2-504-09 Lecture Notes - Lecture 4: Arm Cortex-M, Nuclear Energy Institute, Octane Rating

2-604-15 Lecture notes

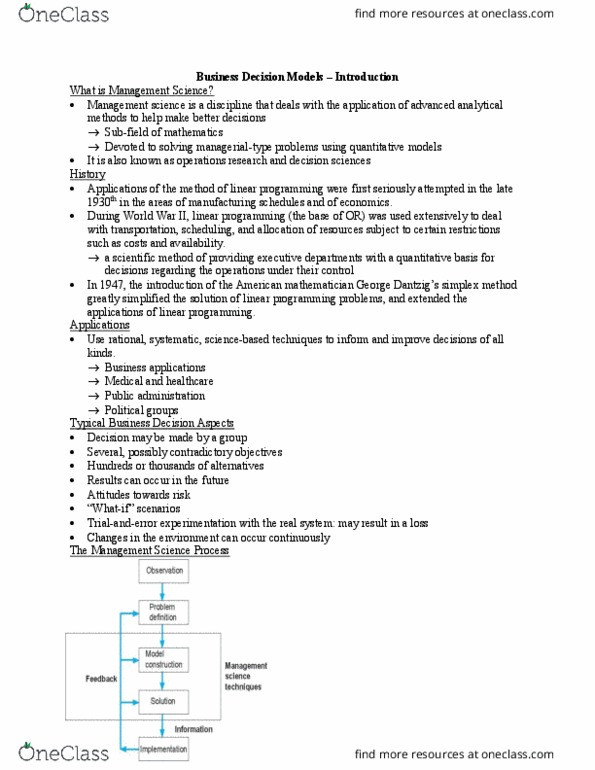

1

3. Applications in finance, marketing, and production management

The aim of this chapter is to begin illustrating the diversity of possible

applications of mathematical programming, especially of linear programming.

Section 3.1 has an application in finance, Section 3.2 has an application in

marketing, and Section 3.3 has an application in production management. Other

applications in production management, in logistics and human resources will be

presented in the following sessions.

3.1 Applications in finance

Numerous decision support models are used in the field of finance, of course, in

financial firms (banks and insurance in particular), but also in large companies.

Some of these models may take the form of linear programs. In companies,

linear programming can, for example, be used to make investment choices (in

situations where you have to decide which projects to choose within a limited

budget) or to decide whether it is more profitable to manufacture a product than

buying it from a supplier. In financial companies, mathematical programming is

mainly used to guide the composition of investment portfolios.

In such a problem, a manager typically must choose between specific

investments (e.g., stocks and bonds) from a large number of possibilities. To do

so, he or she may seek to minimize the risk of the portfolio while maintaining a

minimum return on investment. Note that this problem can be solved through a

nonlinear decision support model. Our manager may also seek to maximize its

return on investment, taking into account risk using constraints that would

guarantee a certain diversification in the portfolio composition. This type of

problem is solved using linear programming.

The example we will now consider corresponds to a variant of the classical

portfolio selection problem, which we will model as a linear program.

The Alternative Bank of Canada case

The Alternative Bank of Canada (ABC) wishes to determine its new credit

policy with a limited budget of $13 million. It intends to distinguish the

following categories of credit: car loans, commercial loans, mortgages and

personal credits which yield the following interest rates:

find more resources at oneclass.com

find more resources at oneclass.com

2-604-15 Lecture notes

2

Categories

Car

Commercial

Mortgage

Personal

Rate

8 %

4 %

5 %

10 %

Table 3.1: Data for the case Alternative Bank of Canada

ABC wishes to allocate at least 40% of loans in commercial loans. To encourage

homeownership clients, ABC wishes to allocate at least 50% of its non-

commercial loans in mortgages. Finally, for diversification purposes, ABC does

not want personal credit to account for more than 60% of commercial loans and

mortgages.

What would be the best credit policy for ABC? Propose a mathematical model to

guide ABC in its decision making.

Step 1: Analysis

To build such a mathematical model, it is necessary to analyze ABC’s problem.

Which data should be considered?

• The maximum budget;

• the interest rates associated with each type of loan;

• the minimum percentage of commercial loans;

• the minimum percentage of mortgages;

• the maximum percentage of personal credits.

Which decisions should be taken?

ABC must determine how to allocate its funds in each category. Because the

bank has a limited budget in millions of dollars, we can more precisely state that

ABC must decide the allocated loan in millions of dollars for each category.

How can we assess the quality of the decision making?

Because ABC has specified interest rates associated with each type of loan (and

allocation constraints in order to diversify its portfolio), it is natural for the bank

to maximize its return on investment.

In which context should we make the decisions?

ABC must first meet its budget ($13 million). Then ABC imposes two types of

constraints. First, ABC wishes to have a minimum percentage of commercial

loans (40%) and mortgages (50% of non-commercial loans). Second, to diversify

its portfolio, it sets a maximum percentage on personal loans (60% of

commercial loans and mortgages).

find more resources at oneclass.com

find more resources at oneclass.com

2-604-15 Lecture notes

3

Step 2: Build a verbal model

To summarize our analysis, we can state the following problem:

1. We seek to determine the allocated loan in millions of dollars for each type

of credit;

2. in order to maximize return on investment;

3. while respecting: i) the budget, ii) the minimum allocation of commercial

loans, iii) the minimum allocation of mortgages, and iv) the maximum

allocation of personal credits.

Step 3: Build a mathematical model

The third and final step to design our model is to translate the verbal model in a

mathematical model.

To do this, we first select mathematical symbols, or variables, which reflect the

decisions. Since there are four types of loans, we select four variables (one for

each type), either:

• Ca, allocated car loans, in millions;

• Co, allocated commercial loans, in millions;

• M, allocated mortgages, in millions;

• P, allocated personal credits, in millions.

Decisions must be taken to maximize return on investment. The latter is

calculated from the specified interest rate for each loan. Thus, if ABC allocates

Ca million in car loans at 8%, the return on investment will be 0.08 × Ca million

for this type of loan. We argue the same for the other types of loans. The total

return on investment (in millions) is therefore calculated as: 0.08 Ca + 0.04 Co +

0.05 M + 0.1 P. We seek to maximize this amount. The objective function of the

model is therefore written mathematically as:

Max 0.08 Ca + 0.04 Co + 0.05 M + 0.1 P.

Then we have to consider the context in which decisions are taken. This

corresponds to the constraints that the decisions must respect. It must first meet

the budget by not allocating more credit than the 13 million available. This can

be expressed as follows:

Total allocated loans (in millions) ≤ 13.

The total allocated loans is calculated as the sum of allocated loans: Ca + Co +

M + P. The equation describing the budget constraint is then written as:

Ca + Co + M + P ≤ 13.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Lecture notes: applications in finance, marketing, and production management. The aim of this chapter is to begin illustrating the diversity of possible applications of mathematical programming, especially of linear programming. Section 3. 1 has an application in finance, section 3. 2 has an application in marketing, and section 3. 3 has an application in production management. Other applications in production management, in logistics and human resources will be presented in the following sessions. Numerous decision support models are used in the field of finance, of course, in financial firms (banks and insurance in particular), but also in large companies. Some of these models may take the form of linear programs. In financial companies, mathematical programming is mainly used to guide the composition of investment portfolios. In such a problem, a manager typically must choose between specific investments (e. g. , stocks and bonds) from a large number of possibilities.