ACCO 340 Lecture Notes - Lecture 10: Negative Number, Net Income

25 Jan 2017

School

Department

Course

Professor

Document Summary

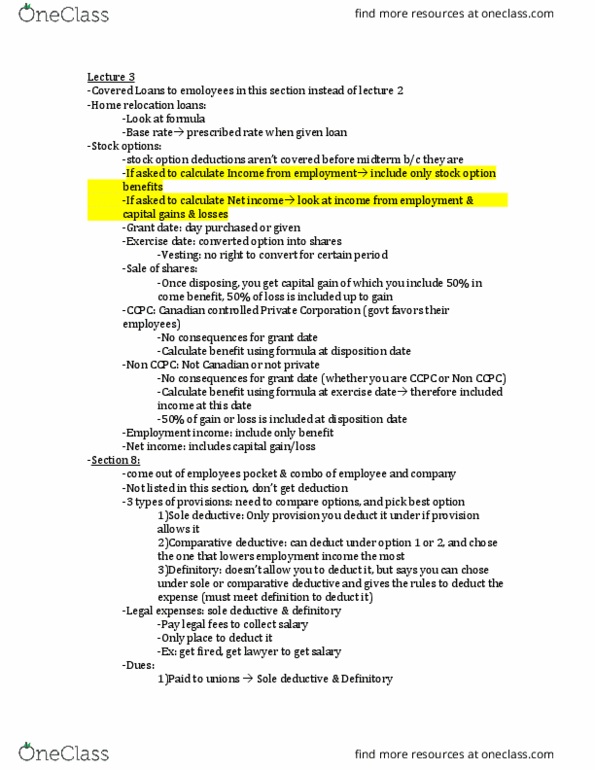

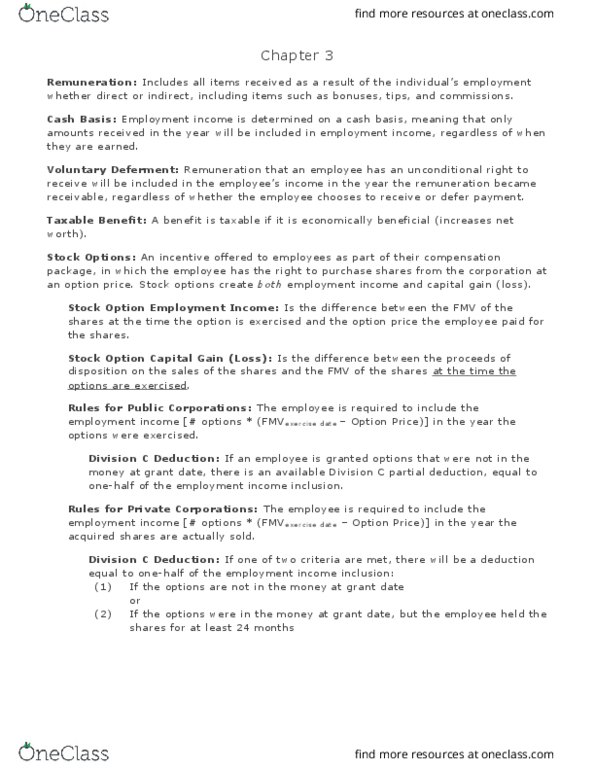

3b taxable capital gain for the year and cannot be negative. Stock option benefit sob is #shares ( exercise price grant price) Capital gain is #shares (pod acb) = sale price fmv date of purchase. Deduction granted as long as the grant price was equal or more than fmv at grant date unless is it a private company. Private company must keep shares for minimum of 2 years. Deductible only if relocation necessary on the first 25,000$, loan given by employer at lower rate. Loan * (prescribe rate upon inception date rate paid) Loan * [(prescribe rate q1 rate paid) *3/12)+ [(prescribe rate q2 rate paid) * 3/12)] + [(prescribe rate q3 rate paid) * 3/12)] + [(prescribe rate q4 rate. Carry back up to 3 years or carry forward. Lpp: only deducted against gains, carry forward 7 years, lpp loses from prior years are deducted in 3b against lpp gain of this year at.