ACC 406 Chapter 1: Chapter 1 Introduction to Managerial Accounting

21 Feb 2018

School

Department

Course

Professor

Document Summary

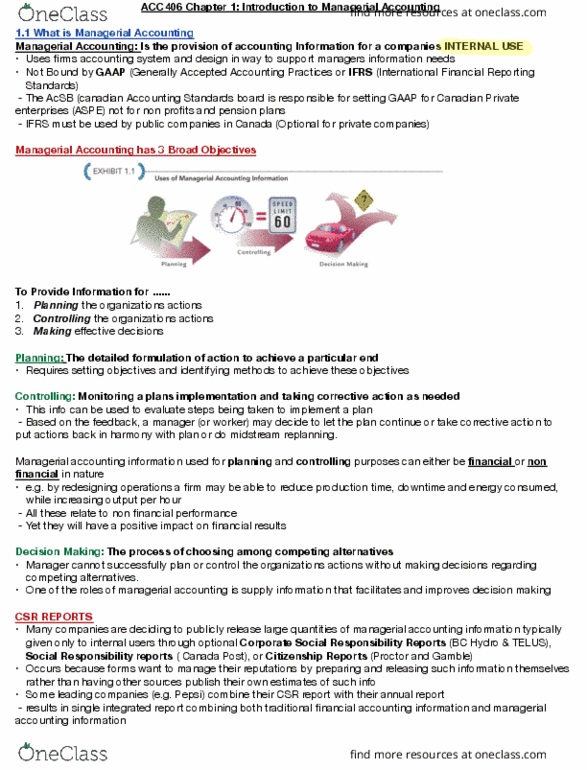

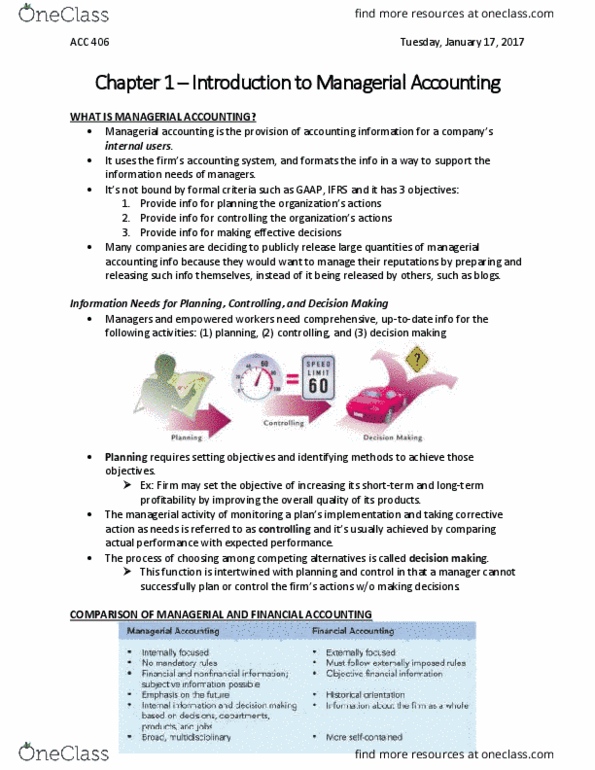

Managerial accounting is the provision of accounting information for a company"s internal users. It uses the rms accounting system, and formats the information in a way to support the information needs of managers. Unlike nancial accounting, managerial accounting is not bound by any formal criteria such as gaap or ifrs, has broad objectives. To provide information for planning the organization"s actions. To provide information for controlling the organizations actions. To provide information for making e ective decisions. Information needs for planning, controlling and decision making. Managerial accounting informations needed by a variety of individuals. In particular, managers and empowered workers need comprehensive, up to date information for the following activities: planning, controlling, decision making. The detailed formulation of action to achieve a particular end is the management activity called. Planning requires setting objectives and identifying methods to achieve those objectives. The managerial activity of monitoring a plan"s implementation and taking corrective action as needed is referred to as controlling.