ECN 104 Lecture Notes - Lecture 8: Marginal Revenue, Perfect Competition, Profit Maximization

15 Jan 2017

School

Department

Course

Professor

Document Summary

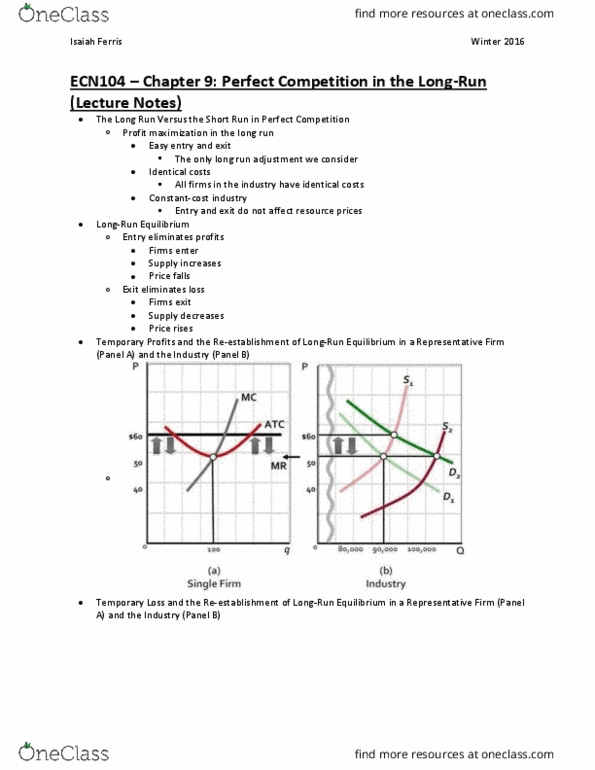

The long run versus the short run in perfect competition. Supply and demand curve hits at a point which is equilibrium because the price is constant price taken graph will have a horizontal line. You keep producing till you hit equilibrium or you keep producing when your cost is much smaller than your marginal revenue. You stop when marginal revenue is lower than cost. Before the mc curve company makes a normal profit. A decrease in demand temporarily lowers price. Lower prices drives away some competitors and the decrease in supply returns price to equilibrium. Increasing supply will lower demand also will lower price in the long run. Constant- cost industry: entry/exit does nto affect lr atc, constant resource price, special case. Increasing cost industry: most industries, lr atc increases with expansion, special resources. Decreasing cost industry: personal computer industry. Productive efficiency: producing where p = min. Allocative efficiency: producing where p = mc.