ACC 406 Lecture Notes - Lecture 1: Certified General Accountant, Continual Improvement Process, Chartered Professional Accountant

30 Jan 2017

School

Department

Course

Professor

Document Summary

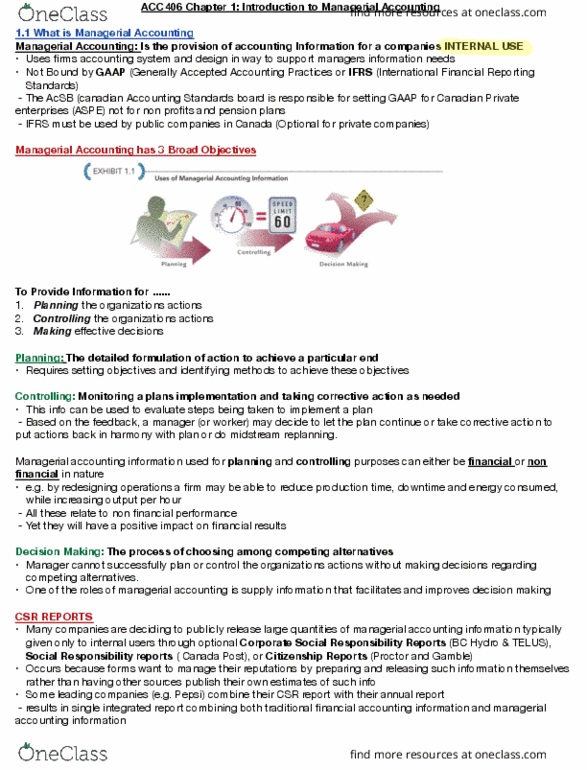

Provides accounting information for a (cid:272)o(cid:373)pa(cid:374)y"s internal users. Designed to provide information for (three board objectives); Information needs for planning, controlling and decision making. Detailed formulation of action to achieve a particular end is the management activity called planning. Planning requires setting objectives and identifying methods to achieve those objectives. Mo(cid:374)itori(cid:374)g a pla(cid:374)"s i(cid:373)ple(cid:373)e(cid:374)tatio(cid:374) a(cid:374)d taki(cid:374)g (cid:272)orre(cid:272)tive a(cid:272)tio(cid:374) as (cid:374)eeded is referred to as control. Controlling is achieved by comparing actual performance with expected performance. The process of choosing among competing alternative is called decision making. Intertwined with planning & controlling as the manager will not be able to plan or control the organizations actions without making a decision regarding competing alternatives. Target users for financial accounting external users. Target users for managerial accounting internal users. Restrictions on financial accounting must follow externally imposed guidelines. Restriction on managerial accounting not required to follow any guidelines. Types of info financial accounting produces objectives and verifiable financial info.