CCFC 513 Lecture Notes - Lecture 7: Income Statement, Retained Earnings

25 Jun 2018

School

Department

Course

Professor

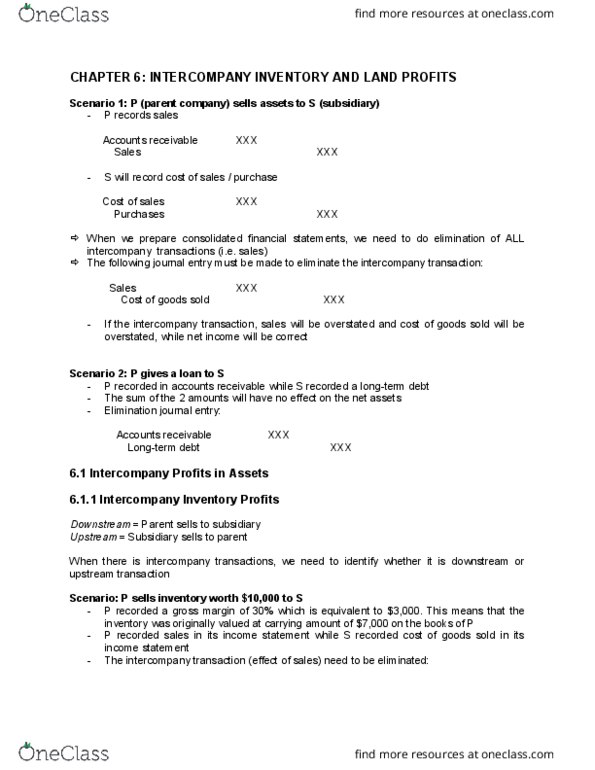

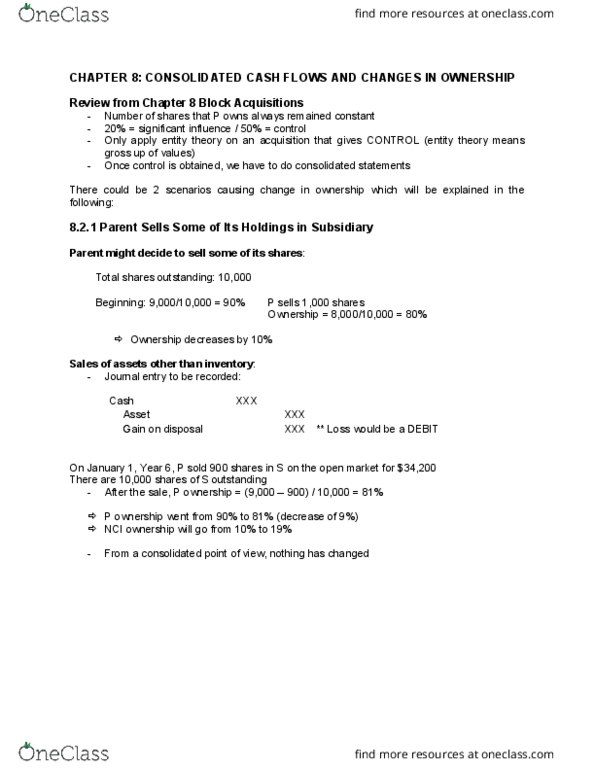

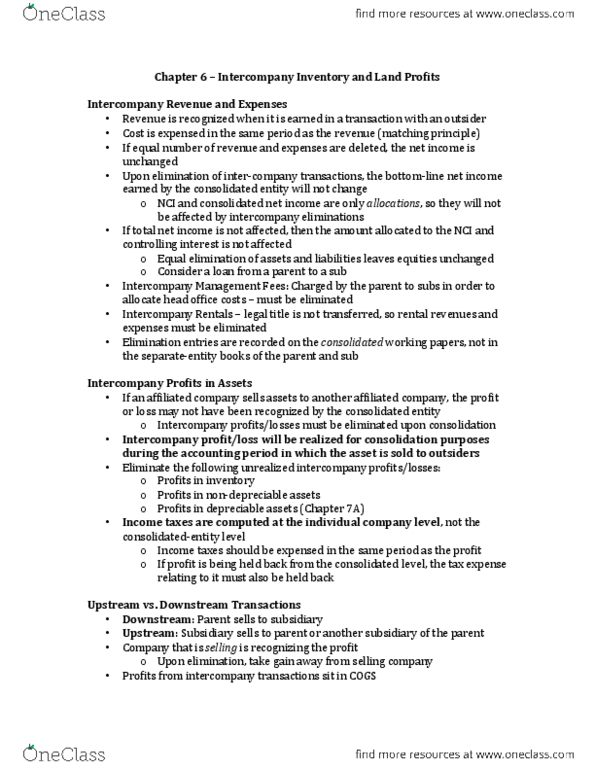

Review Chapter 6

Eliminate all intercompany transactions as if they never happened

There are intercompany transactions in:

- Inventory

- Land

- PPE

Intercompany transactions in inventory

- Step 1: Look at sales and COGS

- Step 2: Identify if there are any unrealized profit

• Problem: When inventory goes from S (subsidiary) to P (parent) and remain on

hand in the consolidated entity at year end, it is not reasonable for S to record a

profit because the asset never left the entity

• Consequence: There will be overstatement of COGS for buyer and

overstatement of profit for seller

- Step 3: When inventory is sold to outsider, the profit is realized. We will then recognize

the unrealized profit

In the current year intercompany, verify if there are any unrealized profit in the PREVIOUS

YEAR

Intercompany transactions in land

S sells land to P

- Land is overstated on balance sheet and S recorded a gain on the sale (there is no gain

there)

- By the end of the year, land is still there we must eliminate the gain on the year the

sale took place

- In Year 1, there is unrealized profit, which is waiting to be realized until land is sold to

outsiders

- At end of Year 2, if we still have a land, it remains unrealized

- At end of Year 3, if land is sold, it becomes realized profit

The unrealized/realized profits depends on timing of the moving of the assets

Intercompany transactions in property, plant and equipment (PPE)

S sold a depreciable asset to P

- S sells equipment to P, probably because P wants to use it, not because P will sell it to

outsider

- With depreciable asset, it stays in the entity until it gets used up by P. When the asset is

used up, it will never leave the company, it will be at NBV = 0

- It is not a reasonable expectation for PPE that the asset will leave the company

Document Summary

Eliminate all intercompany transactions as if they never happened. Step 1: look at sales and cogs. Step 3: when inventory is sold to outsider, the profit is realized. In the current year intercompany, verify if there are any unrealized profit in the previous. Land is overstated on balance sheet and s recorded a gain on the sale (there is no gain there) By the end of the year, land is still there we must eliminate the gain on the year the sale took place. In year 1, there is unrealized profit, which is waiting to be realized until land is sold to outsiders. At end of year 2, if we still have a land, it remains unrealized. At end of year 3, if land is sold, it becomes realized profit. The unrealized/realized profits depends on timing of the moving of the assets. Intercompany transactions in property, plant and equipment (ppe)