatement lower than materiality threshold, aicpa says its applying performance materiality to a sampling procedure. Misstatements: mgt has to be told of misstatements that are not trivial, known misstatement"s. Have proof so mgt has to correct: likely misstatement. Because of differences between mgt & auditor judgement about account balance estimates.