ECON111 Lecture Notes - Lecture 10: Economic Equilibrium, Fixed Cost, Marginal Utility

Week 10 Perfect Competition

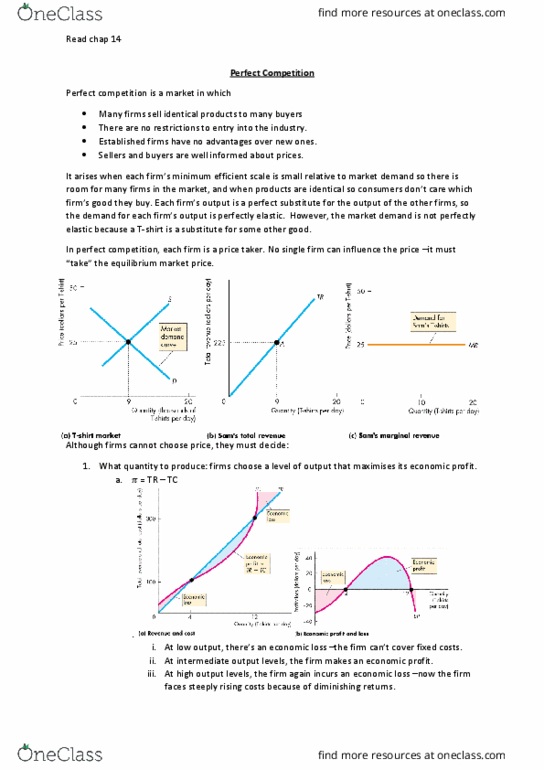

Perfect Competition

- Many firms

- No barriers to entry

- Identical products

- Perfect information (buyers are aware of where to buy and what the price is)

- E.g. foreign exchange market (selling AUD $$)

- Each seller is a price taker (the market decides the price for them)

- Market decides the price, seller decides the quantity (MR vs MC)

Price Taker

- A firm that can’t influence the price of the good or service that it produces

- The firm in perfect competition is a price taker.

Marginal Revenue (MR)

- A firm’s total revenue equals the market price multiplied by the quantity sold

- Extra revenue from selling one extra unit

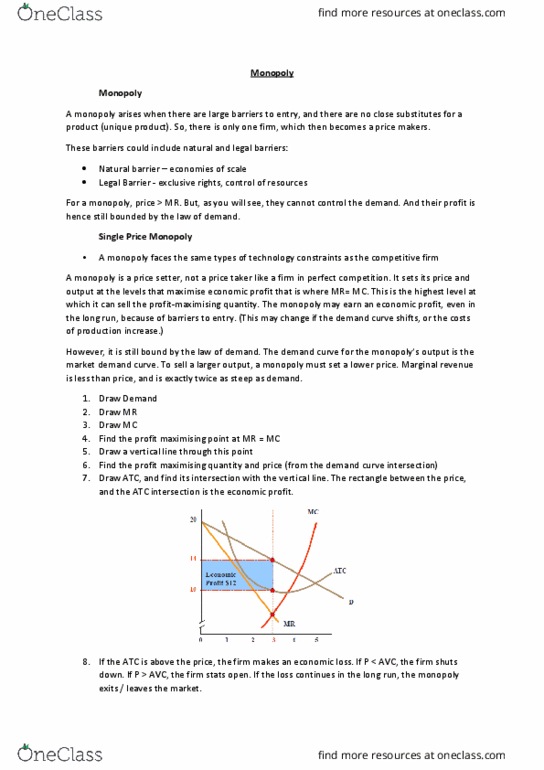

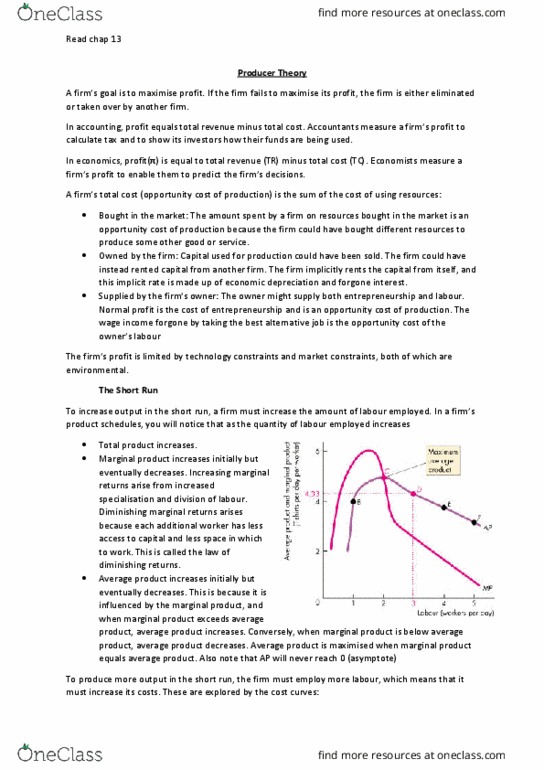

Profit Maximising Output

- As output increases, total revenue increases.

- But total cost also increases.

- Because of decreasing marginal returns, total cost eventually increases faster

than total revenue.

- If marginal revenue exceeds marginal cost (if MR > MC), the extra revenue

from selling one more unit exceeds the extra cost incurred to produce it.

- Economic profit increases if output increases.

-

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Perfect information (buyers are aware of where to buy and what the price is) E. g. foreign exchange market (selling aud 10561) Each seller is a price taker (the market decides the price for them) Market decides the price, seller decides the quantity (mr vs mc) A firm that can"t influence the price of the good or service that it produces. The firm in perfect competition is a price taker. A firm"s total revenue equals the market price multiplied by the quantity sold. Extra revenue from selling one extra unit. Because of decreasing marginal returns, total cost eventually increases faster than total revenue. If marginal revenue exceeds marginal cost (if mr > mc), the extra revenue from selling one more unit exceeds the extra cost incurred to produce it. If the firm shuts down temporarily, it incurs an economic loss equal to total fixed cost.