COMMERCE 1AA3 Lecture Notes - Lecture 2: Net Income, Income Statement, Railways Act 1921

18 May 2016

School

Department

Course

Professor

Document Summary

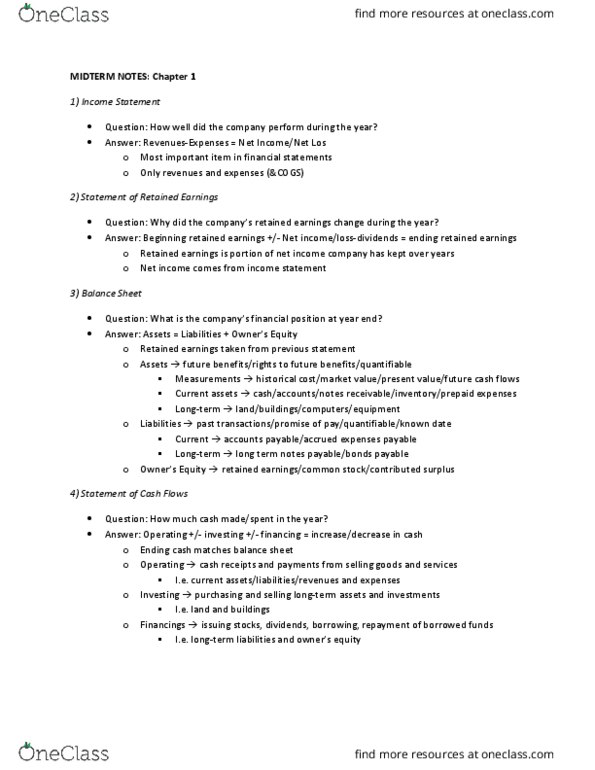

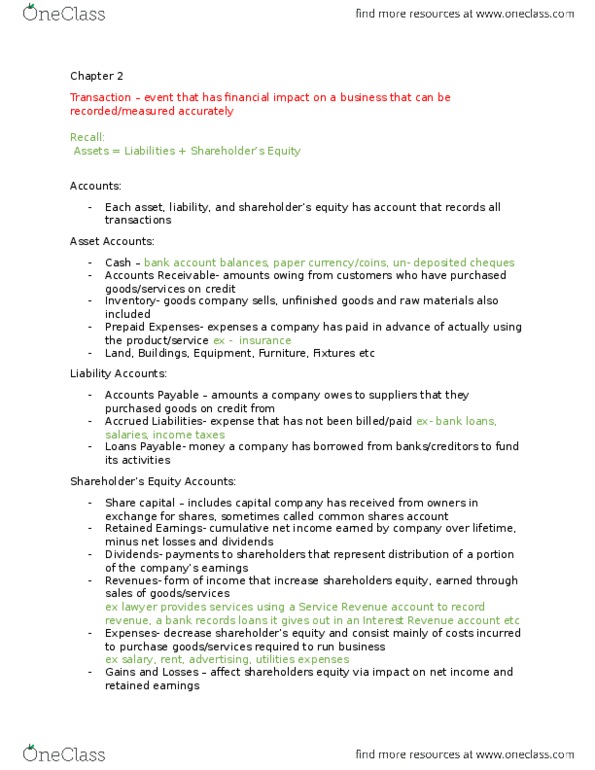

A (cid:396)e(cid:272)o(cid:396)d of ea(cid:272)h assets, lia(cid:271)ilities of o(cid:449)(cid:374)e(cid:396)s" e(cid:395)uit(cid:455: basic summary device of accounting. Cash: money and other medium of exchange. Accounts receivable: promise for future collection of cash, more informal, usually from selling goods. Notes receivable: signed by customer promising to pay, more binding and has interest, usually from lending out money. Prepaid expenses: expenses paid in advance, asset because they provide a future benefit. Land, buildings, equipment, furniture & fixtures: listed under property, plant, equipment. Accounts payable: promise to pay in future. Notes payable: signed by company promising to pay. Accrued liabilities: liability for an expense (cid:455)ou ha(cid:448)e(cid:374)"t paid yet, e. g. Common stock: owners investment in the company. Expenses: cost of operating a business. An event that affects financial position: can be reliably recorded. Students invest ,000 in a company: cash (cid:894)asset(cid:895) Company issues common shares: co(cid:373)(cid:373)o(cid:374) sto(cid:272)k (cid:894)e(cid:395)uit(cid:455)(cid:895) Company pays ,000 cash for land: cash (asset, la(cid:374)d (cid:894)asset(cid:895)