COMMERCE 2AB3 Lecture Notes - Lecture 17: European Cooperation In Science And Technology

26 Jun 2018

School

Department

Course

Professor

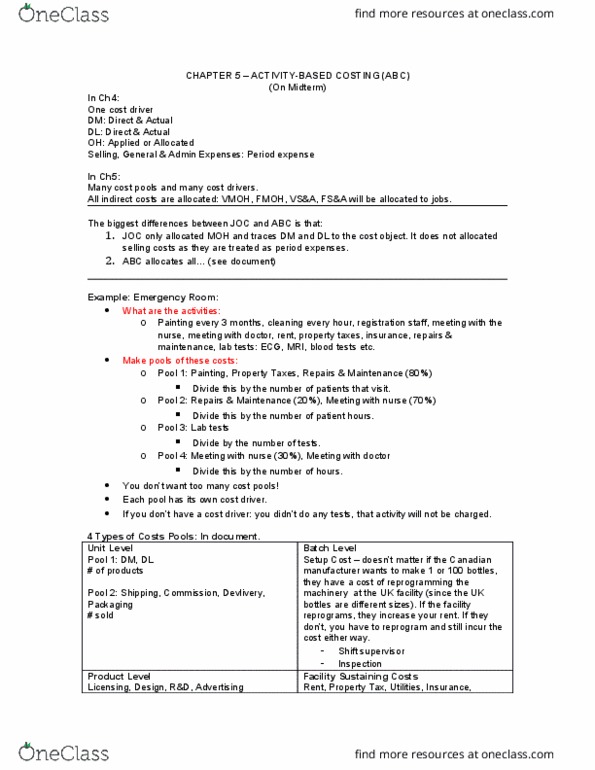

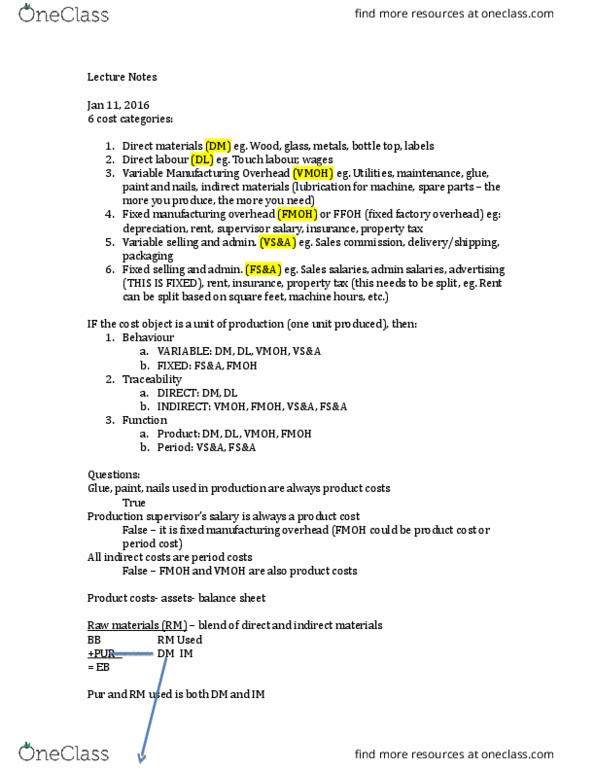

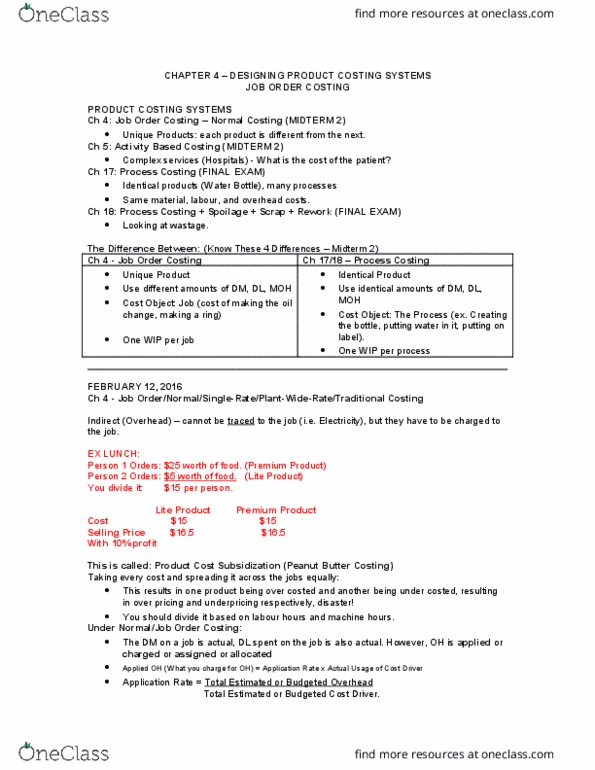

CHAPTER 17 – PROCESS COST ACCOUNTING

Identical products – Homogeneous Products

Uses the same amount of material for each product (DM, DL, MOH)

Different processes where each process is a WIP account.

oHighly automated, so very little labour, most of it is MOH, so DL and MOH is

combined.

oSo we only have 3 costs:

DM – added at a specific time in the process

Conversion Costs (DL and MOH) –throughout the process

Transferred-In Cost for Process 2 is Transferred-Out Cost from the

previous process. After the last process it goes to FG.

Example:

500 bottles

Task 1: Glass for the 500 bottles.

Task 2: Between 20-25% of the process, you are putting beer into the glass.

Right now you have taken 500 bottles up to the 21% mark and the conveyor belt has stopped.

At 21% how many bottles are glass: 500.

At 21% how many bottles have beer in them:

All 500 bottles have 20% of beer in them. This is because 100% of beer is added over a 5% of

the process (20% - 25%). This means that each percent of the process adds 20% of beer to the

bottles. So now:

Physical bottles have 20% of beer in them is 500. If 500 bottles have 20% beer in them then it is

AS IF 100 bottles have beer in them.

At 21% how many bottles worth of conversion costs are there: If there are 500 bottles of

beer that are 21% complete with respect to the process. This means that there is an

EQUIVALENT of 500 x 21% = 105 EQUIVALENT bottles of conversion cost already completed.

In summary: There are 500 bottles that are physical. There are 500 beer bottles EQUIVALENT of

glass. There are 100 bottles EQUIVALENT of beer. There are 105 bottles EQUIVALENT of

conversion costs.

In process costing each process is a WIP

The output of process 1 is the input of process 2. The output = transferred out costs. The input =

transferred in. That is how we accumulate costs from process 1 to process n.

The output of process N is transferred out to FINISHED GOODS.

Usually DM is added at a point during the process, whereas the conversion costs are added

uniformly throughout the process. There can be cases when DM is added for a portion of the

process e.g. adding the beer to the beer bottle between 20% of the process and 25% of the

process.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Uses the same amount of material for each product (dm, dl, moh) Different processes where each process is a wip account: highly automated, so very little labour, most of it is moh, so dl and moh is combined, so we only have 3 costs: Dm added at a specific time in the process. Conversion costs (dl and moh) throughout the process. Transferred-in cost for process 2 is transferred-out cost from the previous process. After the last process it goes to fg. Task 2: between 20-25% of the process, you are putting beer into the glass. Right now you have taken 500 bottles up to the 21% mark and the conveyor belt has stopped. At 21% how many bottles are glass: 500. At 21% how many bottles have beer in them: All 500 bottles have 20% of beer in them. This is because 100% of beer is added over a 5% of the process (20% - 25%).