COMMERCE 1AA3 Lecture Notes - Lecture 5: Current Liability, Income Statement, Accrual

19 Nov 2016

School

Department

Course

Professor

Document Summary

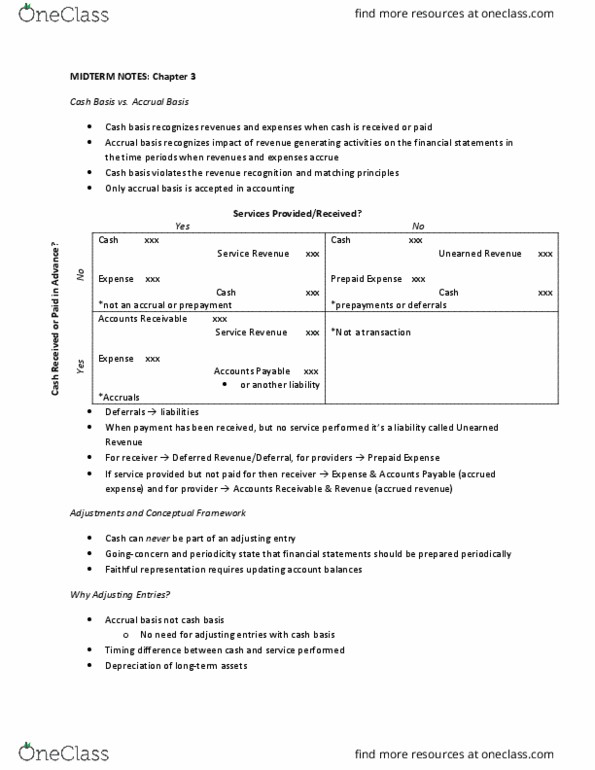

Cash basis recognizes revenues and expenses when cash is either received or paid. Accrual basis recognizes the impact of revenue generating activities on the financial statements in the time periods wen revenues and expenses accrue. The earnings process is complete or nearly complete. Resources consumed to earn revenues in an accounting period should be recorded in that period, regardless of when cash is paid. Adjustments are end-of-year journal entries to update account balances. Going-concern and periodicity dictate that financial statements be prepared periodically. Timing differences between cash and performance give rise to the need for adjusting entries. Prepayments (deferrals): result when cash is received or paid before services are provided or received. Accruals: result when services are provided or received before cash is received or paid. Ending supplies= beginning supplies+ supplies purchases- supplies expense. Ending a/p= beginning a/p+ purchases on account payment to suppliers. Therefore the depreciation is defined as the systematic allocation of the asset"s cost.