MKT 100 Lecture Notes - Lecture 3: Corporate Finance, Macroeconomics, Dividend Discount Model

1

MKT 100 Full Course Notes

Verified Note

1 document

Document Summary

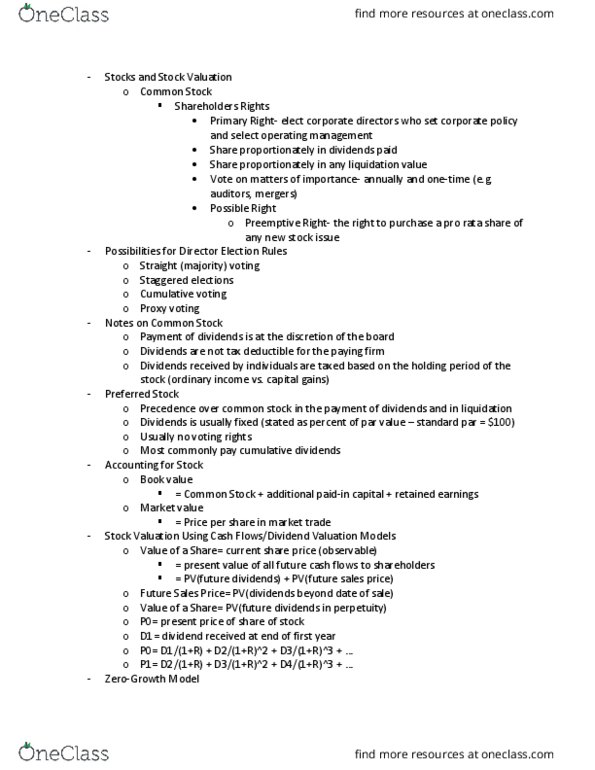

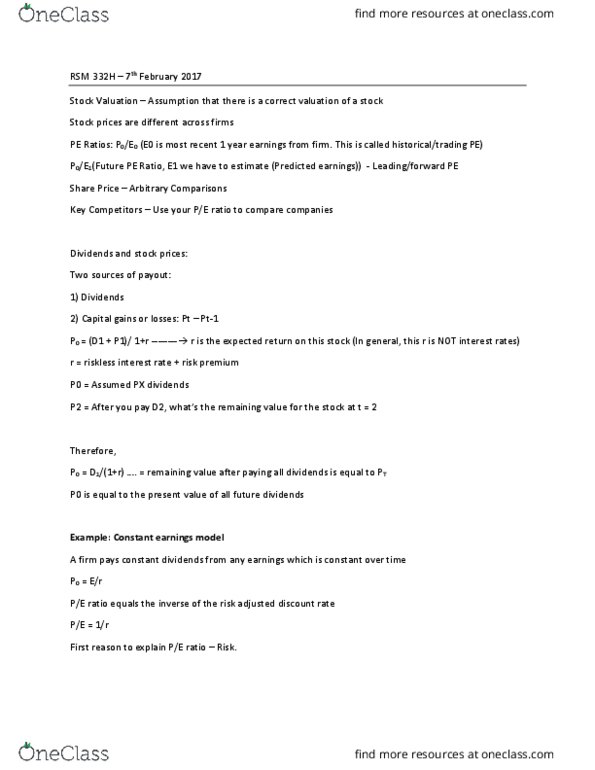

Stock valuation is more difficult than bond valuation because the cash flows are uncertain, the life is forever, and the required rate of return is unobservable. The cash flows to stockholders consist of dividends plus a future sale price. Let p0 be the current price of the stock, and assign p1 to be the price in one period. If d1 is the cash dividend paid at the end of the period, then: P0 = (d1 + p1) / (1 + r)1. However, the future sale price depends on the dividends paid after that point. Therefore, you can illustrate that the current stock price is ultimately the present value of all expected future dividends discounted at a rate (r) appropriate to the riskiness of the cash flows: You might be wondering about shares of stock in companies such as ebay that currently pay no dividends. Small, growing companies frequently plow back everything and thus pay no dividends.