COMM 111 Lecture Notes - Lecture 2: Accounts Payable, Transactional Analysis, Trial Balance

Document Summary

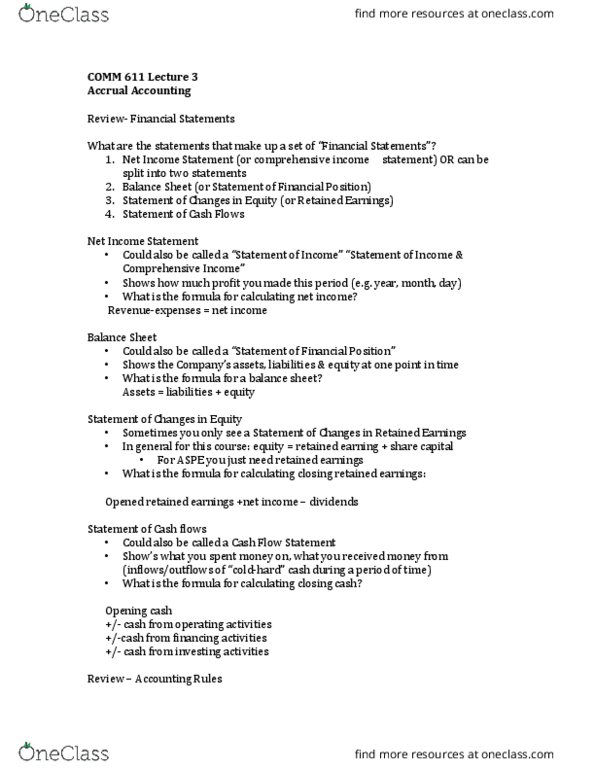

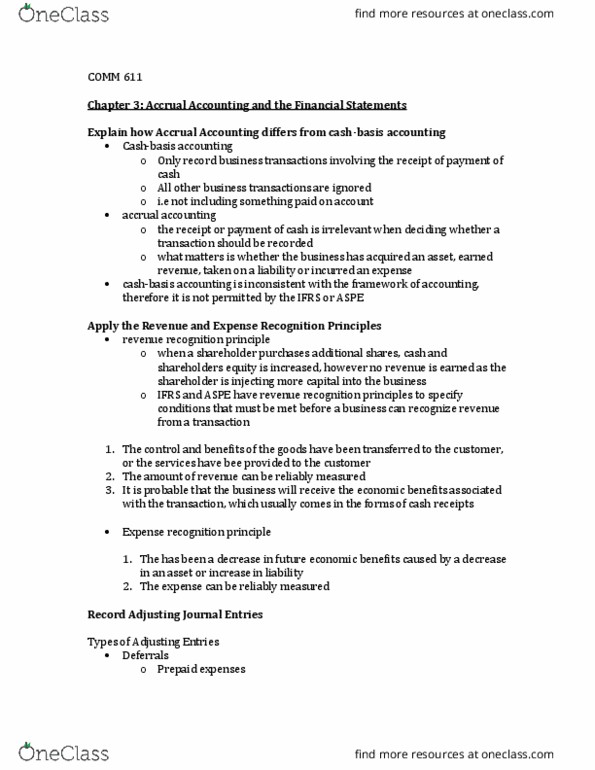

An asset is a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity. Accounting process: economic event, analyze transaction and prepare journal entry, post journal to general ledger, trial balance lists account totals, financial statements are prepared. A transaction is documented in a journal entry. The journal entry is posted to an account. The accounts are added up (individually) and used to create the trial balance. The trial balance is used to create the financial statements. Transaction journal entry (cid:523)t(cid:524) account trial balance financial statements. Accounts: we use accounts to record changes in assets, liabilities, equity, revenues and expenses, types of accounts. Assets: cash, accounts receivable, investments, inventory, land, building, etc. Equity: retained earnings, common shares, preferred shares, etc. Revenue: sales revenue, dividend revenue, interest revenue, etc. Expenses: salary, rent, utilities, advertising, cost of good sold, etc.