ACC 406 Chapter Notes - Chapter 7: Cost Driver, Resource Consumption, Cost Accounting

2 Apr 2017

School

Department

Course

Professor

Document Summary

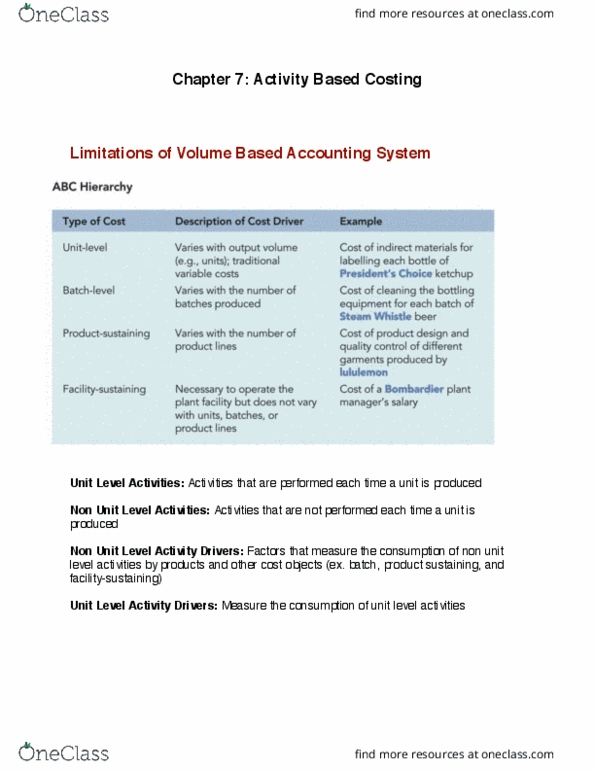

Every activity has a cost driver, which is a factor that drives or causes costs. Cost drivers may be volume related (labour or machine costs), or they may reflect the frequency of certain events (number of setups or km driven). In most cases, more than one cost driver causes costs (such as insurance). Traditionally, cost drivers have been at the unit level, which they are referred to as unit- level drivers, which includes direct material, direct labour and some traceable overhead. Products/services delivered in batches will have batch-level drivers that include purchase orders, equipment maintenance, equipment depreciation and quality control. The need for more accurate product costs has forced many companies to take a serious look at their costing procedures. Two major factors can impair the ability of unit-based plantwide and departmental rates to assign overhead costs accurately: If the proportion of non-unit-related overhead costs to total overhead costs is large, or. If the degree of product diversity is great.