ACCO 340 Lecture Notes - Lecture 3: Qst, Tax, Net Income

24 Mar 2018

School

Department

Course

Professor

Document Summary

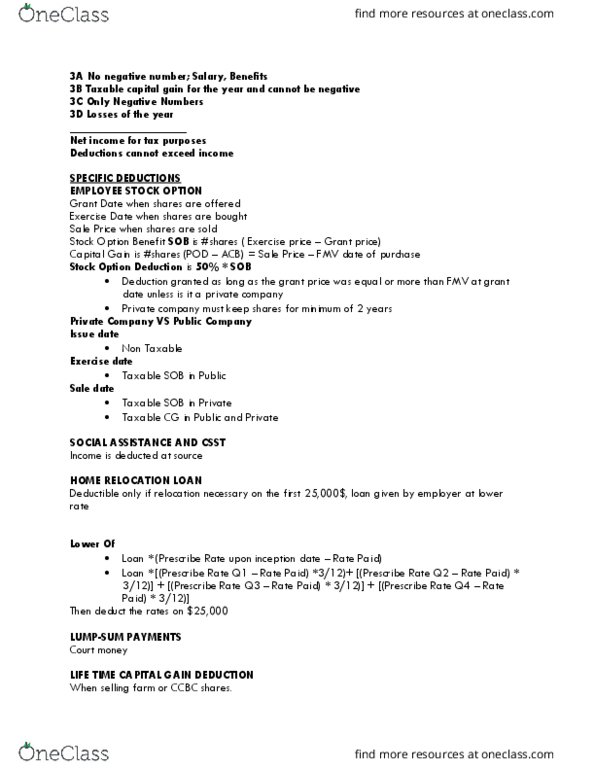

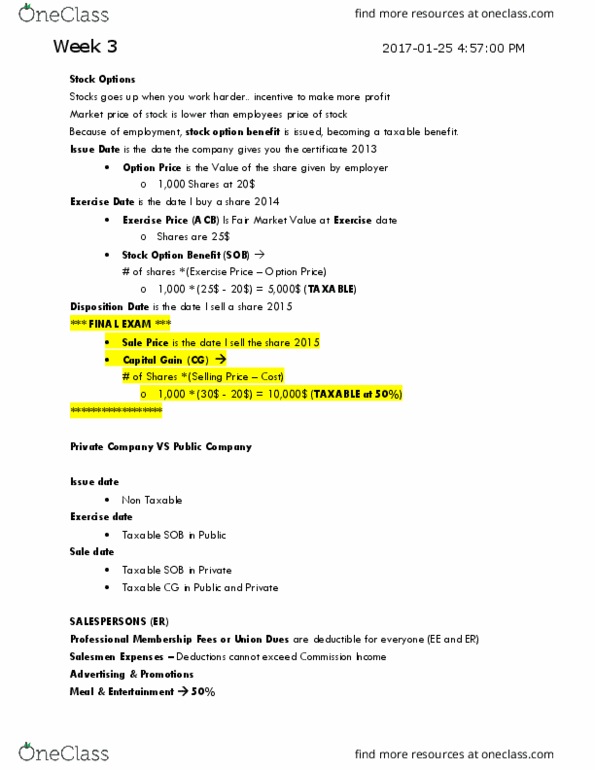

Stock option deductions aren"t covered before midterm b/c they are. Covered loans to emoloyees in this section instead of lecture 2. If asked to calculate income from employment include only stock option benefits. If asked to calculate net income look at income from employment & capital gains & losses. Ccpc: canadian controlled private corporation (govt favors their employees) No consequences for grant date (whether you are ccpc or non ccpc) Calculate benefit using formula at exercise date therefore included income at this date. 50% of gain or loss is included at disposition date. Once disposing, you get capital gain of which you include 50% in come benefit, 50% of loss is included up to gain. Vesting: no right to convert for certain period. Come out of employees pocket & combo of employee and company. Not listed in this section, don"t get deduction. 1)sole deductive: only provision you deduct it under if provision allows it.