Accounting ACCT 2610 Chapter Notes - Chapter 3: Earnings Before Interest And Taxes, Matching Principle, Weighted Arithmetic Mean

19 Sep 2016

School

Department

Course

Professor

Document Summary

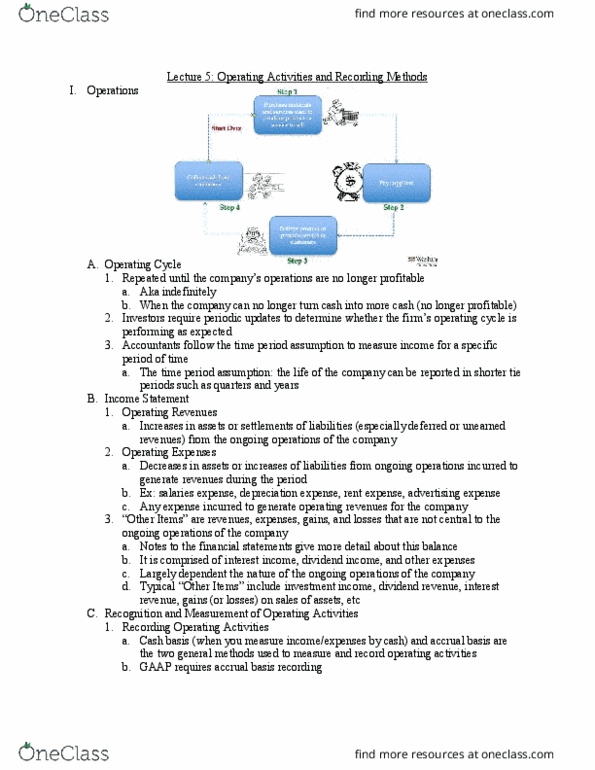

The long term objective for any is to turn cash into more cash. Companies acquire inventory and the services of employees. The operating (cash-to-cash) cycle is the time it takes for a company to pay cash to suppliers, sell goods and services to customers, and collect cash from customers. The time period assumption indicates that the long life of a company can be reported in shorter time period. Revenues are increases in assets or settlements of liabilities from ongoing operations. Operating revenues result from the sale of goods or services. When the company provides the good or service, then the revenue is recognized. Expenses are outflows or the using up of assets or increases in liabilities from ongoing operations incurred to generate revenues during the period. An expenditure is any outflow of cash for any purpose. Not all expenditures are expenses, but expenses are necessary to generate revenue. Operating revenues - operating expenses = operating income.