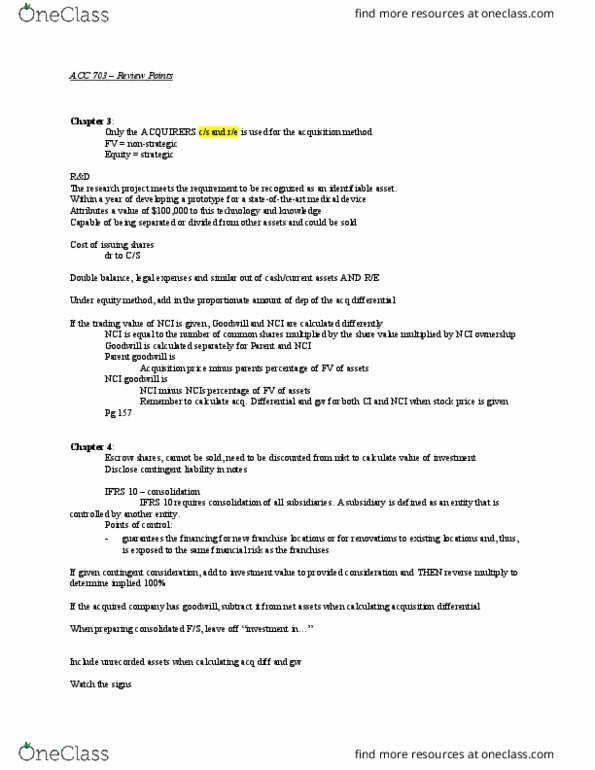

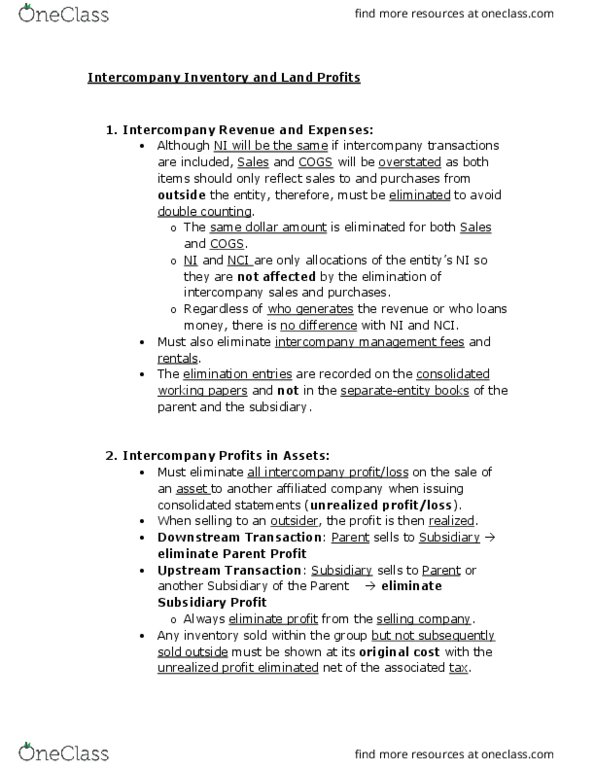

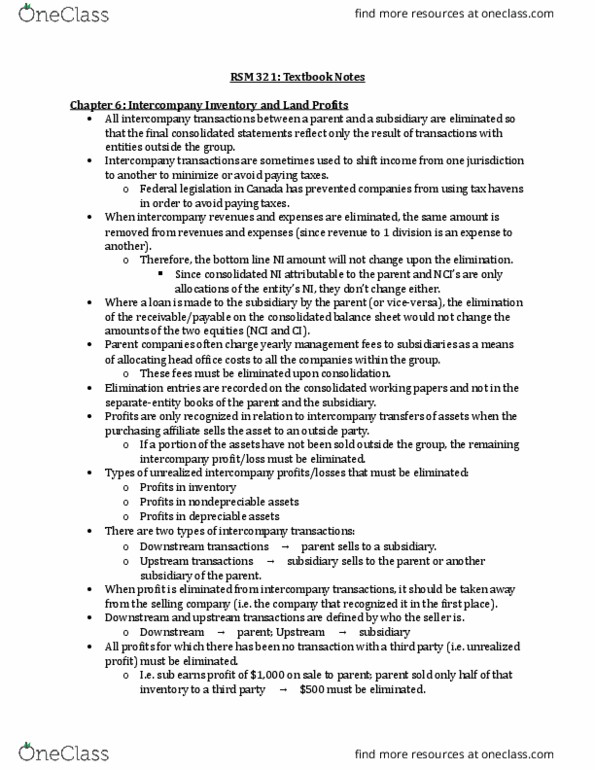

ACC 703 Chapter Notes - Chapter 6: Deferred Income, Income Statement, Financial Statement

Document Summary

Get access

Related Documents

Related Questions

Based on the informationcalculated, if S and O Consulting completed 50 longer time frameprojects and no shorter time frame projects, what would theirprojected net income be for next year?

S and O Consultants

Stephen Michaels and Luanne Taylor met at Country HillsElementary School when they were young and talked about startingtheir own business when they grew up. In 2005, after they bothgraduated from college and worked a couple years they decided theywould start their own consulting company, focusing on setting upSAP software applications for companies.

They started S and O Consultants as an equal partnership,considering incorporating later on. Through some very hard work,and the popularity of SAP applications, the company grew over acouple years to a point where they had 10 employees and plenty ofopportunities. In 2009, they had earned revenues of approximately$3.5 million and net income of $750,000.

The focus of the company is to evaluate the current system ofthe company, install SAP applications for the company, incorporatethe existing company data into the new SAP application, and trainemployees in the use of SAP applications. These four steps wereincluded in every consultation project. In the past year, 2009, thecompany had completed 100 projects. An income statement for thepast year, 2009, is shown in Table One.

Table One

S and O Consultants | |||

Income Statement | |||

For the Year Ended December 31, 2009 | |||

Projects completed | 100 | ||

Project revenue | 3,500,000 | ||

Consulting salaries | 1,000,000 | ||

Overhead expenses | 1,750,000 | ||

Total expenses | 2,750,000 | ||

Net Income | 750,000 | ||

Their consulting company in the past had taken every projectoffered to them. They wanted to build up a clientele, and overtimehave built up a very good name within the consulting environment.They had worked very hard over the past couple of years putting ina lot of overtime, working most weekends, building up the companyand the number of clients. They have gotten to a point where theywant to work less and not take on every project; they can start tobe choosy about which projects they decide to take on. Stephen andLuanne are trying to figure out which projects to choose, basedupon which projects were the most profitable and the best use oftheir time. They have kept very good records, accumulating somevery valuable information over the last couple of years, and wouldlike to process that information to help them figure out whichprojects are the most profitable and which they should pursue inthe future.

They hired a small business consultant, Makayla Carter, to helpthem try to figure out which projects are most profitable. Makaylacategorized the projects by length of time to complete, going fromshortest amount of time to longest amount of time. The total numberof projects completed last year was 100. The total projects wereseparated into the 75 shortest and the 25 longest, based uponconsulting salaries - the 75 shortest projects cost ½ of the totalconsulting salaries or $500,000 of the $1,000,000, and the 25longest projects cost the other ½ of the total consulting salaries,or $500,000. As you can see from Table One, the 100 projectsaccumulated consulting salaries of $1,000,000 â this amount waseasy to track. The overhead expense of $1,750,000 is not so easy toapply to the different size consulting projects. This informationis needed to complete the processing of the information todetermine which length projects are most profitable and should bepursued in the future. Makaya decides to use consulting salaries asthe base to apply the overhead expense to the different lengthprojects.

Using the standard costing method, the consulting salaries wereused as the basis for separating the overhead into the shorter orlonger projects. The resulting income statements are shown in TableTwo. As indicated by table two, $1,925,000 revenue was generated bythe 75 shorter projects, and $1,575,000 was generated by the 25longer projects.

Table Two

S and O Consultants | ||||

Income Statement | ||||

For the Year Ended December 31, 2009 | ||||

Longer projects | Shorter projects | Total | ||

Projects completed | 25 | 75 | 100 | |

Project revenue | 1,575,000 | 1,925,000 | 3,500,000 | |

Consulting salaries | 500,000 | 500,000 | 1,000,000 | |

Overhead expenses | 875,000 | 875,000 | 1,750,000 | |

Total expenses | 1,375,000 | 1,375,000 | 2,750,000 | |

Net Income | 200,000 | 550,000 | 750,000 | |

Makayla was not confident in this information, based uponstandard costing; she was not sure if this was completely accurateand providing the information they needed. She does not think thatthis information is a good indicator of which projects, shorter orlonger, should be pursued. She decides that standard costing is notthe appropriate way to go and that ABC costing would give muchbetter information. The only problem is that she has to go all outof town for a conference that will not be able to complete this forStephen and Luanne. She is asking for your assistance.

By re-categorizing the total overhead expenses of $1,750,000further, the following activity based categories and their totaloverhead expenses and correlating physical measurements areprovided in Table Three.

Table Three

Total Cost | Physical measurement | Longer | Shorter | |

Evaluation of the current system | 600,000 | 30,000 | 7,500 | 22,500 |

Install the SAP application software (Manhours) | 350,000 | 500 | 100 | 400 |

Incorporate the existing company | 300,000 | 2,000 | 600 | 1,400 |

Train the employees of the company | 500,000 | 500 | 75 | 425 |

S and O Consultants

Stephen Michaels and Luanne Taylor met at Country HillsElementary School when they were young and talked about startingtheir own business when they grew up. In 2005, after they bothgraduated from college and worked a couple years they decided theywould start their own consulting company, focusing on setting upSAP software applications for companies.

They started S and O Consultants as an equal partnership,considering incorporating later on. Through some very hard work,and the popularity of SAP applications, the company grew over acouple years to a point where they had 10 employees and plenty ofopportunities. In 2009, they had earned revenues of approximately$3.5 million and net income of $750,000.

The focus of the company is to evaluate the current system ofthe company, install SAP applications for the company, incorporatethe existing company data into the new SAP application, and trainemployees in the use of SAP applications. These four steps wereincluded in every consultation project. In the past year, 2009, thecompany had completed 100 projects. An income statement for thepast year, 2009, is shown in Table One.

Table One

S and O Consultants | |||

Income Statement | |||

For the Year Ended December 31, 2009 | |||

Projects completed | 100 | ||

Project revenue | 3,500,000 | ||

Consulting salaries | 1,000,000 | ||

Overhead expenses | 1,750,000 | ||

Total expenses | 2,750,000 | ||

Net Income | 750,000 | ||

Their consulting company in the past had taken every projectoffered to them. They wanted to build up a clientele, and overtimehave built up a very good name within the consulting environment.They had worked very hard over the past couple of years putting ina lot of overtime, working most weekends, building up the companyand the number of clients. They have gotten to a point where theywant to work less and not take on every project; they can start tobe choosy about which projects they decide to take on. Stephen andLuanne are trying to figure out which projects to choose, basedupon which projects were the most profitable and the best use oftheir time. They have kept very good records, accumulating somevery valuable information over the last couple of years, and wouldlike to process that information to help them figure out whichprojects are the most profitable and which they should pursue inthe future.

They hired a small business consultant, Makayla Carter, to helpthem try to figure out which projects are most profitable. Makaylacategorized the projects by length of time to complete, going fromshortest amount of time to longest amount of time. The total numberof projects completed last year was 100. The total projects wereseparated into the 75 shortest and the 25 longest, based uponconsulting salaries - the 75 shortest projects cost ½ of the totalconsulting salaries or $500,000 of the $1,000,000, and the 25longest projects cost the other ½ of the total consulting salaries,or $500,000. As you can see from Table One, the 100 projectsaccumulated consulting salaries of $1,000,000 â this amount waseasy to track. The overhead expense of $1,750,000 is not so easy toapply to the different size consulting projects. This informationis needed to complete the processing of the information todetermine which length projects are most profitable and should bepursued in the future. Makaya decides to use consulting salaries asthe base to apply the overhead expense to the different lengthprojects.

Using the standard costing method, the consulting salaries wereused as the basis for separating the overhead into the shorter orlonger projects. The resulting income statements are shown in TableTwo. As indicated by table two, $1,925,000 revenue was generated bythe 75 shorter projects, and $1,575,000 was generated by the 25longer projects.

Table Two

S and O Consultants | ||||

Income Statement | ||||

For the Year Ended December 31, 2009 | ||||

Longer projects | Shorter projects | Total | ||

Projects completed | 25 | 75 | 100 | |

Project revenue | 1,575,000 | 1,925,000 | 3,500,000 | |

Consulting salaries | 500,000 | 500,000 | 1,000,000 | |

Overhead expenses | 875,000 | 875,000 | 1,750,000 | |

Total expenses | 1,375,000 | 1,375,000 | 2,750,000 | |

Net Income | 200,000 | 550,000 | 750,000 | |

Makayla was not confident in this information, based uponstandard costing; she was not sure if this was completely accurateand providing the information they needed. She does not think thatthis information is a good indicator of which projects, shorter orlonger, should be pursued. She decides that standard costing is notthe appropriate way to go and that ABC costing would give muchbetter information. The only problem is that she has to go all outof town for a conference that will not be able to complete this forStephen and Luanne. She is asking for your assistance.

By re-categorizing the total overhead expenses of $1,750,000further, the following activity based categories and their totaloverhead expenses and correlating physical measurements areprovided in Table Three.

Table Three

Total Cost | Physical measurement | Longer | Shorter | |

Evaluation of the current system | 600,000 | 30,000 | 7,500 | 22,500 |

Install the SAP application software (Manhours) | 350,000 | 500 | 100 | 400 |

Incorporate the existing company | 300,000 | 2,000 | 600 | 1,400 |

Train the employees of the company | 500,000 | 500 | 75 | 425 |

Questions:

2. Use the re-categorized information in Table Three tocalculate the appropriate rates for each of the four categories toapply the overhead based on the ABC costing method.