COMMERCE 1AA3 Lecture Notes - Lecture 12: Interest Expense, Operating Expense

27 Oct 2016

School

Department

Course

Professor

Document Summary

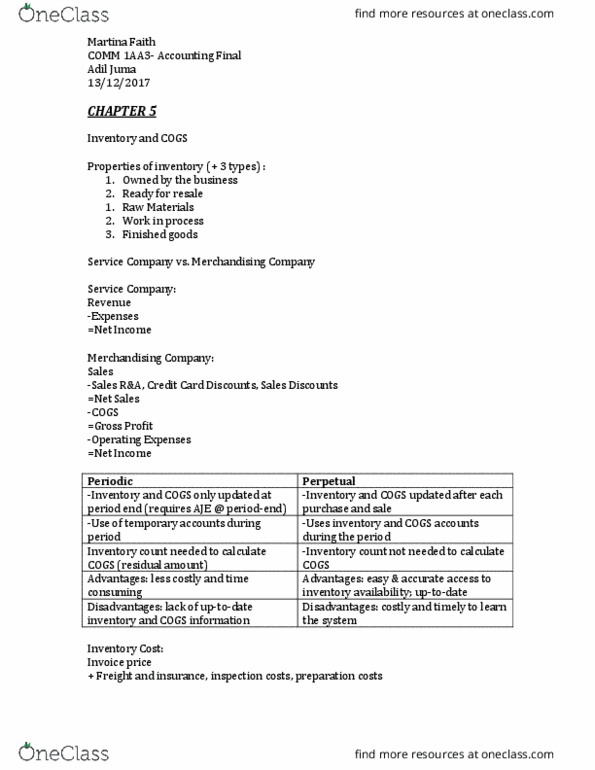

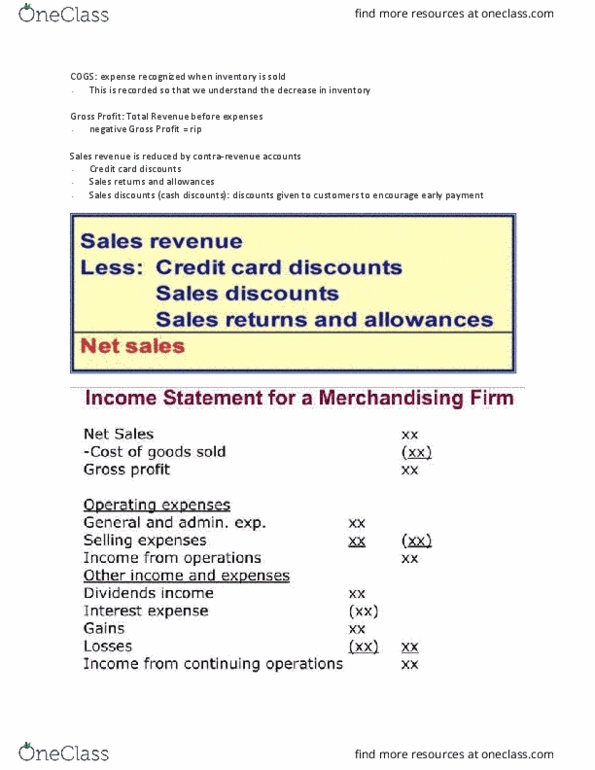

Sales - cost of goods sold = gross profit. Gross profit - operating expense = earnings before interest and tax (ebit) Sales, revenue and sales revenue can be used interchangeably. Credit card discounts ( percent of sales that credit card company keeps ) Sales returns (return of goods ) and allowances ( reimbursement?) Sales discounts ( cash discounts ) ( to encourage early payment ) Dividends income ( interest earned from investing ) All costs incurred to prepare and acquire inventory for sale must be included in inventory. Inventory is counted in the end of the year. Consigned good - holding products from another company, should not be counted as inventory, since it does not belong to you. If goods are sold on fob destination, and goods are in transit ( train, on ship ), revenue cannot be recorded. Until the buyer receives the goods, the goods are the responsibility of the seller.