ACC 406 Lecture 5: Lecture 5

Get access

Related Documents

Related Questions

AirComp Corporation produces component parts for the aircraftindustry. In prior years, they maintained a job-costing systemconsisting of direct materials and direct labor cost andmanufacturing overhead. Manufacturing overhead was allocated toproduction jobs using a single-indirect cost allocation rate, whichwas $115 per direct labor hour.

For 20x1, the Company decided to change the method of allocatingmanufacturing overhead to production jobs from the single-indirectcost allocation approach to the activity-based costing (âABCâ)indirect cost allocation approach. For purposes of developing theABC allocation rates, AirCompâs cost accounting team prepared thefollowing analysis:

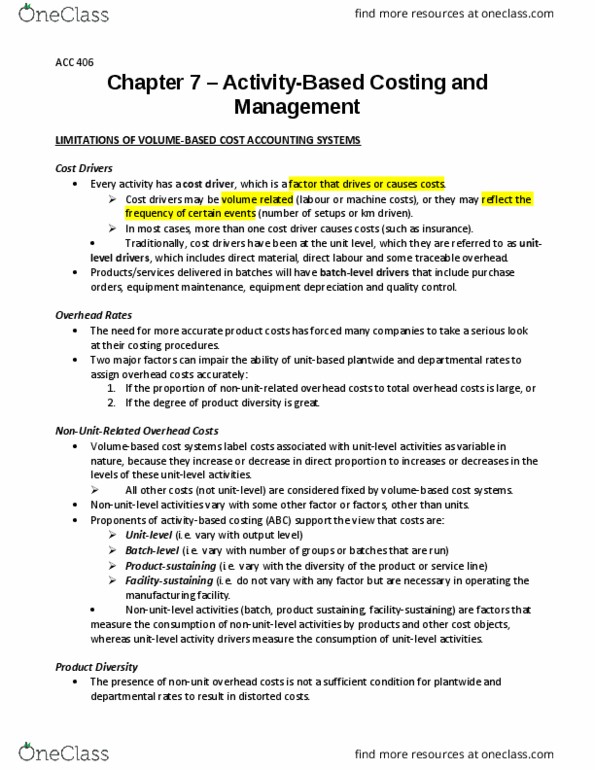

Activity | Cost Driver | Allocation Rate |

Material handling | Parts handled | $0.40 |

Lathe work | No. of lathe turns | $0.20 |

Milling | Machine hours | $20.00 |

Grinding | No. of parts ground | $0.80 |

Testing | No. of units tested | $15.00 |

For 20x1, AirCompâs cost accountant team prepared the followinganalysis of the direct costs and indirect cost activities for Job100 and Job 200, the only production jobs in process for theperiod:

Job 100 | Job 200 | |

Direct materials cost | $9,700 | $59,900 |

Direct labor cost | $750 | $11,250 |

No. of direct manufacturing labor hours | 25 | 375 |

No. of parts ground | 500 | 2,000 |

No. of lathe turns | 20,000 | 60,000 |

Machine hours | 150 | 1,050 |

No. of units produced during period (all are tested) | 10 | 200 |

Required

1.For each job, determine total per unit cost using direct laborhours to allocate manufacturing overhead to each job.

2.For each job, determine total per unit cost using anactivity-based costing approach to allocate manufacturing overheadcost to job.

3.Compare the per unit cost figures for each job computed instep a. and step b., above. Why do the new ABC approach differ fromthe single-indirect cost allocation systems differ in the amount ofthe per unit indirect cost allocated to each job (i.e. what was theimplications of the cost allocation method change on the amount ofper unit cost allocated to each job and what factors caused theobserved changes).

4.How might AirComp Corporation use the information from ABCallocation approach to better manage its business, i.e. what arethe advantages of using an activity-based costing approach?

Hi-Tek Manufacturing Inc. makes two types of industrial component partsâthe B300 and the T500. An absorption costing income statement for the most recent period is shown below:

| Hi-Tek Manufacturing Inc. Income Statement | |||

| Sales | $ | 1,761,600 | |

| Cost of goods sold | 1,249,034 | ||

| Gross margin | 512,566 | ||

| Selling and administrative expenses | 580,000 | ||

| Net operating loss | $ | (67,434) | |

Hi-Tek produced and sold 60,300 units of B300 at a price of $21 per unit and 12,700 units of T500 at a price of $39 per unit. The companyâs traditional cost system allocates manufacturing overhead to products using a plantwide overhead rate and direct labor dollars as the allocation base. Additional information relating to the companyâs two product lines is shown below:

| B300 | T500 | Total | ||||||||||

| Direct materials | $ | 400,500 | $ | 162,200 | $ | 562,700 | ||||||

| Direct labor | $ | 120,000 | $ | 42,700 | 162,700 | |||||||

| Manufacturing overhead | 523,634 | |||||||||||

| Cost of goods sold | $ | 1,249,034 | ||||||||||

The company has created an activity-based costing system to evaluate the profitability of its products. Hi-Tekâs ABC implementation team concluded that $55,000 and $101,000 of the companyâs advertising expenses could be directly traced to B300 and T500, respectively. The remainder of the selling and administrative expenses was organization-sustaining in nature. The ABC team also distributed the companyâs manufacturing overhead to four activities as shown below:

| Manufacturing | Activity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Activity Cost Pool (and Activity Measure) | Overhead | B300 | T500 | Total | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Machining (machine-hours) | $ | 209,884 | 90,600 | 62,600 | 153,200 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Setups (setup hours) | 152,650 | 75 | 280 | 355 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Product-sustaining (number of products) | 100,600 | 1 | 1 | 2 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other (organization-sustaining costs) | 60,500 | NA | NA | NA | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total manufacturing overhead cost | $ | 523,634 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Hi-Tek Manufacturing Inc. makes two types of industrial component partsâthe B300 and the T500. An absorption costing income statement for the most recent period is shown below: |

| Hi-Tek Manufacturing Inc. Income Statement | ||

| Sales | $ | 1,751,700 |

| Cost of goods sold | 1,223,464 | |

| Gross margin | 528,236 | |

| Selling and administrative expenses | 560,000 | |

| Net operating loss | $ | (31,764) |

| Hi-Tek produced and sold 60,200 units of B300 at a price of $21 per unit and 12,500 units of T500 at a price of $39 per unit. The companyâs traditional cost system allocates manufacturing overhead to products using a plantwide overhead rate and direct labor dollars as the allocation base. Additional information relating to the companyâs two product lines is shown below: |

| B300 | T500 | Total | ||||

| Direct materials | $ | 401,000 | $ | 162,400 | $ | 563,400 |

| Direct labor | $ | 120,900 | $ | 42,400 | 163,300 | |

| Manufacturing overhead | 496,764 | |||||

| Cost of goods sold | $ | 1,223,464 | ||||

| The company has created an activity-based costing system to evaluate the profitability of its products. Hi-Tekâs ABC implementation team concluded that $58,000 and $107,000 of the companyâs advertising expenses could be directly traced to B300 and T500, respectively. The remainder of the selling and administrative expenses was organization-sustaining in nature. The ABC team also distributed the companyâs manufacturing overhead to four activities as shown below: |

| Manufacturing | Activity | ||||||||||||||||

| Activity Cost Pool (and Activity Measure) | Overhead | B300 | T500 | Total | |||||||||||||

| Machining (machine-hours) | $ | 209,884 | 90,400 | 62,800 | 153,200 | ||||||||||||

| Setups (setup hours) | 125,580 | 79 | 220 | 299 | |||||||||||||

| Product-sustaining (number of products) | 100,800 | 1 | 1 | 2 | |||||||||||||

| Other (organization-sustaining costs) | 60,500 | NA | NA | NA | |||||||||||||

| Total manufacturing overhead cost | $ | 496,764 | |||||||||||||||

| |||||||||||||||||

| 2. | Compute the product margins for B300 and T500 under the activity-based costing system. (Negative product margins should be indicated by a minus sign. Round your intermediate calculations to 2 decimal places.) | |||||||||||

|

3.)

| Prepare a quantitative comparison of the traditional and activity-based cost assignments. (Round your intermediate calculations to 2 decimal places and "Percentage" answer to 1 decimal place. (i.e. .1234 should be entered as 12.3) and other answers to nearest whole dollar amounts.)

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||