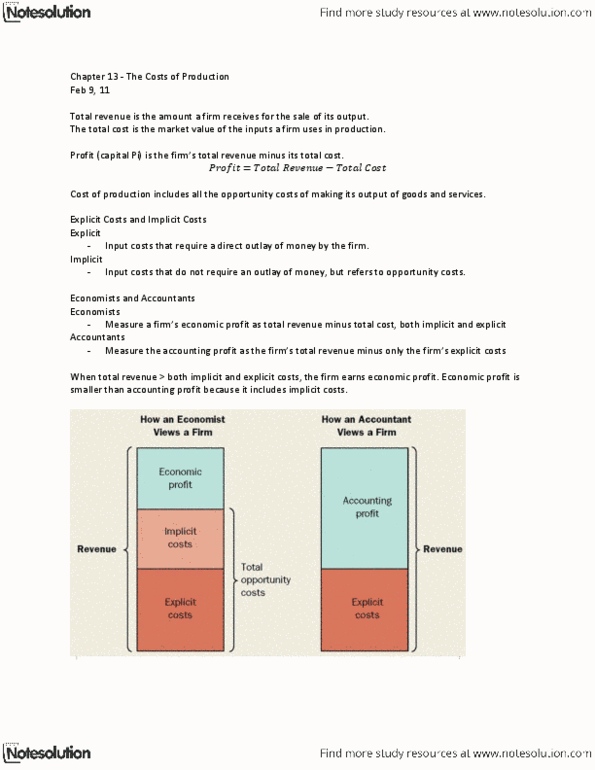

ECON 1B03 Lecture Notes - Lecture 5: Average Cost, Average Variable Cost, Marginal Cost

29 Jan 2020

School

Department

Course

Professor

Marginal product

the increase in output that arises from an additional unit of input

Diminishing marginal product

the property whereby the marginal product of an input declines as the

quantity of the input increases

Fixed costs

costs that do not vary with the quantity of output produced

Variable cost

costs that vary with the quantity of output produced

Average total cost

total cost divided by the quantity of output

Average fixed cost

fixed costs divided by the quantity of output

Average variable cost

variable costs divided by the quantity of output

Marginal cost

an increase in total cost that arises from an extra unit of production

Efficient scale

the quantity of input that minimizes average total cost

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

Marginal product the increase in output that arises from an additional unit of input. Diminishing marginal product the property whereby the marginal product of an input declines as the quantity of the input increases. Fixed costs costs that do not vary with the quantity of output produced. Variable cost costs that vary with the quantity of output produced. Average total cost total cost divided by the quantity of output. Average fixed cost fixed costs divided by the quantity of output. Average variable cost variable costs divided by the quantity of output. Marginal cost an increase in total cost that arises from an extra unit of production.