COMMERCE 1AA3 Lecture 1: COMMERCE 1AA3- Chapter 6

11 Jan 2019

School

Department

Course

Professor

Document Summary

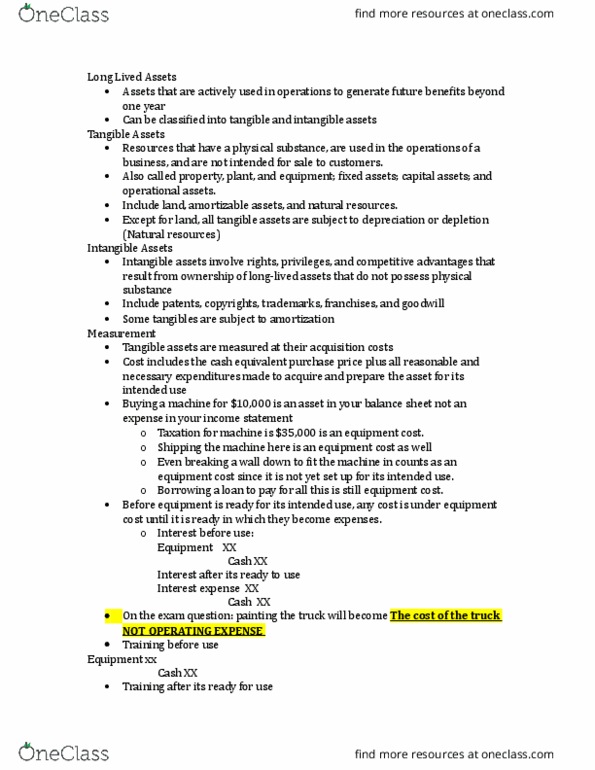

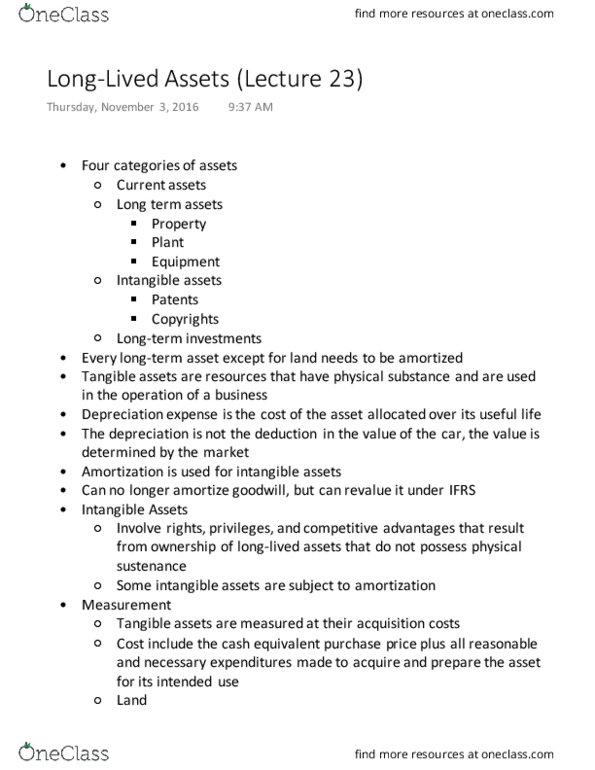

Management discretion- choice of accounting method, assumptions ex. bad debt expense methods- aging, percentage. Long-lived assets: assets that are actively used in operations to generate future benefits beyond one year, can be classified into tangible and intangible assets. ), and natural resources (mineral deposits and timber: except for land, all tangible assets are subject to depreciation or depletion (natural resources) Intangible assets involve rights, privileges, and competitive advantages that result from ownership of long-lived assets that do not possess physical substance. Include patents, copyrights, trademarks, franchises, and goodwill: some intangibles are subject to amortization. The cost of an asset includes all expenditures necessary to get the asset ready for its intended use. The cost of removing unwanted construction on land is part of the cost of land. Land: purchase price, commissions, survey & legal fees, back property taxes paid, grading and removing unwanted buildings. A business signs a ,000 note payable to purchase land for a new production facility.